Editor: Patrice has followed up on his promise to study his strategy - please see his Accumulation Decumulation Study, and visit his writeup on his website.

Please welcome Patrice Leblanc to Don't Quit Your Day Job... today as your guest host!

He graduated from the University of Sherbrooke with a degree in Mathematics and has been working as an actuary in pension administration ever since, mostly working with DB plans. He succeeded in getting an ASA/AICA from the SOA and is finishing up my study for the second Advance course exam for the FSA. He'd like to share a discussion of some retirement withdrawal strategies and a spreadsheet he built for this occasion (scroll to the end for links) - feel free to leave him your questions and comments!

You can also reach Patrice on his personal email.

So you’ve succeeded in accumulating a great lump of money for retirement... great! Now you face another challenge: guessing how much you can access every year.

(It’s a bigger challenge than it first appears!)

The easy way out would be to simply buy an annuity. You can get quotes on the web for this (try the Sun Life calculator or Dinkytown calculator). Such a purchase will insure that you have a constant pension, but will leave your heirs with nothing. Currently, annuities are more expensive due to high life expediencies and low interest rates.

A high number of retirees make the calculation and go for a self-managed fund as part of their pension plan... but how much can you withdraw annually? The infamous Trinity study implies that a 4% withdrawal rate should be okay, but many argue that you need to consider your portfolio, its expected rate of return, volatility and your Management Expense Related Fees (MERs) before coming up with a number. Too high a withdrawal rate and you'll outlive your money... too low and you'll be the richest one in the graveyard!

Establishing a Withdrawal Rate in a Self-Managed Plan

To establish your safe rate, you need to be concerned with two main risks: the volatility of your fund and your longevity risk.

For this article, I will only talk about the first one: fund volatility.

A quick way to never be left with nothing is to use a fixed withdrawal rate (x% of the fund, annually). However, the volatility of such a pension is high.

The classic way to reduce volatility is to go for a balanced Bond/Equity portfolio. However, I would argue that other ways exist to manage the volatility: techniques such as reserve, capping, smoothing and reduction of MER are cost neutral ways to reduce the volatility of your pension. The retiree should not be concerned with the fund's value, but rather with the volatility and viability of his pension.

Dealing with Reserves

“Winter is coming. Prepare yourself.”

-Eddard Stark, Lord of Winterfell Game of Thrones

One of the best techniques at your disposal is your reserve.

Let’s say that you have 1 million dollars at retirement age, and plan to withdraw $40,000 (4%).

Instead, you take $200,000 and put it in 'reserve'. You then withdraw 5% of $800,000 instead, that is $800,000 * 5% = $40,000. If the fund earns more than 5%, the reserve builds for future year. If it earns less, you use the reserve to reduce the impact of the loss on your pension. The great thing about this is that it doesn’t cost a penny and is rather easy to implement.

Let’s experiment with the impact.

Say that in 1996 you had a million dollar fund invested in the highly volatile S&P 500 with a 0.5% MER and started retirement with a 4% withdrawal rate.

| Year | 100% Equity w/o Strategy | Reserve | ||

| Pension | Fund | Pension | Fund | |

| 1996 – Retirement date | $ 40,000 | $ 1,000,000 | $ 40,000 | $ 1,000,000 |

| 2000 bef. dot-com bubble | $ 83,000 | $ 2,075,900 | $ 79,600 | $ 2,081,500 |

| 2009 aft. 2008 crash | $ 39,200 | $ 979,800 | $ 72,500 | $ 881,000 |

| 2015 – today | $ 79,500 | $ 1,986,500 | $ 70,200 | $ 1,523,700 |

It is quite amazing how this single technique can decrease pension changes due to financial crashes and volatility. (For more information on the specific parameter or calculation for this reserve consult the appendix and the provided spreadsheet.)

Capping Indexation

“Don’t be greedy.”

Another great strategy to reduce the interest risk is to cap your potential withdrawals. In other words, if you withdrew $40,000 last year, why not limit this year's withdrawal to $44,000 or less?

This proves essential to mitigate the effects of financial bubbles. On the down side, you delay the gains of excessive returns for later years.

| Year | 100% equity w/o Strategy | Reserve & Capping | ||

| Pension | Fund | Pension | Fund | |

| 1996 – Retirement date | $ 40,000 | $ 1,000,000 | $ 40,000 | $ 1,000,000 |

| 2000 bef. dot-com bubble | $ 83,000 | $ 2,075,900 | $ 60,700 | $ 2,120,100 |

| 2009 aft. 2008 crash | $ 39,200 | $ 979,800 | $ 65,200 | $ 976,700 |

| 2015 – today | $ 79,500 | $ 1,986,500 | $ 69,500 | $ 1,818,300 |

A complementary strategy would be to limit your prospective pension.

