In the 2022 Survey of Consumer Finances, the average household reported $10,196.19 in education debt, while the median household reported $0 in student loans. Only 21.7% of households reported carrying any student debt at all.

Before we continue, though, I need to note the SCF doesn't give us a full snapshot of the data. While very useful for seeing the household distribution of debt, the SCF is strained on the student loan front – neglecting to include student debt from a few important populations.

Let's talk about student debt in America, as measured by the Survey of Consumer Finances, the New York Fed's Household Debt and Credit Report, and the Federal Reserve's G.19 credit report.

Student Loan Debt Statistics in America

Student loan debt is some of the trickiest debt to pin down. Due to survey design and sourcing, the three primary surveys in the United States disagree on how much student loan debt is out there.

I'll primarily use the Federal Reserve SCF in this post. Its microdata is the richest and the most accessible for our purposes. However, let's first look at aggregate student debt stats from the New York Fed and the Fed's G.19 survey and discuss what we find.

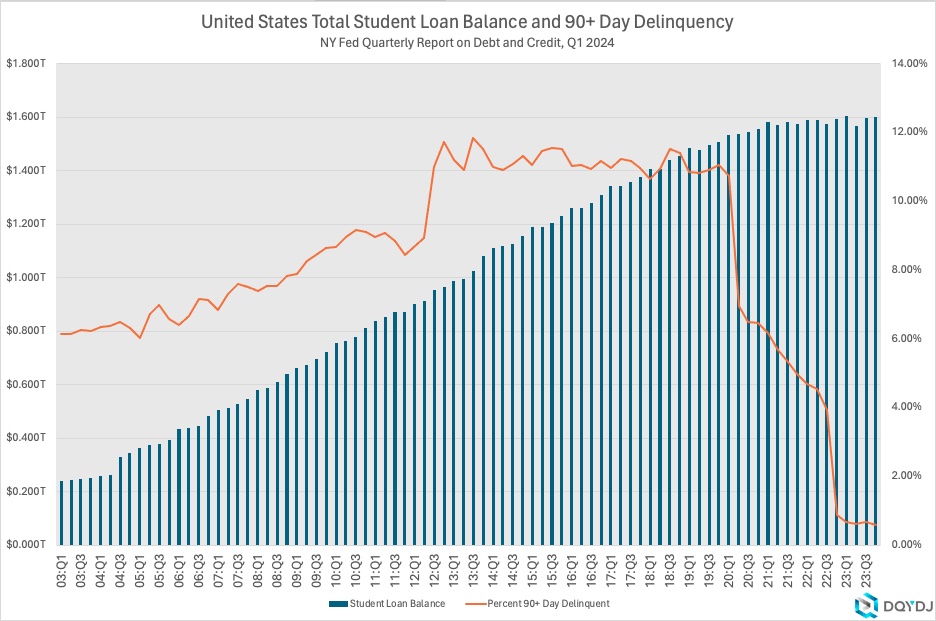

New York Fed Household Debt and Credit Report

The New York Fed Household Debt and Credit report from Q1 2024 implies about $1.601 trillion in student loan debt outstanding.

Currently, .6% of that balance is considered 90+ days delinquent. Note that those delinquency numbers are lower than you might expect because of a series of changes in student loan servicing policies since the COVID pandemic. This graph shows the effect those policies have had on delinquency rates.

The New York Fed's data uses a random 5% sample of Equifax credit reports to compute student loan debt. It's likely pretty accurate – although it may double count student loans during transfers or similar events or miss some older loans.

