Today please welcome guest poster Jason Hull. He'll go over all of the details you need to answer that age-old question: should you quit work to go to graduate school?

Should You Quit Work to Go to Graduate School?

“A man who has never gone to school may steal from a freight car; but if he has a university education, he may steal the whole railroad.”

--Theodore Roosevelt

When I was at West Point, I thought that there was no other possible outcome for the next 20 years of my life but to be a military officer. I was going to spend my first four years as a tanker and then convert to military intelligence (no oxymoron jokes, please; I’ve never consumed zit cleaner in my life) for the remainder of my time, and retire with a decent Army pension and spend the rest of my life sitting on the front porch watching traffic go by.

Then I actually arrived in the real Army replete with all of its bureaucracy and other fun activities. I loved being a platoon leader and an executive officer and working with soldiers, but there were also plenty of opportunities to do what we called “flying a desk.” I figured if I was going to fly a desk, I wanted to get paid what my civilian counterparts got paid to fly a desk!

Furthermore, during my second deployment to Bosnia, due to the nature of the work that I was doing, I had the opportunity to work quite a bit with the JAG officers (if you haven’t seen the old TV series, JAG is short for Judge Advocate General – the military’s lawyers). They kept waving the Jedi mind trick hand in front of my face.

“You want to be a lawyer.”

“I want to be a lawyer.”

“Being a lawyer is fun.”

“Being a lawyer is fun.”

“Alan Dershowitz is your hero.”

“What the?!?!”

Having decided that the military life was not for me, I submitted my resignation paperwork and began preparing for life outside of the military. As part of that preparation process, I spoke with a few recruiting firms that specialized in placing former junior military officers into the corporate world. I quickly discovered that they all specialized in placing former military officers either into process management jobs or pharmaceutical sales jobs.

One firm, though, offered to place the high-achieving junior officers into the elite consulting firms like McKinsey and Bain. I figured that being on the Dean’s List every year at West Point had to count for something, so I signed up to interview.

The interview was with the man who was the person behind the eponymously named firm. He was decked out in a 3 piece suit and interviewed me in the hotel suite he’d rented.

The first question was “what’s your GMAT score, son?”

Since the Army had offered free testing, I had taken them all: GMAT, GRE, and LSAT. I told him my score.

“You should go to a top 10 MBA program instead. You’ll make a lot more money.”

And that was the extent of my 2 minute interview with the man.

By that time, I also had an offer from WorldCom. This admission has just dated me and revealed my age. I could move to Jackson, Mississippi to do something with them and make $55k a year, a 36% pay jump over my military salary.

I applied to the top 10 MBA and law programs in the U.S. and a couple of “fallback” schools. I got accepted to the University of Virginia’s law program, and since it was near where my grandparents lived, that was the one I wanted to go to.

Their graduates earned an average salary of about $100,000.

I was faced with a decision: go to law school for 3 years at an overall cost of about $50k per year (once tuition, books, and living expenses were factored in) with the hopes of getting a job in a high end law firm earning about $100k per year (no certainty) or take a job making $55k a year.

This is a decision that a lot of career changers and people who feel like they’re not making as much progression in their jobs face.

Do I stay in my job or try to jump-start my career progression by going back to school for a graduate degree?

Alas, life is fraught with uncertainty. One of those pieces of uncertainty is that you could draw up the ultimate life and career plan, go to school, get your degree, and get spat out on the other end jobless. Penury is a pain in the butt, and, furthermore, student loan debt cannot be discharged in bankruptcy. Fortunately, aside from in Alabama, debtor’s prison does not exist.

But, we are, admittedly, talking about a, from an individual point of view, black swan event. In most cases, we go to graduate school and we wind up getting jobs after graduate school, and not only do we get jobs, but they tend to pay better than our old jobs did. We build houses with white picket fences, have 2.3 children, and live happily ever after.

What tends to happen is that we follow our hearts instead of our heads. We get sucked into the allure of being able to put “MBA” in our signature lines (by the way, have you noticed that NO graduate of Harvard Business School puts “John Smith, MBA” in his signature line?!? Putting that in your signature line is a surefire indication that I would never, ever, ever hire you to do anything for me, as you’re touting that the pinnacle in your professional life was getting a diploma) and off we go to graduate school, Sallie Mae paperwork tagging along in the breeze.

What do the numbers actually tell us about this decision, though?