If 1 year prior to retirement you had estimated to withdraw $40,000 in a year, why not limit your withdrawal to $44,000 or less?

For instance, how much should a person who retired in 2000 withdraw?

Say that you had $621,000 in 1996. You might then have expected a fund of $1,000,000 in 2000 ($621,000 * (1+10%) ^5). However, as we know due to the bubble, the fund was sitting at $1,500,000 in 2000. A reasonable approach would be to limit the withdrawal in the first few years to see if the excess returns held up... or if it was a just a bubble.

The Smoothing Technique Strategy

“Only time will tell if it holds true.”

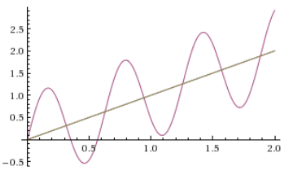

One way to think of your savings accumulation is as an increasing sin function. In that case, you can model your withdrawals based on the midpoint of the function.

When the fund is lower than the midpoint, you would withdraw more as a percentage. When the fund is higher than the midpoint you would withdraw less as a percentage.

However, of course, your fund is not as simple as a sin function.

Let's discuss workarounds. One way to apply smoothing is a linear recognition of N-Year smoothing. First, let's say you estimate the fund's return to be 10%. You could then recognize 20% of the real rate of return instead of the estimate for last year, 40% of the 2 years prior, 60% of the 3 years prior, 80% of the 4 years prior and 100% of the 5 years prior.

Thus the result would be somewhere near the imaginary midpoint line in the above sin function.

The main disadvantage of this method is that smoothing returns will hide or delay the recognition of gains & losses. Thus, this method can serve you as a quick estimate, but you should still consider the real fund returns. This mainly helps manage the small variations.

Reduce Your Management Fees

“Beware of thieves!”

Simply: if you are charged 2%, that's 2% that you are not getting.

I would recommend looking at Canadian Couch Potato articles on this subject. Simply reducing the number of withdrawals in a year or picking lower-fee funds would increase your effective withdrawal rate. At equal returns in the underlying securities, a fund charging an extra 1% might mean settling for $30,000 a year instead of $40,000 over time.

Types of Bonds and Their Effects on a Portfolio

There are two main types of bonds... you can either lend money to a government or to a corporation.

Government bonds generally offer a comparably low rate of return but compensate by being (practically) risk free. In Canada, returns are currently around 1% on these securities.

This means that if you were to pick a 100% Government fund, you would be able to live off interest only if you withdraw a (poverty assured!) 1%. On a million dollar fund, that’s a mere $10,000! (You can really sympathize with the plight of the millionaire investor these days).

Many investors choose to have around 50% of this type of bond in their bond portfolio. My argument is that you should avoid this type of investment for your retirement funds due to the low returns currently presented.

Lending money to a company is better on the return front. Rest assured, however, they offer a lower return than they are expecting to make from their own investments. Therefore, in theory, equity returns should be higher than bond returns. For example, Moody Seasoned AAA Corporate Bond Yields historically were about 4% less than equity returns. Note too that it stands to reason there will be a high correlation with equity returns when comparing the same organization.

Let’s experiment using some bond mixes and a $1,000,000 portfolio:

- 100% AAA corporate bond

- 100% equity in S&P 500

- 50% in each

We'll use a MER of 0.5% and a withdrawal rate of 4% ($40,000 in the very first year). Here’s how your pension withdrawals would have fared in a good period (1950-1969) and in a bad period (1996-2015):

| 100% bond | 50% bond/equity | 100% equity | 100% equity + strategy | 100% bond | 50% bond/equity | 100% equity | 100% equity + strategy | |

| Start at | 1950 | 1950 | 1950 | 1950 | 1996 | 1996 | 1996 | 1996 |

| 5 years | $ 43,200 | $ 51,600 | $64,500 | $ 58,300 | $ 47,600 | $ 62,300 | $ 83,000 | $ 55,100 |

| 10 years | $ 39,800 | $ 74,800 | $ 136,100 | $ 108,600 | $ 49,900 | $ 55,200 | $ 59,700 | $ 63,000 |

| 15 years | $ 38,400 | $ 84,800 | $ 176,600 | $ 160,100 | $ 50,100 | $ 52,200 | $ 48,700 | $ 64,200 |

| 20 years | $ 38,800 | $ 99,300 | $ 235,800 | $ 253,400 | $ 47,700 | $ 65,700 | $ 79,500 | $ 64,300 |

If you had started in 1950 in a 100% bond portfolio, your retirement income would have actually dropped by 1970.

Why settle then for these low returns with little increase in annual withdrawals? (Warren Buffet even suggests his spouse have an aggressive portfolio!)

The experiment has set the fund amounts equal at retirement age, but if you would have kept these portfolios prior to retirement a similar pattern emerges.

