Annually, the IRS sets a maximum IRA contribution limits based on inflation (measured by CPI). There are limits for an individual contribution and an age 50+ catch-up contribution. Since 1998, non-working spouses can also contribute up to the same limit as an individual.

Whether an IRA is deductible or not is determined by a separate IRS formula. Even if you are above IRS limits to deduct an IRA or contribute to a Roth IRA, you can still contribute to a non-deductible IRA.

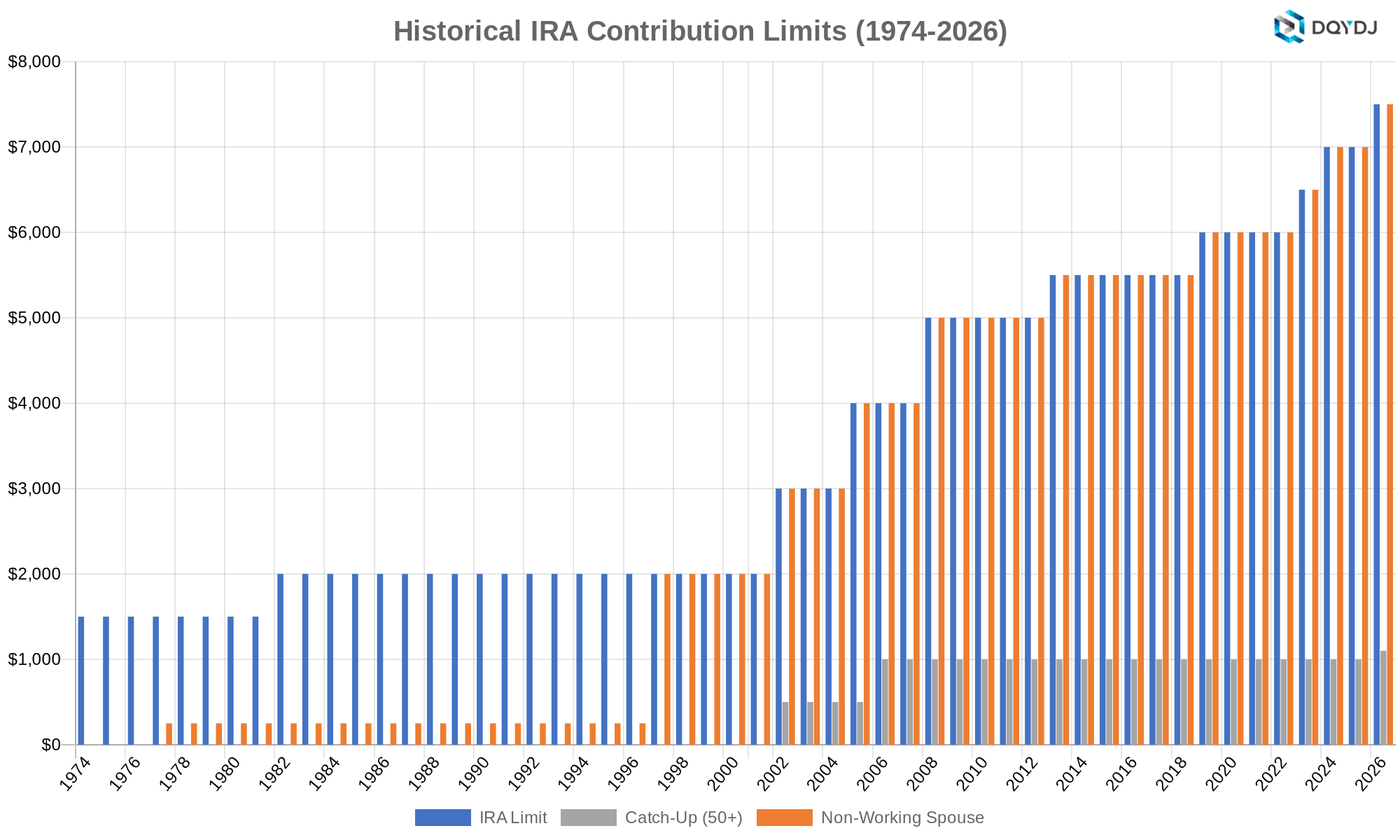

What is the IRA contribution limit in 2026?

IRAs in 2026 have an individual contribution limit of $7,500, up from $7,000 in 2025. An additional $1,100 is allowed for earners 50+ years old, up from $1,000 in 2025.

A non-working spouse can also contribute up to $7,500.

These limits presume you, or you are your spouse, are reporting earned income on your tax return.