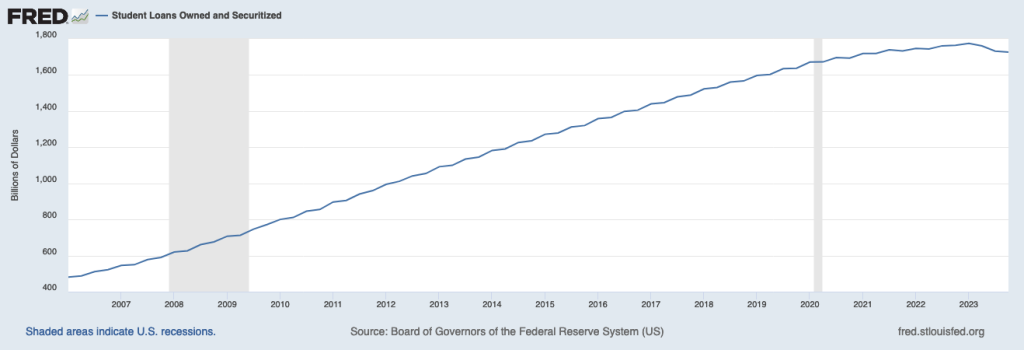

Federal Reserve G.19 Student Loan Debt

In Q4 2023, the Federal Reserve's G.19 credit report implied $1.727 trillion in student loans outstanding.

The G.19 gives us the highest estimate of the three surveys. It includes survey data from student loan debt holders – banks, finance companies, and the Federal Government – and, as you can see, has the most pessimistic view of US student loan debt.

Taking the G.19 worst case student loan total and the 2022 SCF's estimate of 131,306,389 households (technically, PEUs), the average household would hold around $13,153.97 in student loan debt.

The Survey of Consumer Finances

In 2022, the Survey of Consumer Finances implied around $1.339 trillion in educational debt outstanding.

As you can see, the SCF underestimates the Federal Reserve G19's total student debt outstanding by roughly 25%. (Read about the SCF underestimating debt here and here.)

From a footnote in Bricker et. al, 2015 (linked above):

The core is typically the economically dominant single person or couple in the household, plus all other people in the household that are economically interdependent with that single person or couple. In this way, a young adult who is renting a house with roommates will be included in the economic core, but her roommates likely will not be. Likewise, an adult child living at home with her parents but with otherwise independent finances will not be included in the family.

Additionally, we don't see data from dorms: "...the frame for the SCF excludes institutional residences, including college dorms." And I don't know about you, but I held student debt when I was a freshman in a college dorm.

But it's not all grim on the statistics front. The three main sources all grow at around the same rate. That means the SCF is still useful for student loan stats, but you need to keep its blind spots in mind.

Student Loan Debt Statistics by Percentile

Again, the SCF implies that only 21.7% of households – or Primary Economic Units – hold any student loan debt at all. Here are the student loan debt breakpoints for selected percentiles of households:

| Student Loan Debt Percentile | Student Loan Balance |

| 1-49% | $0.00 |

| 50% | $0.00 |

| 75% | $0.00 |

| 80% | $3,000 |

| 85% | $12,000 |

| 90% | $28,000 |

| 95% | $63,000 |

| 96% | $78,000 |

| 97% | $91,000 |

| 98% | $112,000 |

| 99% | $180,000 |

Example of how to read this: "3% of American households have $91,000 or more in student loan debt"

Remember, this is a snapshot of current student educational debt. All the caveats I laid out in the aggregate section apply here. It does not show the whole universe of loans or stats for households that have already paid off their debt. It is not anticipating future loans, either. It's a snapshot of a moment in time.

Age 25-40 Households and Student Loan Debt

In this section, I'll zoom in on households headed by someone aged 25-40. This cohort averaged $17,912.98 in student loan debt in the 2022 SCF, and 39.8% of households reported holding a balance greater than $0.

Student loan debt is concentrated among younger folks. These households held an estimated $599 billion in student loans, or 44.8% of all student loans. (This cohort represented 25.5% of households in the 2022 SCF).

Here is the student loan percentile chart only for households led by someone age 25 - 40:

| Student Loan Percentile | Student Loan Balance |

| 1% | $0.00 |

| 50% | $0.00 |

| 75% | $15,000 |

| 80% | $20,000 |

| 85% | $32,000 |

| 90% | $50,000 |

| 95% | $88,600 |

| 96% | $99,000 |

| 97% | $107,000 |

| 98% | $166,000 |

| 99% | $300,000 |

Example of how to read this: "2% of American households headed by someone age 25-40 have $166,000 or more in student loan debt"

Student loan forgiveness

As Joe Biden was last running for President in 2020, one topic that captured the popular imagination was student loan forgiveness.

