Editor: we originally wrote this as a four part blog post in June 2009, only a few months after we started the site.

The ACA passed and is the law of the land, but we're leaving our contrary post up (and merged to one post) for posterity. Enjoy a snapshot in time!

Part 1: Lies, Damn Lies, and Statistics

45.7 Million in America Are Uninsured

"There are three kinds of lies: lies, damned lies, and statistics." -Benjamin Disraeli

Where did the estimate of 46 million people in America without health insurance come from? You probably have health insurance through your employer or through some other means. However, there are people in this country without insurance. What does it mean, and why is the number's background not nearly as scary as the number itself? Read on...

The Can of Worms

I will not use this article to suggest an effective health care reform. I strongly believe that there are efficiencies in the health care system which are not being realized. Most likely, I will follow up with another article discussion other aspects of health care reform. However (!), this specific article is meant to solely address the most commonly repeated fact in the health care debate- the question of how many people are without health insurance and why. Whew... read on.

Heavily Quoted, Lightly Understood

Both President Obama and Christina Romer, the White House Council of Economic Advisors Chair, have made statements to the effect that there are 46 million uninsured in the United States. Where exactly did this number come from? In August 2008, the U.S. Census Bureau released this report (I highly suggest that you at least skim this report, start on page 27) reporting that there are 45.7 million people in America who do (did?) not currently have health insurance. There is no question to the stastistical accuracy of the samping... as page 9 states, all comparative statements are significant at a greater than 90% confidence interval (again, unless it is stated it isn't).

Break it Down

45.7 million people in America had insurance. Note I said "people in America", not Americans... the report is a statistical sampling of people in America, but not specifically American citizens. This is an important point, and one that speakers have been careful to dissemenate accurately. If you parse the speeches which mention the 46 million number, you will note that the speaker will never say "American citizens."

According to the article, 15.3% are without health insurance, down from 15.8% in 2006. In 2006, 47 million people in America were estimated without health insurance. In 2007, 253.4 million people had health insurance, up from 249.8 million the previous year. Furthermore, the government provides coverage for 83 million people, and 202 million had private insurance (yes, there is an overlap).

Our total population considered in this study is 299.1 million. 45.7 / 299.1 does equal 15.28%. Still, who comprises the 45.7 million? Is 46 million a number which denotes people without insurance for a whole year? Do they even want health insurance? How many non-Americans are included in that total?

The Census has a disclaimer in the report which states it over reports the number of uninsured chronically (page 27) and that you should take a look at a CBO report, and a Survey of Income and Program Participation Working Paper (#243, June 2004). This report is the CBO report from 2003. They report a number between 21 and 31 million who can't get insurance for an entire year. Here is the Working Paper.

Judging the 'want' of people and their health insurance is hard to say. According to the report, the real median household income in the United States was $50,233 in 2007. Knowing half of households made more means we can perhaps look at the uninsured stats by income and take a guess who could afford health insurance. There were 17.603 million people in households making more than $50,000 who were uninsured. This leaves 28.1 million uninsured but perhaps wanting insurance, or (28.1 / 299.1 =) 9.4%.

9.737 million uninsured are non-citizens, and would not be covered under any health care overhaul anyway. 22,214 million people total are non-citizens. There are (299.1 - 22.2 =) 276.9 million citizens in this scenario, leaving (36 / 276.9 =) 13.0% of citizens uninsured.

Parsing the Rhetoric

The most important number, which also happens to be the most unclear, is the number of American citizens who chronically cannot receive health insurance. There are other ways to slice the data... there is a large number of younger people in America who do not have health insurance, for example. Any reform should concentrate its resources not on the headline '45.7' million number, but a vastly smaller number. The disagreement about a Government-run solution versus a market solution will continue even with clearer statistics, but keep in mind how these numbers are being twisted the next time you hear them repeated as fact.

Now that that's over with, I'll get ready for some more articles on the subject. Eventually, I'll discuss why any public plan will overrun its budget in short order. After that, I'll write about how the market can be harnessed to provide the care we desire for the underserved. Sit tight.

