"Inflation is always and everywhere a monetary phenomenon." - Milton Friedman

Smart guy, that Milton Friedman. I heard he won a Nobel Prize.

There's no Nobel Prize on my desk (yet), but I'm willing to strike down some of the current arguments about the coming hyperinflation, the current "under-reported" inflation, and even targeted hidden inflation (a.k.a the Middle Class Squeeze).

Every Side Has Inflation Hawks...

Let's break down the three arguments. Unfortunately, I can only give these superficial treatment - if you think I'm misrepresenting one of them let me know. However, keep in mind you probably wouldn't read this if it was 5,000 words...

- The Coming Hyperinflation! - Adherents of this theory are concerned with the rapid expansion of the monetary base, which we can easily graph at the St. Louis Fed's excellent data repository. Here is a graph of M2, also known as a measure of money, or, specifically, currency in circulation in checking accounts and in accounts easily converted to money.

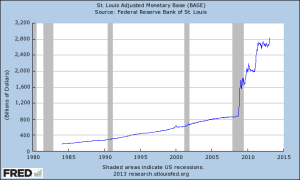

Scary, isn't it? Didn't Friedman say that money would cause inflation? We'll get back to that. Another chart you'll often see is the monetary base, which is the money supply before all the M2 magic happens. Take a look:

Scary, isn't it? Didn't Friedman say that money would cause inflation? We'll get back to that. Another chart you'll often see is the monetary base, which is the money supply before all the M2 magic happens. Take a look:

Keep that last chart in mind for this coming discussion. - We're Hiding High Inflation! - This argument centers on quite a few aspects - first and foremost that the Fed strips out volatile energy and food prices from the inflation indicator they watch. Another aspect takes issue with the hedonic regression used to determine the CPI and even the concept of substitution in the CPI (bread expensive? Let them eat cake!). Even though I sympathize with some of this argument in light of the huge price increases of some commodities, the price of gold is not inflation. I'll go into this further one day - but, to summarize, the price of things we use goes down and we find new necessities... that's what's clouding the picture. You didn't pay for satellite TV, Netflix, and Pandora in 1950.I know, I know - you can't eat an iPad. Very funny - but someone has to determine what an average household buys, and, at least in the DQYDJ household, it isn't 100% food and energy.

- Middle Class Needs Are Inflating! - This is an argument I first saw championed by Paul Krugman (another Nobel winner). Observe: the middle class (or at least middle income brackets, which is as good a definition as any) spent much the same proportion of their earnings on food, shelter, clothing and transportation in the 80s as today.Well, admittedly, it's quite possible 70s food was better than today. However, aside from a few Chinese Drywall incidents (and some other shoddy bubble-peak building examples), your typical 2011 residence was better than your typical 1984 home.

Want some examples of changes to necessities since the 80s?

Here in the Bay Area, building codes were revised in the 80s - turns out ground floor garages without sufficient support don't mix with earthquakes. Clothing was pretty good in the mid 1980s, but there has been a ton of innovation in specialized equipment - compare 1984 running shoes to the modern variety, for example. And transportation? Well, that one isn't even close. (That's a very scary video.)

Other than maybe food, if you want 1984 quality goods you can get them a lot cheaper than the 2011 variety. Enough that I would wager you could spend a lot less of your household budget.

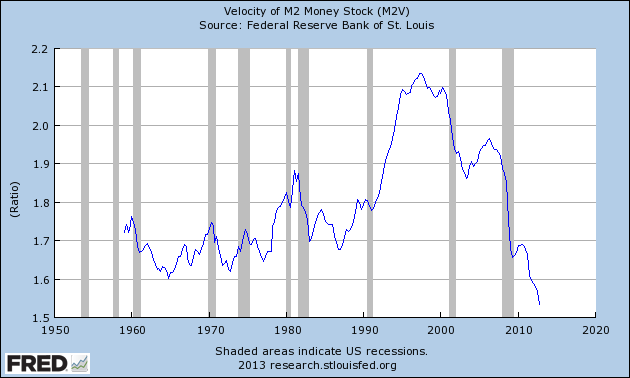

The First Great Inflation Sponge - The Velocity of Money

A brief primer on monetary velocity that only a parable can provide is provided in full hilarity by this letter to the editor in Parade. In it, $100 to an innkeeper pays off an entire town's debts, and the $100 is later refunded to the customer.

