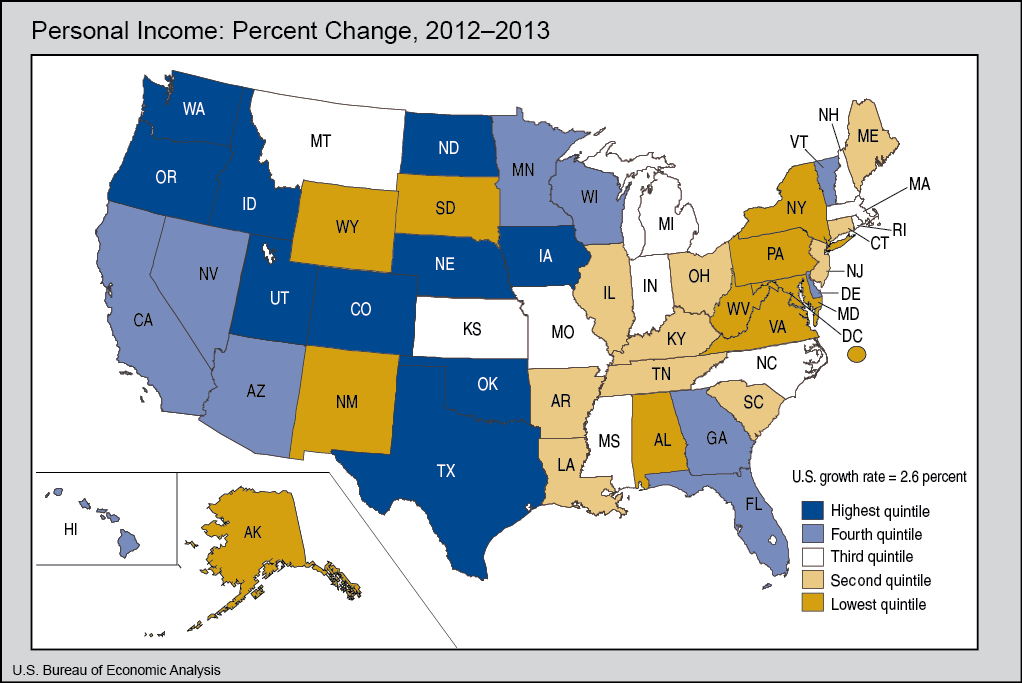

The Bureau of Economic Analysis recently (okay, fine, more than a month ago) released the very interesting state personal income overview for 2013. In it, they break down that oh-so-important indicator, personal income growth, into a percentage change from 2012 in each state (and Washington, DC).

Uneven Growth

The report revealed an interesting income trend when it comes to industry - every single industry tracked grew earnings in 2013, except government (and explains some of the poor growth in DC, Virginia, and Maryland in the map above). That came with a caveat, however: most private industries grew earnings at a slower pace than in 2012.

The states ranged from a high of 7.6%(!) income growth in North Dakota, related to the energy boom all the way down to a mere 1.5% in West Virginia. If you want to roll it up regionally, there was a tie at the top: the Southwest and the Rockies both saw 3.4% wage growth. Compare that to the Mideast, which lagged with 2.0%.

How Did You Do? Your State? ... Your Region?

I lagged California's 2.8% from 2012-2013, at least according to the tax return I just filed - volatility in a bonus will do that (haha). Shockingly (!), for a web site named "Don't Quit Your Day Job...", the web site's earnings don't contribute that much to the bottom line.

That said, in a state where $1.8 trillion dollars was earned in 2013 (across a population of 38.3 million), California's 2.8% is impressive. Overall, California ranked 16th on the income growth scale, and was 12th overall in per capita income in 2013.

So - maybe you don't get as excited about BEA releases as we do - but you've got to admit that this particular release is an interesting one.