While net worth comparisons are interesting and revealing for all ages, net worth is most important for retirees. When people retire, they rely solely on wealth, periodic payments, and individual help to live.

Here's a cut of our wealth percentile data for American households headed by a 65+ year old individual. Beyond that, we further zoom to retiree wealth for ages 65-69, 70-74, 75-79, and for 80+.

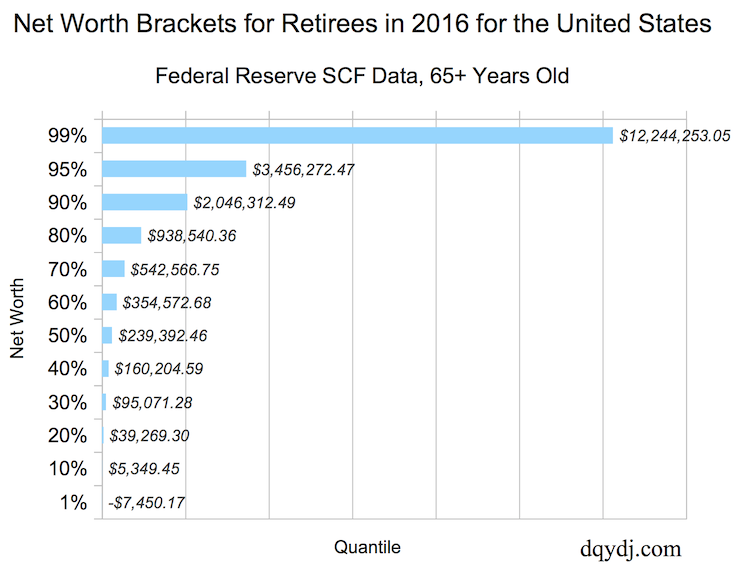

Retiree Wealth for Americans in 2016

These net worth quantile numbers come from the 2016 Federal Reserve SCF, first released in September, 2017. The Net Worth by Age Calculator contains specifics on data quality and the number of households. The summary we created, 65+ data, contains 1,538 responses.

Note that the numbers in this article do not attempt to include the value of Social Security or Pension payments.

In many ways net worth is superior to periodic payments, especially when it comes to gifting and inheritance. We'll attempt to quantify these income streams in a future article, but note that this post solely concerns assets and debts.

Further Breaking Down Retiree Net Worth in America

While interesting as a summary, the above data deserves further resolution. Don't expect all retiree spending stages to be the same - in theory, older households are fully adapted to retirement and spending at a different rate.

Those considerations in mind, we calculated retiree wealth for households headed by 65-69, 70-74, 75-79, and 80+ aged household heads.

Zoomed Retiree Wealth Brackets Using 2016 Data

| AGE | 65-69 | 70-74 | 75-79 | 80+ | 65+ |

| 1.00% | -$15,800.90 | -$3,733.34 | -$27,869.87 | -$2,005.82 | -$7,450.17 |

| 10.00% | $3,782.88 | $6,360.61 | $6,855.19 | $4,351.19 | $5,349.45 |

| 25.00% | $48,080.84 | $56,956.49 | $77,843.90 | $88,179.43 | $68,997.53 |

| 50.00% | $209,575.26 | $233,614.37 | $242,699.75 | $270,904.40 | $239,392.46 |

| 75.00% | $663,124.34 | $713,067.58 | $647,046.50 | $713,592.77 | $691,559.63 |

| 90.00% | $1,949,487.61 | $1,922,937.68 | $1,826,225.26 | $2,183,142.06 | $2,046,312.49 |

| 95.00% | $3,486,587.42 | $3,478,511.32 | $2,968,004.67 | $3,646,926.18 | $3,456,272.47 |

| 99.00% | $12,315,188.40 | $11,673,570.56 | $13,865,072.71 | $11,783,806.33 | $12,244,253.05 |

Remember, this data is a static snapshot of retiree (or retiree aged, anyway) net worth in 2016. Individuals in different brackets faced different stock, bond, and job market conditions reaching their current wealth.

In other words, this data doesn't necessarily show how individuals draw-down their wealth in retirement. Why would 80+ aged households have more wealth otherwise?

For older households, there is an increased propensity to spend or gift retiree wealth buttressed by the fact earned income is more uncommon for older households. We can't draw conclusions about individual retirees or even retirees as a percentile group over time using this snapshot. If you need an accurate figure on drawdowns, run the numbers on a longitudinal study such as the University of Michigan's PSID.

Anything Interesting in the Retiree Net Worth Data?

So, there you have it - a retiree wealth snapshot using our favored 2016 wealth dataset. As with the 2013 data, retirees have much greater wealth than younger age groups.

Keep in mind, as we've stated before... you can expect this wealth distribution in a society that produces a huge amount of wealth. Older age groups should hold more wealth before cycling it to younger folks through spending, gifting, and inheritance.

By that measure, this was a healthy print.

And yes, we know - pensions, periodic payments, and Social Security make a huge difference in consumption patterns, even if inferior to net worth. At some point we will model these forms of income in net worth.