In Biden v. Nebraska, the Supreme Court ruled (6-3) that the Biden Administration could not cancel up to $400 billion in student loans. The administration, however, has persisted in forgiving student loan debt in certain categories. As I went to press, the Biden Administration had made 3.9 million borrowers eligible for debt cancellation, totaling $138 billion in potential loans. Additionally, the Administration announced another 78,000 public service workers were eligible for forgiveness, with loan amounts totaling $6 billion.

We'll see how much of a difference these Executive actions make in the next version of this post.

How many households could pay off their student loans?

Another way to look at student loan debt is to see what percentage of households could pay off their student loans if they had to. A crude way to do that is to look at how many households have both a positive net worth and positive student loan debt.

Around 16.3% of households – 21.4 million or so – have student debt along with a positive (or $0) net worth. About 75.2% of households with student loan debt have a $0 or higher net worth overall. Compare that number to the overall net worth statistics.

Of course, caveats apply. This doesn't account for liquidity. For example, these households may be unable to liquidate a house or a privately held business easily.

Student Loan Debt by Generation

As you might imagine, student loan debt heavily falls on Millennials and Generation X. Nearly 40% of Millennial households have an active student loan balance – and another 26% of Generation X households:

| Generation | Average | 25th Percentile | Median | 75th Percentile | Percentage with Debt |

| Millennial | $18,421.38 | $0.00 | $0.00 | $15,000 | 39.78% |

| Generation X | $13,035.11 | $0.00 | $0.00 | $1,900.00 | 25.82% |

| Baby Boomer | $4,248.07 | $0.00 | $0.00 | $0.00 | 7.1% |

| Silent | $604.376 | $0.00 | $0.00 | $0.00 | .23% |

Wondering my chosen split of generations? And remember: these are for survey responses in 2022 and 2023.

- Millennial (21-40 years old)

- Gen X (41-57)

- Baby Boomer (58-77)

- Silent (78-94)

Student Loan Debt by Income Bracket

Student loans are not only skewed by age but also by income. In fact, student loans are biased – quite a bit – to upper incomes. Here is the chart for the average student loan debt by household for the entire universe of households ranked by income percentile:

| Income Percentile (%) | All Households | Age 25-40 Households |

| 0-9.9 | $3,392.81 | $5,408.85 |

| 10-19.9 | $5,175.09 | $6,609.82 |

| 20-29.9 | $6,619.59 | $10,946.30 |

| 30-39.9 | $5,958.56 | $13,100.86 |

| 40-49.9 | $8,765.09 | $14,974.00 |

| 50-59.9 | $10,940.88 | $14,772.98 |

| 60-69.9 | $13,842.86 | $18,294.17 |

| 70-79.9 | $13,333.26 | $21,015.16 |

| 80-89.9 | $19,834.86 | $46,538.19 |

| 90-94.9 | $17,644.24 | $29,466.92 |

| 95-98.9 | $11,968.63 | $24,701.42 |

| 99-100 | $4,894.84 | $34,901.35 |

In the table, income brackets are based on all households. The column with households headed by someone aged 25-40 is of households who fit that criteria amongst all households. So, for example, you can say, "Among households headed by someone age 25-40 in the top 1% of all incomes, the average student loan debt was $34,901.35".

Student Loan Debt in America

Student loan debt is a complicated topic. Younger households indeed tend to hold student loan debt. It's also true that higher-income households hold student loan debt. And that's how the system is designed to work.

College is marketed as a way to earn more. If true, we'd expect higher-income people to have more student loan debt!

The fact that there are households with loans that don't crack the upper-income brackets is a symptom of something. If the system worked as promised, would we expect so many households with student loan debt in the lowest 10% of the income distribution?