We're going to make the case that even though it can feel hard at times and you're probably nowhere near your peak earning years... you should make every effort to build savings in your 20s.

When you're in your 20s, your greatest asset is your youth itself. Not only does being young mean your (possibly mediocre savings amount) has more time to compound and increase in value, but you've also got to face a sobering fact: one day you won't have your youth anymore.

Why Should You Have Savings in Your 20s?

Credit where credit is due: Lauren Martin writing on Elite Daily dropped a viral hot-take-bomb which made the claim that any savings in your 20s was 'wrong':

This goes back to a piece of advice a very successful friend gave me: “Don’t save money. Make more money,” he nonchalantly stated, pushing me into a taxi.

Unlike most things people tell me, this advice did not go in one ear and out the other; it stayed with me and changed the way I look at everything from my career to my savings.

Here's the problem, Lauren: your friend gave you horrible advice.

Looking for someone to validate an idea you already had percolating in your head is one thing, but screwing up a lifetime of finances because of an offhand remark of a dude shuffling into a taxi is yet another. The truth is, spending all of your resources in your 20s will leave a hole in your bank account come 30 (40? 50?) years old - and your relatives and support system are more likely to forgive a 20-something for silly decisions than a 40-something - by then, the elder generation will have his own retirement to worry about.

What Do You Mean 'A Hole in Your Finances'?

"When you care about your 401k, your life is just “k”" - Lauren Martin in Elite Daily

It's easy to point out: the biggest advantage of the youth is, well, their youth.

The very fact that their relatively small contributions to savings and retirement accounts will be 'in the market', so to speak, for a long time... that's why they are at an advantage. Those programs are set up with that idea in mind - yes, retirement accounts often allow catchup contributions for folks over a certain age, but contribution caps themselves are an explicit message: "use it or lose it". If you don't contribute anything to your 401(k) at 29, no one is going to allow you to contribute more than your cap at 41.

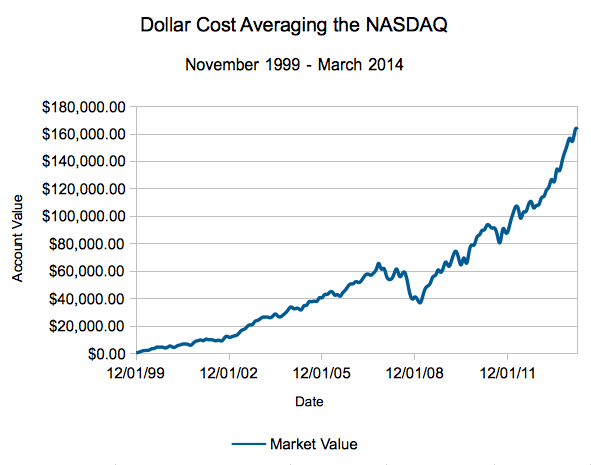

Additionally, not touching money for a long time has the curious effect of compounding that money.... to the point that the highest performer of all investor types is someone who forgets they have an account. We've done many case studies here on the site, but the best illustration of why time and consistency matters is one we posted last March: if you graduated school during the tech bubble and invested $500 a month in the NASDAQ, oblivious to that whole tech bubble thing... would you have ever made your money back?

Yes... in fact, you would have gotten around 8.5% annual returns through March of 2014:

$500 a Month into the NASDAQ, Starting Right Before the Bubble

This is purposefully picking one of the worst times to start a career: right before the massive technology bubble bursting. And, yet, 15 years later (so a 22 year old would be ~37), in retrospect the returns would look pretty good! All that from a $500 a month investment ($6,000 a year).

What About the Fact You Make More Money When You Are Older?

This is true - age is also a proxy for experience, both with the technical or day to day aspects of your job, but also with the politics of the workforce. On the other hand, Martin's quote about making more money way oversells the case:

Your 20s are not the time to save; they’re the time to gamble. $200 a month isn’t going to make the dent that a $60,000 pay raise will after spending all those nights out networking.

Luckily for you, we've done the math recently on what sort of raises you can expect over your career. For young workers (male here, female here), that argument never really applies. If it does, it is generally for the top 10% of workers (go look at the charts in those posts), and only if measured from the early 20s - before 25.

If you're going to make $60,000 more than yourself the day before your 30th birthday, you are in the top 10% of all workers.

The takeaway message isn't that you shouldn't strive to make more money - it's that you need to be realistic. Perhaps productivity and wages increase much higher for the Milennials than for the Boomers and Xers, but historically a $60,000 increase in real income once you are already in your career isn't something to count on.

Yes, that includes Boomers who network at bars and clubs.

Enjoy Your 20s! But Also Think of Your 40s!

In your 20s and reading this site? Your parents are probably in their 50s and 60s, possibly just recovering from assisting you with your college education and possibly also now assisting your siblings. Instead of taking your advice on savings while you're 20-something from a man falling into a cab and retold secondhand by another 20-something, how about you ask your parents if they wished they had saved more money back when they were in their 20s?

Even if they say "ehh, we made up for it", note that it's easier to save less when you have other responsibilities to your family, than it is to save more once those responsibilities come to the foreground. It's easier to build up savings in your 20s and turn it off in troubled times, then to hit troubled times and suddenly also increase your savings rate! (Again, to a rate higher than it needed to be 20 years earlier since you now have less time for compounding!)

I'm not being an internet curmudgeon - you need to have fun, too, in your 20s (and beyond, actually). Just don't sacrifice the rest of your life to do it.

While a 20 year old can treat their 40, 50, 60 year old and beyond self with respect and set themselves up for success by having a savings base... the reverse will never work, unless you also invent a time machine.

So do yourself a solid - set up a savings plan while you're young, make it a habit - then spend whatever is left over on crazy adventures. It's worth it to build up a base of savings in your 20s. If you want an idea how much to save, check out our own comparison tool for savings rates by age and for net worth by age to see how your peers stack up.