Part 2: The Problem with Estimates

No matter what the final estimate for Health Care reform is, it will cost a lot more.

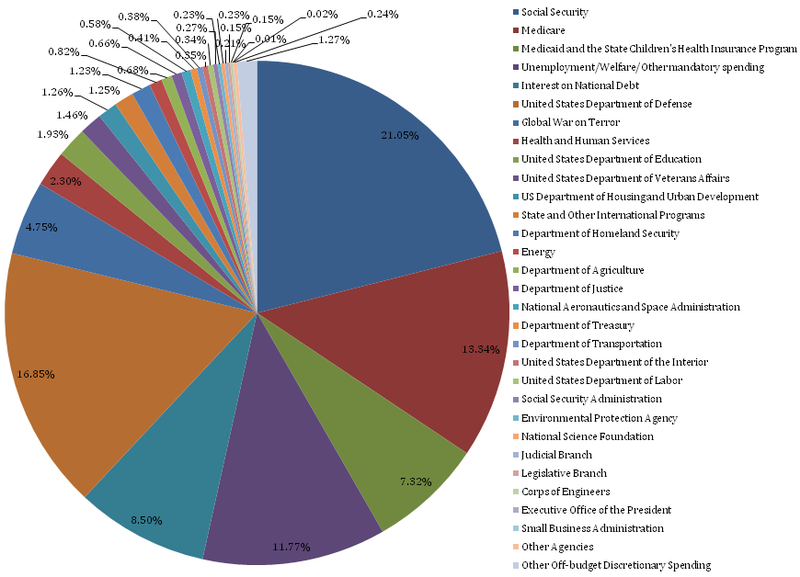

The bills being written already carry price tags so high it’s mind boggling… $1 trillion over ten years, even $1.6 trillion over ten years. A large number like that seems to convey honesty and straight-talk, yet probably only scratches the surface of what will be a much higher bill. Recall: Social Security was sold to the American public as a 1% tax on the employee and employer, scaling up to 3% on each in 1948. How close are the rates to 3% now? Well, employers and employees both pay 6.2% in tax and Social Security is now the largest expenditure in the federal budget.

No, Walter, You’re Not Wrong...

This article’s point is only to illustrate the cost difficulties any attempts by congress to reform health care will have. It is not to push for any specific health care overhaul plan. There is much inefficiency in the current system which definitely need to be ironed out. Future health care articles by me will probably cover the things this article is lacking.

Myth, Legend, and Lore

What do you think of when you think of ‘Socialized Medicine’? Probably cradle to the grave care in Scandinavia, or some other European country. Setting aside the fact the word Socialized is almost a dirty word, note that in America it has come to mean ‘Run by the Government’. It doesn’t matter what the word’s actual definition is, Socialized Medicine boils down to a health plan in which people pay the government in order to facilitate health insurance.

There is already government run medicine here. At the federal level, there are at least four Government health care plans today. The Veteran’s Administration, Medicare, Medicaid, and the State Children’s Health Insurance Program. Going back to the Census document I used in my previous article, you can see that Government run programs already insure 27.8% of people in America.

Massachusetts: The Lessons Learned

One state has already passed a universal health care mandate (2006). Massachusetts Senator Ted Kennedy is helping craft one of the reform bills using Massachusetts as a guide. However, tough times in the state (and nation, obviously) have led to some tough decisions in the plan- to the tune of $115 million in cuts. Massachusetts already is running $75 million over budget in 2009, even after a budget with 1/3 more spending than 2008 (which itself was almost 50% over budget). Is this the sort of program we want to extend to a national scale?

Debunking Another Myth

Medicare covered 13.8% of people in the country in 2007 (Medicaid covered . Medicare is a Government run health plan, which has all of the qualities which are held up as desirable in any public-option health care overhaul. It can set its own rates, it is easy to qualify for and its relatively cheap for the insurees. Wouldn’t it then be a great example of how Government could run a public health care?