To answer this question, I decided to set up a Monte Carlo simulation to evaluate the range of outcomes of one prospective case. "What’s Monte Carlo?", you may ask, "besides a ritzy casino that has self-cleaning toilets?". Because the world either has an infinite range of outcomes – think of picking a point along a line; you could pick an infinite number of points – or an exceptionally high number of outcomes – how much money will you earn in your life has a finite set of outcomes, but probably numbers in the hundreds of millions or billions of outcomes – it’s impossible to create the one equation to rule them all and solve for an average expected outcome. Instead, we pick random outcomes from the set of all outcomes to estimate what could happen. In this case, I ran 1,000 potential future scenarios.

I looked at a 25 year old with a $0 net worth. I know. Most 25 year olds have a negative net worth, but this also can serve as a baseline case. This 25 year old faces two choices: stick at his/her job for the next 40 years or stop working, go to graduate school for 2 years, and then face the job market and work until age 65.

I also had to make some assumptions about this person’s behavior and the world around him to keep from creating a behemoth untenable model from Hades.

- Pay raises were matched to inflation. I know this isn’t really the case in the real world. Some people do better than others.

- This person saved 10% of his income. If he did not have negative net worth, then the money was invested in the S&P 500; if he had negative net worth (from graduate school), then the money went to paying off the principal of the loan until he hit $0 net worth.

- I randomized inflation from historical inflation rates since 1914. Even though inflation since 1990 has been lower and less volatile, I didn’t want to artificially depress inflation.

- I used S&P 500 returns since 1871 to create a BetaPERT distribution. For those of you who don’t know what that means, I simply created a lowest possible return and a highest possible return and used the average return and average volatility of annual returns to give my random number generator a range to pick from. Annual returns could be no higher than 56.79%, no lower than -44.20%, and would average 10.60%.

We also have to make some assumptions about what our typical person is making, would pay for graduate school, and what chances he’d have of getting a better job after graduate school. For this information, I turned to the Bureau of Labor and Statistics for data about how workers with bachelor’s degrees compare to their higher educated master’s counterparts.

Based on the BLS’s data, we know a few things about our educated workforce:

- If you have a bachelor’s degree, your average salary is $55,432. To keep the random number generator from selecting some wild salary like $0.03 per year or ONE HUNDRED BILLION DOLLARS, I said that our person could have been earning between $25,000 and $100,000 per year, with the average salary matching the BLS’s numbers.

- If you have a master’s degree, your average salary is $67,600. Again, I put some boundaries on what the random number generator could spit out, limiting our first year post-grad salary to between $30,000 and $150,000.

- The unemployment rate of undergrad degree holders is 4.5% and the unemployment rate of master’s degree holders is 3.5%.

Since our hypothetical person already has a job, he’s not in the 4.5% who are currently seeking work. Therefore, I created three possible outcomes for graduate school and, doing some inferring from the BLS’s data – since their data didn’t reveal the employment outcomes of people who had jobs and then quit to go to graduate school – determined the probabilities of each.

- Graduate from grad school and get a job with a master’s level salary: 78%

- Graduate from grad school and get a job with a bachelor’s level salary: 21.2%

- Graduate from grad school and no soup for you: 0.8%. Note: to prevent myself from having a horrendous problem with Markov chains, I made the assumption that if our graduate got the unlucky roll of the dice, he’d find a job in year 2, either at bachelor’s or master’s level pay. I realize this might not be quite realistic, since once you’re out of a job, it’s incrementally harder to get back into the workforce.

Finally, I estimated the average cost of graduate education to be $43,800. I figured our grad student did enough TA work to pay for all other non-education related costs in his life.

Yeah, yeah. tl;dr with all of the methodology junk. What was the outcome?!?

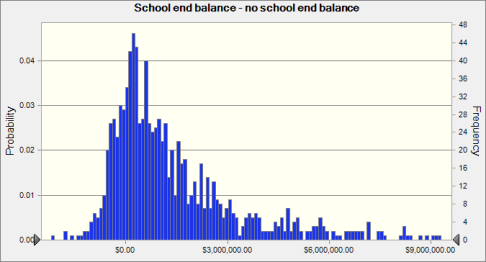

It’s no surprise that the results tend to stack up right around the “slightly better off” area. The range of outcomes was that the 25 year old went from being $2.2 million worse off to $27 million better off for having gone to graduate school.