The History of the IRA Contribution Limit and Non-Working Spouse Contribution (1974-2026)

| Year | IRA Limit | Catch-Up (50+) | Non-Working Spouse |

|---|---|---|---|

| 2026 | $7,500 | $1,100 | $7,500 |

| 2025 | $7,000 | $1,000 | $7,000 |

| 2024 | $7,000 | $1,000 | $7,000 |

| 2023 | $6,500 | $1,000 | $6,500 |

| 2022 | $6,000 | $1,000 | $6,000 |

| 2021 | $6,000 | $1,000 | $6,000 |

| 2020 | $6,000 | $1,000 | $6,000 |

| 2019 | $6,000 | $1,000 | $6,000 |

| 2018 | $5,500 | $1,000 | $5,500 |

| 2017 | $5,500 | $1,000 | $5,500 |

| 2016 | $5,500 | $1,000 | $5,500 |

| 2015 | $5,500 | $1,000 | $5,500 |

| 2014 | $5,500 | $1,000 | $5,500 |

| 2013 | $5,500 | $1,000 | $5,500 |

| 2012 | $5,000 | $1,000 | $5,000 |

| 2011 | $5,000 | $1,000 | $5,000 |

| 2010 | $5,000 | $1,000 | $5,000 |

| 2009 | $5,000 | $1,000 | $5,000 |

| 2008 | $5,000 | $1,000 | $5,000 |

| 2007 | $4,000 | $1,000 | $4,000 |

| 2006 | $4,000 | $1,000 | $4,000 |

| 2005 | $4,000 | $500 | $4,000 |

| 2004 | $3,000 | $500 | $3,000 |

| 2003 | $3,000 | $500 | $3,000 |

| 2002 | $3,000 | $500 | $3,000 |

| 2001 | $2,000 | — | $2,000 |

| 2000 | $2,000 | — | $2,000 |

| 1999 | $2,000 | — | $2,000 |

| 1998 | $2,000 | — | $2,000 |

| 1997 | $2,000 | — | $2,000 |

| 1996 | $2,000 | — | $250 |

| 1995 | $2,000 | — | $250 |

| 1994 | $2,000 | — | $250 |

| 1993 | $2,000 | — | $250 |

| 1992 | $2,000 | — | $250 |

| 1991 | $2,000 | — | $250 |

| 1990 | $2,000 | — | $250 |

| 1989 | $2,000 | — | $250 |

| 1988 | $2,000 | — | $250 |

| 1987 | $2,000 | — | $250 |

| 1986 | $2,000 | — | $250 |

| 1985 | $2,000 | — | $250 |

| 1984 | $2,000 | — | $250 |

| 1983 | $2,000 | — | $250 |

| 1982 | $2,000 | — | $250 |

| 1981 | $1,500 | — | $250 |

| 1980 | $1,500 | — | $250 |

| 1979 | $1,500 | — | $250 |

| 1978 | $1,500 | — | $250 |

| 1977 | $1,500 | — | $250 |

| 1976 | $1,500 | — | — |

| 1975 | $1,500 | — | — |

| 1974 | $1,500 | — | — |

The IRA or Individual Retirement Account, just like its cousin the 401(k), was an invention of the 1970s.

First introduced in the Employee Retirement Income Security Act of 1974 (better known as ERISA), the IRA is a portable retirement account which allows contributions from workers outside of the worker's employer. The IRA family also claims employer run IRAs; one example is the Simplified Employee Pension IRA (SEP IRA), created in 1978.

Popularity of the IRA as a Retirement Account

The IRA gained popularity in 1981 with the Economic Recovery Tax Act encouraging workers to contribute more to the IRA. It established a $2,000 limit (up from $1500) on contributions regardless of a worker's access to a retirement plan through work.

Congress reversed course in 1986, limiting contributions for earners at jobs with retirement plans.

Key Dates in the History of the IRA in the United States

- 1974

Individual IRA accounts are created in the Employee Retirement Income Security Act. The initial limit was $1,500. - 1981

Congress passes the Economic Recovery Tax Act, raising the contribution limit to $2,000 and not tying the limit to money earned at a job with a retirement plan available. - 1986

Congress eliminated the universal deduction in the Tax Reform Act. IRA contributions are limited by earned income and any retirement accounts an earner has available through work. - 1997

The Taxpayer Relief Act introduced the Roth version of the IRA, allowing its holder to pay taxes in the present for the freedom of not paying tax when withdrawing from the account. Like the now-known-as 'traditional' IRA, no taxes are charged on any growth in the account. Additionally, for that tax year the Spousal IRA limit was increased from a then-$250 to $2,000. - 2002

2001's Economic Growth and Tax Relief Reconciliation Act increased contribution limits for 2002, and introduced 'Catch Up' contributions for 50 year old and older workers. EGTRRA also changed the contribution limits by statute, and indexed future increases in the contribution limit to inflation. - 2005

The Bankruptcy Abuse Prevention and Consumer Protection Act clarified that defined contribution plans such as the Individual Retirement Account were protected in the event of a bankruptcy, up to $1,000,000 (with no need to check if that level of income would be required). The amount periodically increases with the cost of living. - 2005

The Tax Increase Prevention and Reconciliation Act of 2005 eliminated any income limits on rollovers from Traditional Roth IRAs to Roth IRAs. Visit the Roth IRA Conversion Calculator to model whether it is worth making a conversion. - 2026

The SECURE 2.0 Act of 2022 increased the catch-up contribution for IRA holders ages 50+ from $1,000 to $1,100, with annual cost-of-living adjustments going forward.

Historical Sources on the IRA Limit

For more reading on the IRA, here's a great start:

- The always excellent Investment Company Institute on the history of the IRA through 2003

- National Institute of Pension Administrators presentation on the bankruptcy status of retirement accounts

- IRA Rules on the IRS website

- Tax Policy Center Maximum Benefits Table

We also have a post on the historical contribution limit on the 401(k).