No, and no one would make that claim. President Obama has already proposed $600 billion in cuts to Medicare and Medicaid over the next decade to help pay for health care reform. If we want to have a public option, doesn’t that seem like taking money from your left hand to give to your right? A further study for your consideration: the Pacific Research Institute reports than Medicare spending has increased 34% more per patient than other forms of insurance since 1970. If government medicine can’t control it’s own costs now, where does the idea that government will reduce waste in medicine come from? Ben Franklin (or was it Rita Mae Brown?) once said, “The definition of insanity is doing the same thing over and over and expecting different results.”

When Herrings are Red

“Well, the government runs the military,” is often used as an argument for a government run health insurance. This is just purposeful redirection, ‘ignoratio elenchi.’ It's a complete non-sequitur. The U.S. Constitution, Article I, Section 8 provides the government with the right to raise a military. There is no such entry for ‘health care’. Military and Defense spending is an externality… a single person's needs for national defense are way too low to give it much thought. The need of an individual for health insurance is a whole different ballgame. Controlling externalities is a necessary function of government. There is no comparable argument for government run health care.

Also, there is the question of scale. The United States Military is, bar none, the greatest fighting force in the world. The military consists of 1,473,900 active duty personnel and 848,056 reserve personnel stationed at around 820 installations. "Pretty big," you might say. On the other hand, the United States consists of 307,212,123 people!

Let It Be Summarized!

As I stated in my last article on this issue, I believe something should be done to fix the health care problems in our country. I question whether a ‘Public Option’ is the right prescription to nurse our health care system back to health (how about them metaphors?). Discussing the vast costs and the best method to insure more people isn’t an issue that should be taken lightly, and probably shouldn’t be forced through our legislative system at warp speed. Regardless, change is necessary, so this debate is a healthy one to have. Let's keep it going.

Part 3: Stacking the Deck

Government participation in the private insurance market is a trojan horse for a single payer system.

The debate that needs to happen is not private options versus a public option in insurance, it's private options versus a single payer system. No, private insurance will never go away completely, but any public option will soon become much larger then originally planned under a public option. Private insurance will become relegated to supplemental programs which build on top of (and react to the inefficiencies of) a government run plan.

The Can of Worms is Open

Of this series of articles that I have been writing, this is likely to be the most controversial. Yes, I know there is potentially a series of restrictions that could be placed on any public option which would prevent it from growing 'too' (however you define it) large. I do not believe that these restrictions would be properly formed in any bill that emerges. Any monopsony (which is what a public option is) that dictates prices to sellers creates price distortions which will be passed on to private plans (just like Medicare today) which eventually will be forced to leave the market since there are no more profits to make.

Really? Private Plans Can Compete With Government?

A thought exercise for your consideration:

You are considering starting a widget factory. You are highly trained in widget making and administration, but you are an unknown commodity in the widget community.

There is one other widget maker in the world, UncleSamCo. UncleSamCo, historically, has run their widget making assembly line inefficiently. However, UncleSamCo has some interesting abilities. Even though it is inefficient, it can make up for losses by printing money. It can dictate prices to the suppliers of raw materials. Its huge size allows it to borrow money at a very low rate. It has the ability to levy taxes. Can you compete in this market?

The answer, of course, is a resounding no. Is there a way to control for all of these anticompetitive advantages? Most likely the answer is yes, but in practice there will not be a control. The cost of debt is already a major disadvantage. Glance at the borrowing costs for Humana, WellPoint, and Aetna (The Investing in Bonds site doesn't allow these prices to be quoted on external sites). Note their long term bonds all trade over 6.25%. How about for the government? As of 6/26, the yield on 30 year treasuries was estimated at 4.30%. How can a private company compete with an entity that can borrow at 2% less over the long term, and can even levy taxes (or cause inflation)?

Fundamentally, to allow competition in this 'market hybrid' based solution, it would be equivalent to tying the government's hands behind its back. If we want to allow a single payer system, let us discuss it on its merits. Pretending the public option is anything less is disingenuous.