Sure, it was meant as, perhaps, a knock on stimulus. However, it was actually illustrating monetary velocity - literally, how fast money in the money supply is spent. If new money is created but is instantly buried in a hole, that's different than the scenario described in the story above. Stories from the tail end of the Weimar Republic's hyperinflation describe insane monetary velocities - why hold onto money if its value is cutting in half or a third daily?

If velocity decreases? Even in the face of new currency, inflation should be tame, or deflation might even be present. Take a look at monetary velocity over the last few years:

Now, is the relationship causal? You'll have to hop into the Keynesian debate on the Quantity Theory of Inflation, but... maybe. The fact remains - even if the money supply is increased, a drop in velocity can mean stable prices. That's some of what we're seeing today.

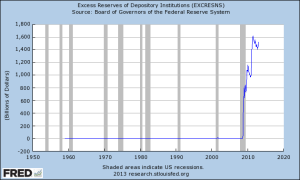

The Second Great Inflation Sponge - Interest on Excess Reserves

Okay, this is a pretty epic graph, so let's lead with it before explaining what happened:

Banks in the United States (there are similar systems in place around the world) are mandated to hold a certain amount of deposits with the Federal Reserve - these are known as reserve requirements. Now, obviously, holding aside a certain amount of the assets under your management is a major opportunity cost - those reserves never used to pay anything. That's why you see a flat-line on excess reserves back to the late 1950s - why would a bank hold aside more money if that money could earn more money elsewhere?

Banks in the United States (there are similar systems in place around the world) are mandated to hold a certain amount of deposits with the Federal Reserve - these are known as reserve requirements. Now, obviously, holding aside a certain amount of the assets under your management is a major opportunity cost - those reserves never used to pay anything. That's why you see a flat-line on excess reserves back to the late 1950s - why would a bank hold aside more money if that money could earn more money elsewhere?

That was all true, until a little known policy went into effect at the Fed - interest on excess reserves held with the Fed. That policy change happened in October of 2008. And the rocket ship in the graph above? That was banks storing more money at the Fed - at last reading (January, 2013) it stood at a whopping $1.52 trillion.

So, thinking back to the graphs in the "Hyperinflation" section, you can see why that isn't that serious of a problem - the banks are calculating they can make more money in interest from the Fed (currently .25%) than lending that money out. In short, the money that would be sloshing around in a normal economy is parked at the Fed. Perhaps in normal circumstances that monetary expansion would be inflationary - but right now it's like burying new money in the yard.

What Does the Future Hold for Inflation?

A lot of what happens in the near-term depends on how well the Fed can soak up excess liquidity if they end up stopping the policy of paying interest on reserves, or the economy otherwise starts to heat up. Chairman Ben Bernanke has hinted in past speeches that the Fed has considered dropping the interest paid on reserves. Economist Alan Blinder has made the case explicitly that lowering the rates paid on the excess reserves will get banks to lend out some of that $1.52 trillion. (To wit: he advocates eventually going negative and charging banks interest to hold money with the Fed).

The nightmare scenario? A sudden increase in velocity and decrease in reserves held at the Fed, resulting in massive inflation before policies can get a grip on the problem. Now, note that markets aren't exactly predicting massive inflation, at least as measured by the CPI. That doesn't mean that inflation won't happen, or run-up of some commodities - just that the shrill voices you hear are not the market consensus.

So, your call - how do you think we'll work our way out of this? Will we avoid the mistakes of the Weimar Republic? Are you buying gold and oil? Stocks or bonds? Let's hear what you're thinking!