For example, at age 30 in 1960 a lump sum of $51,000 in an 100% equity portfolio would have left you with $1,000,000 at age 65 in 1995. In a 100% bond portfolio, it would have taken you double that amount, $106,000, to obtain the same portfolio size. (Thus your pension would have cost you double!)

A life cycle technique helps, but I would argue for a portfolio with a heavy equity allocation, even in retirement.

A common praise for bonds is that they cover the costs of inflation. I would argue that equity does as well. If the whole economy raises prices, it stands to reason that company values will also rise! While the coverage is not as correlated, you should eventually recover from high inflation with equity-heavy portfolios.

So, please note: while 100% bond portfolios reduce fluctuations and volatility, other strategies also exist to reduce fluctuations.

A brief note on higher withdrawal rates and a combination of reserve, capping & smoothing at 6% and with lower cap and reserve protection at 8% withdrawal rate:

At 6% the strategies produce a good result, with a final reserve of 20% and a final fund of $1,000,000, but with significant fluctuations in your annual withdrawal. At 8%, there was a significant drop and you were left with a final fund of around ~$800,000. (Considering that starting in 1996 would have faced two major crises back to back, perhaps that's not so bad?)

Note again that all the results above include a 0.5% MER on bond and equity funds.

Conclusion

As a retiree, it's not the size of the fund that matters... it’s how much you can withdraw safely.

Your focus should not be on the health of your fund at any given time, but on the fluctuation of your pension and its size. Regardless of the amount of your savings the above strategies are completely scalable. Whether you have $1,000,000 or $100,000 (and choose to self-manage!) you too can implement these strategies.

Appendix:

I do not know your specific objectives. Perhaps you would feel better with $120,000 at 69 and $44,000 at 78. Or, perhaps, you find that any drop of larger than 5% doesn't sit right with your personality. Perhaps, even, you believe that mirroring the worst crash since 1929 will be a common thing from now on.

Achieving no drop at all is unrealistic if you're banking on high annual pension withdrawals. In that case, price out annuities – they are the closest instrument to a no-volatility retirement. Otherwise, determine a reasonable drop for your personality and goals (75%? 95%?) and how much you would want to withdraw around age 80 (more or less than at age 65?).

The default parameter in my model represent my own personal preferences. I wouldn't necessarily recommend that you match my preferences. At best, my starting point it will serve as a discussion opener for your own retirement. (In short: feel free to change any of my inputs.)

In changing any parameters or in trying other strategies, I strongly suggest you look at the impact of starting retirement in various years in the past to see the impact (ex: 1929, 1942, 1980, and 2000). Also try a stress test: increase the MER by 1% or more to see what would happen if the economy is consistently worse than we are historically used to seeing.

If you would want to apply these strategies going forward, simply note the return you receive year by year and apply your personal formula to fund value and returns.

Data

For this article, I’ve limited myself to:

- The estimate of S&P 500 by Robert Shiller, compiled by Don't Quit Your Day Job.... It already incorporates dividend returns.

- Moody Seasoned AAA Corporate Bond Yield by Board of Governors of the Federal Reserve System (US), Moody's Seasoned Aaa Corporate Bond Yield© [AAA], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/AAA, September 23, 2016.

- Other sources for my model can be found in the spreadsheet in the fund list.

(If you reside in another country, using a local estimate may prove a worthy exercise. The MER was estimated based on various Canadian index funds, but various funds of course offer lower or higher MERs.)

Reserve

The objective of this strategy is to absorb the shock of a crash. It’s not to absorb small changes or, in my mind, to offer inflation protection as a goal.

Parameters:

- Reserve target: This is the percentage of your total fund you will put aside in retirement. I’ve found that even a low percentage would tremendously help with interest rate fluctuations. With around 20% you can protect enough while still not drawing from a reserve all the time. You should consider also changing your withdrawal rate or else the more you reserve, the lower your pension will be. Ex: new withdrawal rate = target withdrawal rate / % of reserve.

- Equity to bond %: Many suggest that a reserve should be 'safe' from fluctuation. This field will adjust for this effect. However from the historical rate of bond returns, I’m not convinced this'll be the case. I find that you lose too much by being over-exposed to bonds. My default parameter is to not include bonds in the reserve.

- Max reserve: After decades of good economic conditions, the reserve may exceed sanity levels. In those cases, you could transfer some reserves to the main fund.

- Reserve protection: This answers the question: how much should you protect past your pension? 100% protection is not the right approach. You almost certainly won't be able to prevent, say, a 1% loss of your savings in a given year. That potential risk of loss is what allows a much higher rate of return. It's also why Guaranteed Income Funds have low returns... it costs a lot to offer “guaranteed” returns at any given date.

- Protect against inflation: Should you use the reserve to protect against inflation? (The default is not to use it in the reserve.)