How the Crowd Out Would Proceed

Any health care reform will be paid for by some combination of an increase in taxes on current medical benefits, mandated coverage (the healthy subsidize the unhealthy to a degree), additional taxes on loosely related items (say, cigarettes or unhealthy food), and cost savings from supposed efficiency increases. On their own, any of these options have their supporters and detractors. However, I will assume that in any bill that comes to a vote will contain both:

- Some form of taxes on current health care (maybe over a certain premium price)

- Mandated enrollment

(You may not like those assumptions; please leave your both your comments and complaints).

- The public option will begin, and insure a small subset of the general population as planned.

- The public option will reimburse for procedures and doctors at a rate lower than current private plans (this is the biggest assumption, but Medicare does this now)

- The disparity between private and public plan reimbursement rates will increase as private plans pay the difference in the true costs of practicing medicine. This eventually will drive up the premiums of private plans.

- Premium price increases will cause additional taxation of benefits (the idea behind the taxes is to start taxing once a certain plan cost is hit) and companies will slowly start to scale back their investment in corporate plans.

- As more and more companies drop their private plans, the remaining plans will become more expensive as they are now subsidizing more people on the public plans.

- Eventually, company purchased health care will become an anachronism... only highly compensated employees will retain private plans.

Is this all bad? Maybe, maybe not. I will not use this article to discuss what I feel could allow a market based system to work (maybe next?). I only wish to argue that a public option will quickly become the option for the vast majority of people. The Lewin Group estimates that a public plan would mean a reduction of 119.1 million people on private insurance, and an increase of 131.2 million people on the public plan. What about the private insurers left? Read on.

Two Solutions to Scarce Resources

No matter how you frame the problem or your opinions on the subject, there is no way to deny that that medical care is a scarce resource. There are exactly two ways to allocate scarce resources:

- Allow the market to set the price of resources accordingly

- Ration the resources accordingly.

If the United States population has decided a market based solution will never work, necessarily the burden of allocating medical care will fall to the second option. This is where I see the private insurance market competing... again, assuming doctors aren't forced to practice in the public system. If a doctor feels his value would be more in a private system, he could opt out of the public system and work for a private plan. These private plans would exist, like they do in Italy today, to cover things above and beyond what a public option offers - whether in type of medical solution, or to compete on speed. In this style of system, basic needs could be met under a public plan, with supplemental coverage offered in the market.

Of course, if doctors are mandated to practice in the public option, this creates the potential for a black market in medical care.

Who's Right?

I'll leave that for the reader to decide. I hope I have convinced you that the argument is actually private versus single payer, instead of what has been disseminated widely as a public option. As the population of the greatest country in the world, (I know, I know, 'citation needed'. We're certainly not in soccer!) we are qualified to discuss the balance between the access to care and the cost of care without the options on the table being shrouded in mystery. Let's have this conversation in a logical, reasonable manner.

Part 4: The Prescription

In my mind there are two issues that need to be addressed in any successful health care overhaul. First, costs have to come down so health care stops costing $7,900 per person and increasing at a rate faster than inflation. Second, access to health care needs to be expanded to include the 21 to 46 million people without insurance. Since it is commonly accepted that the health care system needs an overhaul, what should that overhaul look like?

The Advantages of Government

There are two elephants in the room (if some are hiding and I can't see them, let me know in the comments section) which the market has little incentive to deal with.

- It is in an insurance company's best interest to avoid people with chronic diseases and conditions. Once a chronic condition is identified, that person's cost to the insurance company is known to be greater, on average, than a person without that condition.

- Preventative medicine doesn't pay the bills. Our medical system reimburses more for procedures and tests than physicals and diet plans. Additionally, insurance companies know that their customers may switch plans. This strangely creates a disincentive to offer more preventative services; another company can merely not offer the same benefit yet offer a cheaper overall package. This means that diet, exercise, and other similar programs get the shaft.

