Don't look now (ahem, actually, look now!) - talk about a coming rate hike by the Federal Reserve and changing risk assessments worldwide has spiked the yield on low rated corporate debt. Or, you know, other reasons.

Measured by the Bank of America Merrill Lynch CCC and below and AAA rated corporate debt yield indices, the last week has seen an amazing widening of the spread between 'junk' or 'unsafe' (charitably) corporate debt, and safe AAA graded debt: a 13.86% spread as of 12/02, up from as low as 12.32% last week on the 23rd.

(This year we've seen spreads as low as 7.42% on March 2nd.)

The Rapidly Rising Risk Premium on Corporate Debt

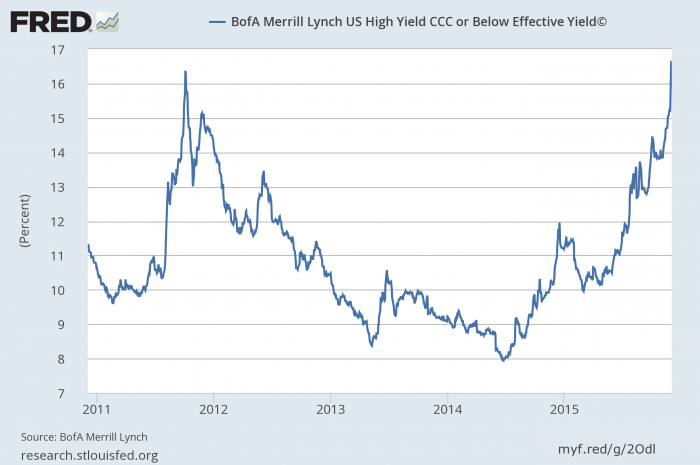

Yield on CCC debt through December 2015, BofA Merrill Lynch

That's a pretty dramatic chart in isolation, but more interesting for our purposes is a graph showing the spread between low rated debt (CCC and below) and nominally safer debt, rated AAA. This measure shows the so-called "flight to quality", as investors shun riskier assets for the higher quality that AAA corporates offer.

CCC - AAA Yield Spread, BofA Merrill Lynch

What Does It Mean?

I'm not even going to try to wrap a narrative around it, but it's a sign of... something. We're now at the highest spread since the Great Recession... although we spent plenty of time with less risk tolerance back early last decade.

So you tell me... what does it mean? Is it just folks finally taking the Fed seriously? A turning point in the cycle? A worldwide flight to safer assets? Something else entirely? Nothing much?

You fill in the blanks, and if you feel like it even post a comment. (We'll be here all week!)