In honor of tax season, we at DQYDJ annually post savings rate and asset allocation summaries.

Unfortunately, I find mine particularly boring. I am young enough and have enough time left in the market that it has pretty much become throw it all in stocks and wait. Because of that (and that I've been at it for a little while now), my monthly fluctuations are usually much higher than my monthly savings so it's tough to keep perfect track as my allocation changes.

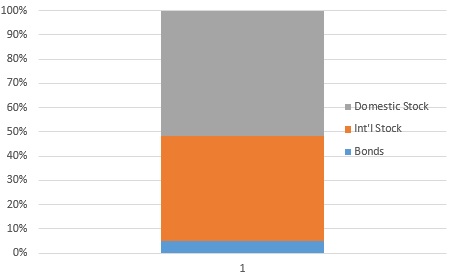

95% Stocks, 5% Bonds

My asset allocation is 50% domestic stock, 45% international stock, 5% bonds and around 0% cash (my checking account getting too high gives me anxiety). I plan on keeping a similar asset allocation for another 8-10 years before shifting to very slightly more bonds.

Around 50% Domestic, 45% International and 5% bonds

As you can guess from the S&P 500 return, the portfolio has been performing very well over the past few years. From the beginning of February 2018 until now is the largest loss I will recognize due to the volatility in the market and the timing of when a lot of my purchases have been.

I wanted to break it down by passive vs. active investing but it is 100% passive besides the stock purchase plan I have. I hold it generally until it vests and save a little bit extra to time some long-term capital gains.

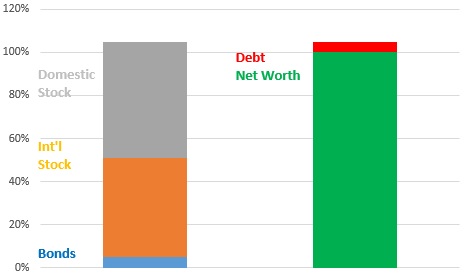

But, enough about the investment strategy, let's start looking at this as a percentage of my net worth.

I Like Cheap Debt

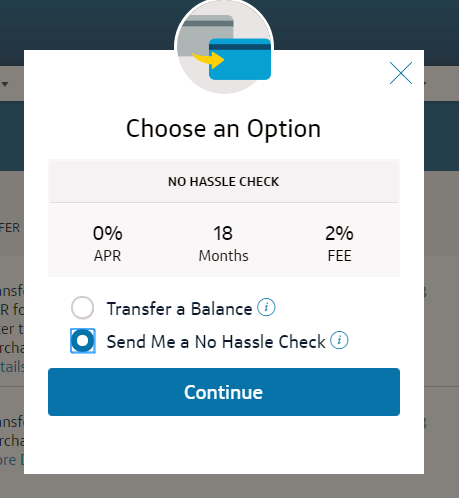

It's hard to find ways to leverage debt besides real estate and mortgages. One of the habits I have begun the past few years is to always maintain a cash balance on a balance transfer credit card.

I usually have carry about two balance transfer offers for credit cards at any time. Usually the deal is 0% APR for 18 months and a 3% fee (about a 2% interest rate) or 15 month 0% APR for 0% fee, etc. Small time-frames and small amounts of debt sure, but I like the idea of being able to maintain a low cash amount with very cheap debt while maintain a very high % of my net worth (not just assets) in stocks.

Unfairly inexpensive debt option

The most recent offer I accepted was for a check at 2% fee (for 0% APR over 18 months). I assume there's a good amount of risk involved in carrying the debt (maybe August 2019 will be a particularly cash-constrained time) and the underlying assets I will purchase. The past few times have paid out well though, and I consider it a way to slightly amplify the returns of my portfolio, increase risk and get some leverage without using real estate.

Leverage only slightly increases my portfolio size

Unfortunately, it is a small amount of debt compared to the amount you can leverage with real estate. Some online brokers offer the ability to lever up relatively cheaply, but I haven't made that step yet to add even more leverage to my portfolio. (Consider that a sure sign that we're about to skyrocket)

The plan for the upcoming year is probably getting into real estate again, shoveling money at stocks and trying to find ways to get cheap debt.

Cheers,

Cameron Daniels