In the case of pre-existing conditions, insurance companies have no incentive to allow people with a diagnosis of a chronic condition to join the plan. Insurance companies also have the perverse incentive to not encourage preventative care because people can leave the plan. This is especially awkward because healthier people tend to be cheaper for insurance companies. These conditions will probably need some 'Congressional Intervention' to solve. Coverage mandates and some minimum preventative programs are in our future.

Solutions in the Public Domain I Love

There are two generalizations which may as well be facts when it comes to costs. First is you will cost more in the future than you do now. Second is that smoking and diabetes (type 2) are (generally) preventable. The first is just life... as we age, we have more conditions which cost more to treat. The second means that we can have an effect on our future health by changing our behavior today.

A complaint about current High Deductible Health Plans (I am in a HDHP) is that too many young, healthy individuals join these plans, driving up the cost for people in 'classic' premium/copay plans. I love the idea of HDHPs, many reimburse 100% for preventative medicine, and additional procedures, visits, and tests are at the insurance company rate (which is lower than the billable rate for a walk-in). The beauty of the plan is, on the off-chance something very expensive (medically) happens to a holder of the plan, they will be saved from bankruptcy- another request of President Obama in any health care overhaul. HDHPs do exactly that... they take bankruptcy out of the equation. Fundamentally, HDHPs are catastrophe insurance.

How do you hedge against future costs? 21-year-old Joe Sixpack won't have his sixpack forever. He will eventually need more than the occasional antibiotic. Here is an informative description of the Cato Institute's plan which would attempt to solve this issue. The link to the full report is here. The idea revolves around the use of "Health-Status" insurance, which is insurance for a premium rate change. If Joe Sixpack develops a chronic condition, this Health-Status insurance will kick in. This sort of a private market solution goes a long way to addressing the pre-existing condition 'elephant' mentioned above as well.

In car insurance, Joe Sixpack is perhaps the riskiest demographic to insure. Unmarried 21-year-olds require more reimbursements from car insurance companies. Older drivers (and females) don't tend to behave in the same way behind the wheel, and cost less to insure. Many factors affect car insurance rates... number of recent accidents, age, type of car, number of tickets... and the private market classifies these risks correctly and adjusts rates accordingly.

In health care, if Joe Sixpack joins a premium based plan at work, he pays the same amount as Steven Kegger, a

54-year-old smoker with type II diabetes who is 80 pounds overweight (these people are made up, get off Google!). The risk of various lifestyle factors is disconnected with the price of insuring those same behaviors. If there were less onerous regulations on health care companies to be risk-blind, markets would be more efficient. Recently, the Wall Street Journal ran an editorial about Safeway (for our non-California readers, it's a supermarket) and how their health insurance is structured. By incentivizing' good behavior (or penalizing bad, as the case may be) Safeway has managed to keep their costs under control. If it's okay to increase the tax on cigarettes, for example, why is it not okay to assign costs based on lifestyle choices? I would never advocate forcing people to stop their bad habits (I certainly lean Libertarian in that regard). However, I believe the market needs to price this behavioral risk accordingly.

A Note About Price Transparency

If I want to purchase car insurance, I can go to any number of web sites and get an accurate, comparable quote. If I want to purchase life insurance, ditto (and they are allowed to adjust for behavioral choices... weird). If I want to purchase health insurance, it's close to impossible to compare the true costs across plans. With any health care overhaul, this needs to change. True price transparency will allow consumers to see what plan is actually better. Medical care is the same way... think about it. How much is a vaccine? An office visit? A hip replacement? Price transparency is an important step towards any successful overhaul.

Fix It.

Here we are, approximately 4,000 words later. Congratulations, you made it! Now what?

I hope I have convinced you that the statistics are wrong, the costs of government care will be huge, the 'public option' is actually a single payer system, and a market based solution is the best solution. Health care reform is a serious and timely issue, and I hope to see this country approach it in the correct way. Removing the perverse incentives in the market and allowing efficiency to reign supreme will allow the best medical plan to shine through.