In the aftermath of the Great Recession (and much longer), a number of countries saw negative savings rates. With debt they issued and – highlighted by the case of Cypress – money they seized, they effectively paid less money back than they borrowed from people. The US isn't there yet, but it makes us ask: would negative savings account interest rates would in the United States?

No Imminent Danger of Negative Rates

Even though negative rates aren't imminent in the United States, they are a theoretical. The US has moved to a positive federal funds rate in the aftermath of the recession.

So again - this isn't currently on the table.

Think about Cypress though, or treasuries in countries which are still negative. Larger accounts might still be earning negative rates on their savings. It's the small accounts where we didn't see as much movement - with some exceptions.

As a thought experiment, though:

- Could negative savings account interest rates happen here?

- If they were imminent, could you avoid them?

We Already –Technically – Saw Negative Interest Rates

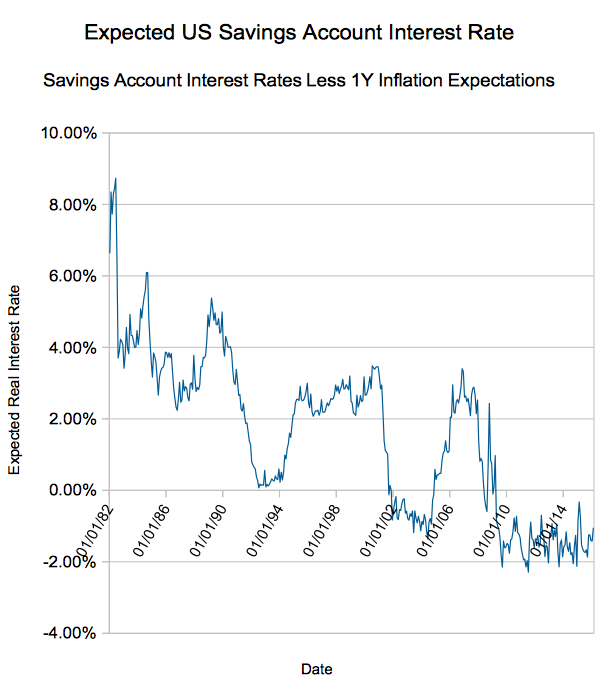

In the aftermath of the Great Recession we did see negative rates. I don't mean nominal rates - I mean inflation adjusted, or real rates.

You can derive an expected inflation rate from the market. Using the spread on inflation adjusted government debt and nominal debt you have a decent guess what the market expects from CPI over defined time frames. Even better, the Federal Reserve Bank of Cleveland maintains a series which adjusts expectations for bias.

For a few years post-crisis the market expected much more inflation than savings accounts were paying:

Now, your bank account also quotes a rate over the next 12 months (most banks probably don't publish their inflation expectations).

Essentially, though, if you expect higher inflation than your bank account pays you're settling for negative interest.

Data note: we mashed up the 1 month certificate of deposit series from the Fed, with the interest rate series on deposits under $100,000. It's not exact - but these are decent proxies for savings rates.

Real Returns Are Different than Negative Nominal Returns

It's true – in the above scenario your principal was still protected. Even when savings interest was 0% you'd get your money back.

That's one major difference between the aftermath and a true negative rate scenario.

What if it happened, though?

At first, your bank would probably either eat the cost of negative interest rates or increase fees.

At some point, though, one American bank will cross the rubicon and start charging negative rates. And, at first, some people will grin and bear it.

Remember, a bank isn't just providing interest. There are other conveniences and features to a bank:

- Debit cards and electronic transfers

- Bill pay

- Insurance on your cash

- Protection from disasters

- Safe storage

However, customers won't stick around forever. Eventually people will decide to pull cash from the bank.

That last graf isn't flippant. Negative rates in Japan caused a massive uptick in the number of people buying personal safes. Assuming your cash isn't destroyed, lost, or stolen, burying it in your backyard or under your mattress guarantees you your principal back.

You might also put your cash in some proxy, like gold. Again, Japan shows the way – Japanese citizens bought gold before a consumption tax law change in 2014.

(Note that in the United States, gold is taxed as a collectible – our Government already thought of that. Bitcoin too, before you get any ideas.)

In a Negative Interest Rate Scenario, Can You Just Hold Cash at Home?

In theory, yes. If you're able to get money from a bank you could attempt to hold it at home.

When the topic of negative interest rates first came up globally, the banking system came up with some "solutions". Chief among them: banning cash.

Especially around 2016 we saw a number of serious think pieces wanting to ban the $100 Bill (and the 500 Euro Note).

You can imagine why - the $100 is the largest denomination currently in use in the United States. It lets you store the most cash in the smallest volume.

This argument is quite literally the opposite side of the coin from when the US semi-seriously discussed removing small denomination coins. We've discussed seigniorage here on the site, and those denominations lose money. The $100 bill, however, prints money.

The argument around large bills also sometimes leans on criminality as a crutch. Criminals presumably like $100 bills (and 500 Euro bills) because they're easier to move - and there is evidence to back this up. The EU eventually killed the 500 Euro note citing this argument.

What countries don't broadcast is killing large bills also makes it easier to impose negative rates. If the largest bill you could get is a $20, you'd have to store 5 times as many bills at home in a negative rate scenario.

How much outstanding currency would banning the $100 affect?

At the end of 2018, there were $1.861 trillion in notes outstanding. $1.343 trillion of those were $100 bills. That's 72% of all bills!

Negative Savings Account Interest Rates Can Happen In the United States

Just because the United States hasn't seen negative savings account interest rates doesn't mean we can't. They've happened in other countries, and the EU has even provided a roadmap of banning large bills.

To summarize negative interest in the United States:

- In theory, you could see negative interest rates, even here.

- You would probably see rates get progressively more negative and marginal savers would react in different ways.

- The Government would make it less convenient to store money at home (and perhaps go after things like bitcoin and litecoin)

- You'll probably see further pushes to make more transactions electronic

And that's all there is to it, really. If negative rates do eventually come to the states, your best move might be investing in riskier assets:

- Money Market accounts

- Longer duration Government Debt or Inflation Adjusted Securities (see TreasuryDirect.gov)

- Corporate Debt

- Other AAA rated sovereign debt (note there is a FX risk)

- Prepay longer dated debt like mortgages

- Overpay your taxes and get a huge tax return (oh, the irony)

- Even riskier assets - take a pick from most other things in the world.

Let us know what you think you'd do under negative savings account interest rates:

- Prepay bills like property tax and insurance?

- Prepay the mortgage?

- Minimize the amount you leave in the bank?

- Decrease your tax withholding and get a fat return?