In this article, we continue our annual tradition of sharing our savings rate. We consider a savings rate to be one of the most important numbers you can optimize when it comes to your personal finances - all the strategies you put into play are easier with a higher rate, and you have more room for error. Every dollar you don't spend is not only coming off the expenses side - it's also sticking around to help you grow your net worth at a faster pace!

Along those lines, we've also noted that with a calculation of net worth and a savings rate alone (and a reasonable return estimate) you can guess how long it'll be before you're financially independent. We've also created a calculator for you to try to match our savings rate calculation.

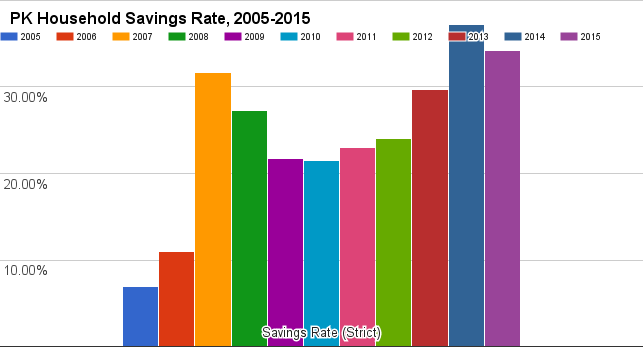

Our Household's Savings Rate This Year and the Recent Past

Our net savings rate in 2015 was 34.23%. That is slightly down from our net rate of 37.26% in 2014.

(Note that net savings do not count paydown of principal or increase in the value of our investments. We've discussed this methodology before here.)

For comparison to your own rate, we're married 30-something homeowners in the Bay Area with a daughter and another baby on the way... and a very loyal dog!

We've been tracking our net savings rate closely the last 11 years.

In table form, for whatever purposes you deem useful:

| Year | 2005 | 2006 | 2007 | 2008 | 2009 | 2010 |

| Savings Rate (Strict) | 6.91% | 11.02% | 31.63% | 27.31% | 21.68% | 21.47% |

| Year | 2011 | 2012 | 2013 | 2014 | 2015 | |

| Savings Rate (Strict) | 22.96% | 23.99% | 29.68% | 37.26% | 34.23% |

Our Reaction to Our Savings Rate

We're pessimistic on our rate this year - we expect it to dip a bit due to the expenses of our second, but hopefully we'll keep it over 30%.

I do think 30% is a solid savings rate target. That's especially true for net savings rates which are way stricter than gross savings rates quoted elsewhere (and yes, I know that a dollar paid down on a loan is still a dollar towards net worth). We've charted out the effect of savings rates on your years to financial independence before, and estimated that even 10% savings rates should keep you on track for retirement in a 40-year career assuming normal investment conditions (who knows?).

(However, if you're 22 and trying to retire by 30? Aim for 68-72%!)

In Closing...

Ostensibly, this is a personal finance site. That means that topics that Cameron and I cover are tangentially related to one of our interests, whether that means we disagree with the practice, are neutral on it, or embrace it. We're only going to write on things that hold our interest long enough to write 500+ words.

That's why the few inward looking articles we do a year are important. It signals to you whether we're following our own advice and "practicing what we preach". On a personal level, it also keeps my wife and I on target. I'd expect you to discard everything written here if we suddenly became chronic overspenders!

So, stay tuned for some of our other 'personal' personal finance articles - normally we like to share our investment breakdown versus benchmarks along with our active/passive breakdown. As usual, there's no ETA on those pieces - expect the normal levels of randomness from DQYDJ in the meantime!

How was your savings rate in 2015? Do you prefer gross or net savings rates? Since it's probably gross, how much do you hate that we still quote net rates?