The interesting part of the data gives us an opportunity to explore the difference between mean and median results. The mean, or the average, was the sum of all of the outcomes divided by 1,000. Since we had a few cases where our 25 year old did exceptionally well by going to graduate school which were not balanced out by his relatively uneducated counterpart doing equally as well, the mean of the outcomes was a $1.62 million improvement.

Don’t let your limbic system (what I call Monkey Brain on my site) see that number and run off to apply to every graduate school you can find. There’s more to this story.

The median number makes us think twice. The median is the dead middle point of outcomes: 50% of the outcomes are better off and 50% are worse off. In this case, the median value is $810k, half of the mean outcome. Furthermore, 20% of the people who went to graduate school wound up worse off financially for having taken the time off to go back.

Going back to grad school, according to the simulations I ran, should make the average 25 year old that I created better off in the long run. There are some caveats to this decision, though:

- The higher the undergrad salary, the less sense the decision makes. The financial purpose of going to graduate school is to create an incremental bump in salary. This usually happens for either career changers or for people who work in places like the government, where if you have an advanced degree you get paid more.

- Graduate school outcomes were best for cases where the graduate school salary was significantly better than the undergraduate salary. This is the corollary to the first caveat. If you’re making $50k per year, go to grad school, rack up the debt, hang out for a year afterwards working as a Starbucks barista because you can’t find a job, and then get a $40k per year job afterwards just to take anything, you’re tethering yourself to that new salary, and the reality is that it’s difficult to escape. HR wonks love to ask you what your previous salary was because it creates an anchoring effect. If it was high, they can come up with excuses like cost of living or improved culture/better workplace environment to drive your salary expectations down, and if it was lower than what they were planning on offering, they can just offer you a slight increase to make you happier. You’re better off bargaining from a position of strength unless you have a story to tell, like “I was a starving artist, and then I went to Harvard Business School, where I became a quant jock and now can model corporate financial meltdowns with a 99.38% accuracy.”

- Brand matters. This isn’t Polo, where a pony irrationally drives up the price of a shirt. This is a world where money is given to you based on a hirer’s impression of the job you can do for them. Since these hirers have never seen you before and don’t know you from Adam’s cat (in most cases), they have to use proxies to determine your likelihood of creating incremental value for them. One is your resume, but if, as described above, you’re a career changer, then you’re going to need another proxy to speak for you. Success at a name brand school serves that function.

- What you study matters. This is purely a matter of economics. If there’s marketplace demand, then there’s going to be a higher price for whatever is offered. Almost nobody wants a 13th century Antarctic literature specialist, no matter how many degrees of authority academia has conferred upon that person. If you have a solid understanding of how, for example, to build an interstate bridge that won’t collapse when the wind blows or when there is a large amount of vehicular traffic put upon it, then you’ll likely find a place in the world to practice your skills and be handsomely rewarded for such capabilities.

Since leading units of tanks doesn’t have much of an analogous application in the civilian world, I decided to go to law school at the University of Virginia. After a year, I was lured over to their next door neighbor, the business school, and I, calculating the opportunity cost of a 4th year in a JD/MBA program and shuddering at the loss, decided to only get my MBA. (No, I don’t sign my name "Jason Hull, MBA.") Within 2 years, I’d paid off my student loans, which enabled me to start a software development company that I later sold.

This leads me to one final thought about the pursuit of academics for the sake of enrichment. I’ve read many of the classics and thoroughly enjoyed them, and I didn’t need an advanced degree in classical literature to enjoy them. I decided, as an encore career, to become a financial planner for many reasons that are documented at my website. I paid for the educational requirements from NYU to sit for the CFP® exam myself, mainly because the topic was really interesting to me. I pursued my current career path somewhat out of academic curiosity; where else do I get to build models to answer questions about the possible outcomes of people’s lives and figure out the steps to take to improve that range of outcomes? However, to get to this point, I was ruthlessly economically driven. Financial Independence allows you the time, freedom, and financial flexibility to pursue your academic interests if you so desire. There is no entitlement in the world for going to school to pursue your PhD in 13th century Antarctic literature and then expecting your student loans to be forgiven by the government after you couldn’t find a job because you chose a field of study that had no practical application in the real world. Go out, make your way, make a mark, earn your living, create value, and then either pursue those studies of “academic interest” on the side because they interest you, or study them when you are financially set enough to be able to support yourself in your pursuits.

Jason Hull. Jason Hull is a candidate for the CFP(R) Board's certification, is a Series 65 securities license holder, and owns Hull Financial Planning. He is also a personal finance columnist for U.S. News & World Report.