On this page is a Roth IRA Conversion Calculator. Enter your current and future tax rate and return assumptions – we'll do the math to help you decide whether to convert a Traditional IRA to a Roth IRA.

Roth IRA Conversion Calculator

To use the tool, you'll need to enter some information about your traditional IRA accounts, your age, and your current taxes. You'll also need to guess at your future tax rates for the tool to model your optimal choice.

Inputs to the Conversion Tool

Here are the inputs to edit:

- Current Age: Enter your age today, or the age you will be when you convert the IRA.

- Withdrawal Age: Enter your age when you'll start to withdraw from the IRA. (60 is the minimum in the tool, enter 60 if you will withdraw at 59.5).

- Current Marginal Tax (%): Input your marginal tax rate in percent, adding how much you are taxed on each additional dollar of earnings (Federal, plus optionally State and Local taxes).

- Marginal Tax Rate at Retirement (%): Guess your retirement marginal tax rate in percent, again adding up how much you will be taxed on each additional dollar of earnings (Federal/State/Local taxes).

- Retirement Investment Tax (%): Estimate your capital gains tax rate at retirement. (This is used to estimate the taxes owed on your tax savings opportunity cost fund.)

- Return on Investment (%): How much will your investments return per year? Be as conservative or as bullish as you wish, or try a few scenarios. Try our S&P 500 historical return calculator to derive some reasonable guesses.

- Total Amount to Convert ($): Enter your overall balance in Traditional IRAs to convert.

- Non-deductible Amount ($): Enter the amount of the total balance that is non-deductible. Generally, you can make non-deductible contributions when you make too much to qualify for an IRA in a given year and file form 8606. See the IRS's guidance for IRAs for more.

Running the Conversion Tool

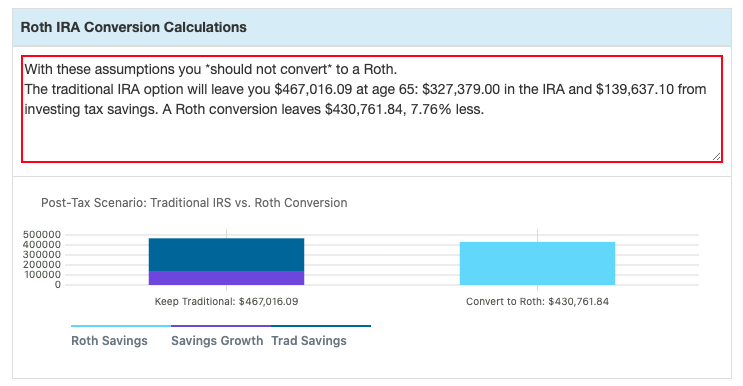

Once you're happy with your true numbers and your assumptions, hit the Should You Convert? button. Using those estimates, we'll quickly run an after-tax scenario comparing two courses of action:

- Convert your Traditional IRA to a Roth IRA: Modeling any taxes you'll owe on the conversion, we'll use your ROI assumption to model tax-free money at your withdrawal age.

- Leave your Traditional IRA and Invest any Tax Balance: Assume any taxes you would pay on a conversion (read: only money for which you took a deduction) are invested at your ROI assumption. Add the marginal amount to your IRA balance at your withdrawal age.

Inside the result box, you'll see the results of your scenario run. Additionally, just below DQYDJ will add a visual representation to your choice – hover (or tap on mobile) to see the breakdown in each scenario.

Questions on Traditional and Roth IRA Conversions

Before I let you go, let’s address a couple of questions around traditional IRA to Roth IRA conversions.

How do I minimize taxes when converting a traditional IRA to Roth IRA?

There are two ways to minimize taxes when converting: convert in a year you earn less in income, or make non-deductible contributions and pay taxes up front.

If you earn less money in a conversion year, you will have a lower current marginal tax rate making the Roth IRA more attractive. With non-deductible contributions (using IRS form 8606), you pay tax up front and add money to an IRA – this money will not be taxed again when you convert (this is called a Backdoor Roth IRA).

Why should you model converting a traditional IRA to a Roth IRA?

Using assumptions you provide, this tool will help you decide whether to convert a Traditional IRA to a Roth IRA.

With a Roth IRA, you pay all of your taxes today in exchange for the government never taxing you again on the funds. With a traditional IRA, you pay no taxes today in exchange for taxes when you withdraw the funds in retirement.

The IRS allows you to convert a traditional IRA to a Roth IRA. You can never be sure if it’s a good deal to convert an IRA, but this conversion tool will help you make an educated guess. Based upon your estimated future tax rates (and structure), investment returns, and time in the market, it’s possible to guess the optimal decision.

Of course – the optimal monetary decision. Life is messy; this tool can’t model every scenario outside the bounds of the assumptions.

Roth IRA Conversion Calculator Disclaimer

Consult your financial and tax advisors before making any decisions.

This tool is for research and informational purposes only and is not tax or investment advice. Additionally, the tool can only project numbers, no tool can project future returns, tax rates, or family situations.