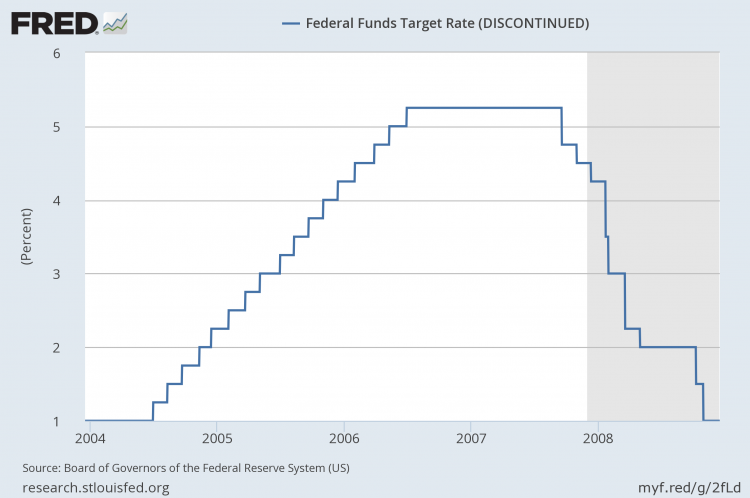

On December 16th, the Federal Reserve raised the Target Federal Funds rate for the first time since June of 2006 - raising it from a range of '0.00% to 0.25%' to a range of '0.25% to 0.50%'. They also telegraphed a very gradual rising of rates in the future - previous hiking cycles have tended to ratchet up one rise at a constant rate every meeting. A good example, of course, being the most recent hiking/cutting cycle, which started in 2006:

... Don't expect a similar looking staircase this cycle.

Future Inflation

With that said, one of the things the Fed concentrated on in this statement is their 2% inflation target. To wit:

"...the Committee will assess realized and expected economic conditions relative to its objectives of maximum employment and 2 percent inflation."

We haven't seen 2% inflation for quite some time, but one of the interesting things we can do using various financial instruments is to predict future inflation rates (in essence, subtract inflation adjusted yields from non inflation adjusted yields in the same timeframe). This is a series we return to often, and we have a calculator which neatly calculates expected inflation over various timeframes. (We also have a backwards looking daily inflation calculator back to 1913, if you aren't into the crystal ball).

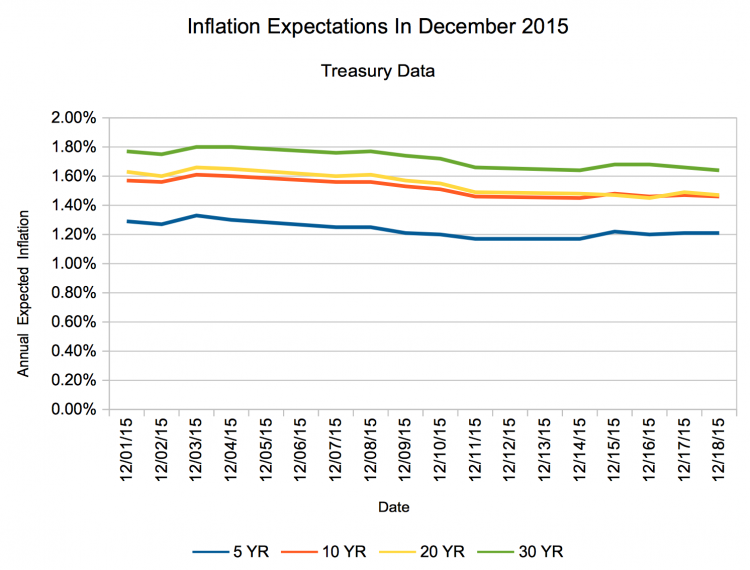

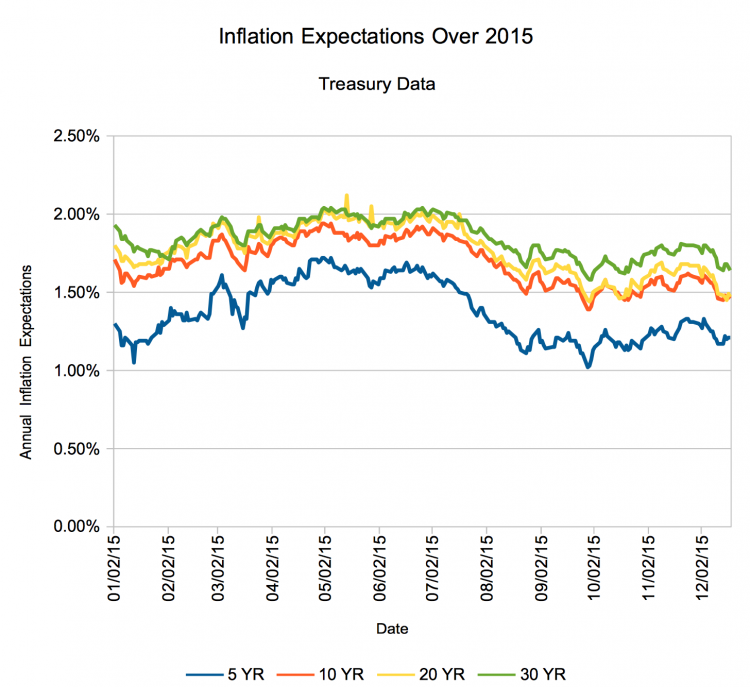

So, does the market expect 2% inflation at any point in the near to not-so-near future? (Data is from the Treasury, all numbers are annual inflation expectations).

... and for the entire year?

Expectations vs. Reality

So, we'll eventually do a post on how these calculated expectations have compared to reality over the years - but as you can imagine, the market is often wrong with these calculated predictions. That is - these are breakeven rates, but there is nothing stopping them from being wrong - even wildly wrong.

Still, it's interesting to see that the market still doesn't see 2% annual inflation over any of the timeframes we're tracking.

What do you think? Will we see 2% inflation over a sustained timeframe ever again?