One category we haven't visited lately is Treasury breakeven rates.

By subtracting the current yield on inflation adjusted securities from the yield on treasuries, you can get an approximation of the market's current inflation expectations. While this methodology isn't exact (taxes, timing, estimates, etc...), it's very easy to calculate and within shouting distance of some of the more expansive methods.

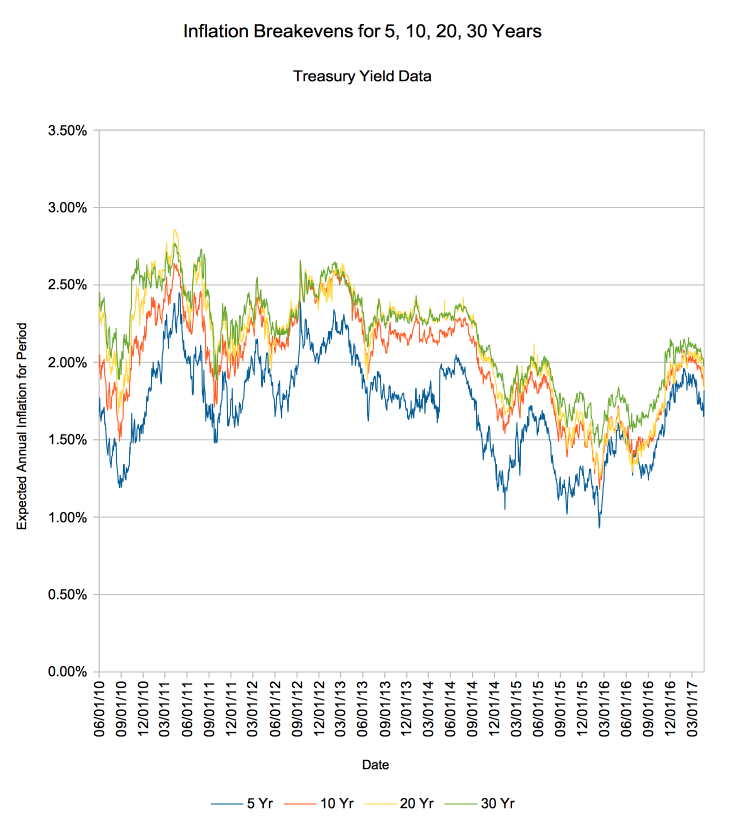

Inflation Expectations as of 4/20/2017

5 Year, 10 Year, 20 Year and 30 Year Inflation Breakevens, 4/20/2017. Read: expected annually.

When President Trump was elected, there was a quick rise of expectations on the longer series. 30 year and 20 year inflation expectations surged back to... well, 2014 levels.

The last couple of months seem to have traced out the top of a curve. On the thirty year, for example, we saw a peak of 2.16% expected annual inflation on February 15th. The market has since dialed it back to 1.97%.

Not much on an absolute level, to be sure - but that's an 8.8% drop over the course of only a couple months.

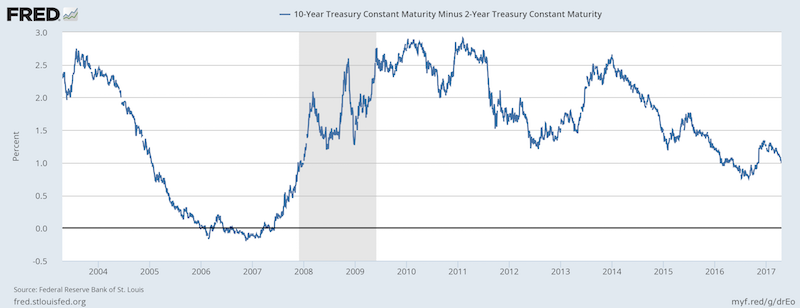

A Flattening Yield Curve

At the same time, the yield curve itself has flattened.

A flattening yield curve is usually (but certainly isn't always) a harbinger of leaner times. In essence, the yield curve is a plot of the cost for an entity (usually a government) to borrow money over various time periods. If it costs more to borrow over a short time period than a long one, the flat (or inverted) yield curve is reflecting some anticipated risk in the near future. (Or actual problem in the present).

One measurement of the 'steepness' of the yield curve is a simple subtraction of the two year constant maturity treasury from the ten year - a measure that currently stands at 1.02%. In November and December, that number was closer to 1.25%, so there has undoubtedly been some flattening:

Ten Year Constant Maturity Treasuries minus 2 Year Constant Maturity Treasuries

Following the Curves

What does it all mean? Your guess is s good as mine, and I'd prefer to just point out the changes rather than make predictions based upon them. There's nothing absurdly alarming, per se. Even over the last 9 years we've had a number of periods with dropping inflation expectations and/or a flattening yield curve but haven't seen a recession yet.

So, over to you - much ado about 8.7%? A real concern? Sound off below, and check out our calculator for treasury breakevens after!