- Extra protection & after x%: It makes sense that with better reserve health, the more protection it's useful to have. Instead of going with fixed protection, increase and decrease this parameter depending if you're above or below the the target reserve. I find that protecting 1% extra for any percentage above or lower than the 20% reserve is okay. For example, if the reserve is at 25% of the main fund, then protect +5% of your withdrawal rate.

- Long term reserve: If you have an aggressive strategy, a good way to maintain your reserve would be to slowly reduce reserve coverage. In other words, if you withdraw 20% from the reserve, next year should protect less. It’s easy to see the impact if you change the retirement date to 1929, just before the crash in the Great Depression. Effectively, this parameter will decrease by x% if the previous year's(/years') decline was more than twice your target withdrawal rate.

- Reserve longevity and Reserve stability. It seems sane to limit withdrawals for reserves to last at least 5 years (i.e. a 20% withdrawal rate). In the case where reserves reduce too much for this test, I take the higher of 80% of last year's fund reserve and a 40% withdrawal rate from the reserve. This helps get through 1929-type events with a few pennies in reserve!

Capping

This strategy helps lower your pension expectations. If you become used to an extravagant lifestyle, you may find it more difficult to reduce expenses later. In truth, the strategy delays gains in your fund to better manage pension fluctuations.

- Max increase: Set the maximum increase in withdrawals per year. You can look at, for example, the impact of a change in this parameter if you retired at 1995 or 1950.

- Max increase before retirement: Same as the above, but since you are not getting a pension out of your fund, you should let it rise more rapidly.

- Tying the max increase to indexation is a great way to deal with inflation risks. However, some experts have recently argued that your consumption actually decreases by a few percent during retirement each year. I’ve added a feature to the sheet to remove 2% from inflation to better reflect this potential scenario. During periods of super high inflation, you may want to add a cap on inflation protection.

- In case of sustained great economic conditions, I’ve found that increasing the cap by one percent per year greatly reduces the gap compared to a strategy without a cap. For example, if the previous five years all hit a cap, I would suggest increasing the cap by 5%.

- If you are unreasonably conservative, a minimum withdraw rate of 1% can help you be more realistic in your planning. If that happens in your modeling, you should review your parameters.

Smoothing - Linear recognition N-Year smoothing technique

This strategy is more complex.... but at the end of the day a formula can help you manage it.

The calculation

For linear recognition with 5-year periods and an expected gain of 10%

- First, you take the current fund balance. Then, subtract the 4/5 of the gain/loss (G/L) of last year, but add 4/5 of the expected gain of 10%. You repeat for previous years. Subtract 3/5 of the G/L of 2 years ago, add 3/5 of the expected gain, subtract 2/5 of G/L and add 2/5 of the expected gain of 3 years ago, subtract 1/5 of G/L and add 1/5 of the expected gain of 4 years ago. This method will fully recognize the fund as of 5 years ago and somewhat average out the latest return.

- Ex :

- Input :

- Fund as of 2001 = $1,000,000

- Fund as of 2002 = $876,502, return of -12.35%

- Fund as of 2003 = $679,587, return of -22.47%

- Fund as of 2004 = $868,891, return of 27.86%

- Current Fund as of 2005 = $957,889, return of 10.24%

- Calculation

- Smoothed Fund = $1,049,934 = $975,889 - 4/5 * $868,891* ((1+10.24%) – (1+10%)) - 3/5 * $679,587 * (27.86% - 10%) - 2/5 * $876,502 * (-22.47% - 10%) - 1/5 * $1,000,000 * (-12.35% - 10%)

- Input :

Parameter input

- You can modify the number of years you want to smooth (in 'N-years', the N). It should be tied with the economic cycle length you foresee, historically around 5 years. That is, we expect to have a recession every 5 years or so. Higher lengths will further increase the gap between the reality of the fund and the smoothed estimate. A smaller number could be used, but the impact of the smoothing would be lower.

- Also set the expected rate of return of your fund. I’ve estimated the historic average to be around 11%, but it’s a moving average. For some decades it was higher and in others it was lower. Even in longer lengths of time, the average varies a lot depending on which recessions you’ve included in the span. Investopedia claims the S&P 500 has an historic average gain of around 10%. In the end, the impact of the estimates is not overly important compared to the number of years of smoothing.

- You can add in a corridor. So that way instead of the smoothing estimates you would assume the estimate to be at a maximum of 105% of real fund or 95% of real fund. The Society of Actuaries says that you should use an unbiased corridor for a pension fund estimate.

- I’ve added to my model another potential strategy: if the smoothed average is too high above the real fund's return, I believe that the withdrawal rate should be lowered... or at least not increase compared to the previous year. Since my purpose is to limit the drop in withdrawal rate, I’ve limited these drops to 95% of last year fund. That way I limit the impact of the current fund, but do not exceedingly rely on it during the length of smoothing.