The 401(k) is one of the best accounts to save a significant amount for retirement in the United States. 401(k) contribution limits are generous, and allow you to shield a healthy amount of income from taxes. However, the majority of people don't contribute the maximum to their 401(k) – which leads us to ask: what if you always maxed out your 401(k)?

What if you always maxed out your 401(k)?

If you only invested in the S&P 500, started working in January 1999, and always maxed your 401(k) you'd have around $825,000 today.

(For other start dates, see the chart below.)

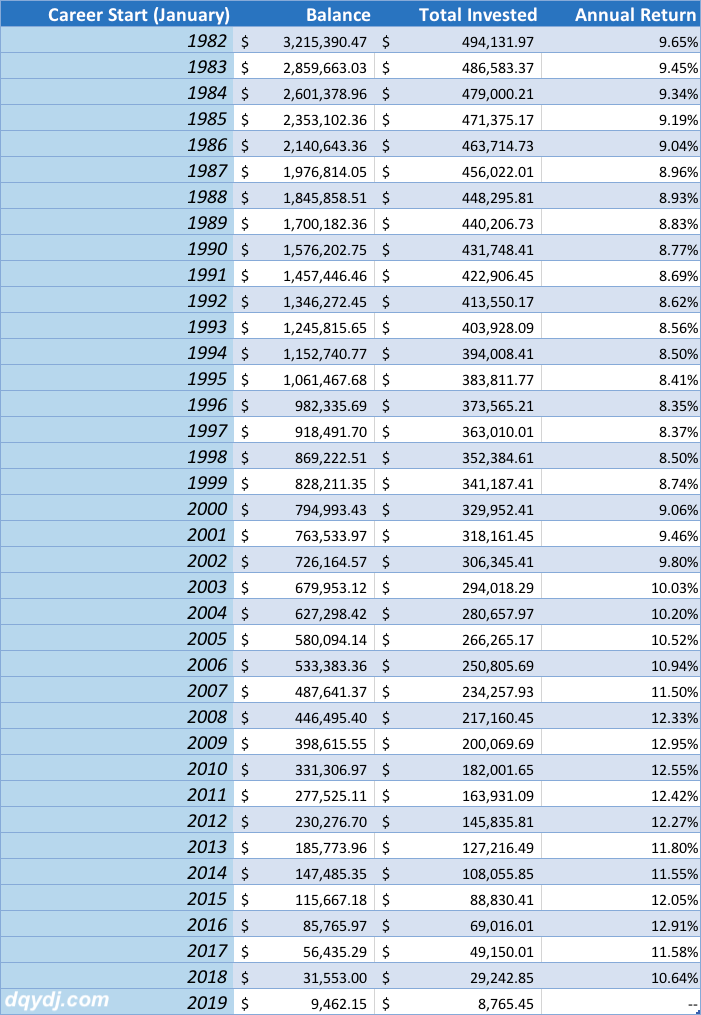

Maximizing a 401(k) for every career start year

If you had started maxing out your 401(k) back in 1995 or earlier in an S&P 500 fund, we estimate you'd be a 401(k) millionaire!

A roughly 60 year old worker who started contributing the max in 1982 would have a massive $3.2 million account. Even a roughly 35 year old worker who started maxing out a 401(k) in 2007 would have about $485,000.

Here's the graph showing career start dates and maxed out 401(k) balances for every career start year back to 1982:

As you can see, no matter what year you started your account, after a few years it was a tremendously great deal.

You not only built a tax-free reservoir of wealth, but also shielded all of those contributions and gains from state and federal taxes!

401(k) Maximum Assumptions

It's impossible to do a post like this without some hand-waving. We invented an S&P 500 index fund using our S&P 500 Periodic Return Calculator as the only investment option.

Here's everything we assumed for this post:

- We tracked both the current account balance in a 401(k), as well as the annual return implied by the current balance and your total contributions (XIRR)

- We assumed you only invested in a S&P 500 index fund with a typical fee

- Numbers track 401(k) balances based on starting in January of each year since 1982

- The simulation assumes equal contributions each month

- We added a 3% employer match

- Our data ends on 05/03/2019

Of course, making this "exact" isn't possible. Perhaps you only had expensive funds available, a greater or smaller match, or some other difference. Still – we're happy with the simulation.

Who maxes out their 401(k)?

Hopefully, you do.

Unfortunately, the odds are against that - so I'm glad you're reading! The vast majority of account holders do not max out their 401(k)s.

In 2018, Vanguard released a report quantifying just how rare it was for an account holder to maximize a 401(k): only 13% of people maxed their 401(k)s in 2017.

That's a low number, but is actually an improvement from the 10% seen in 2012!

We've shared the history of 401(k) contribution limits. Even if you didn't max while younger, one benefit available to older workers is the 'catch-up' contribution. This allows account holder who are 50 years old or older to contribute an additional amount to their accounts - a full $6,000 in 2019.

Unfortunately, the participation rates for catch-up contributions are also low: 14% of those eligible used them in 2017. In 2015 that number peaked at 15%.

It's not all bad news, though: in 2017, participants (including any employer match) averaged a contribution of 10.3%, which is healthier than the United States average savings rate!

What are average 401(k) account balances?

Thanks to a Fidelity analysis of Q3 2018 balances we know in 2018:

- The average 401(k) balance was $106,500

- The average IRA balance was $111,000

Unfortunately, looking only at 401(k) balances doesn't tell the whole story, which is why we included IRA balances.

One of the awesome features of 401(k)s is portability. When you leave a job, you are able to roll over your 401(k) into an IRA.

This means that any study of 401(k)s will have a reverse survival bias - you'll only see balances for people still with their current company, or who have chosen to not roll over their 401(k) into an IRA.

Take the two together as roughly $215,000. We estimate that, in theory, any maxed 401(k) account started before 2012 and invested only in the S&P 500 would already be higher.

Also, see how you would have fared if you always maxed an IRA.

What else can you learn from maxed out 401(k)s?

From our study, we learned some interesting things about maxed out 401(k)s:

- Ignoring recent account start dates, if you always maxed out your 401(k) starting in 2009 you have best results out of any year. You'd have seen a huge 12.95% annual return!

- Maxed out 401(k)s that started in 1996 performed the "worst"... but still boast an awesome 8.35% annual return.

- The median annual return if you always maxed out your 401(k) and started between 1982 and 2018 was 9.46%

- The (simple) average annual return if you consistently maxed your 401(k) and started between 1982 and 2018 was 10.09%

- If you always maxed out your 401(k), your leverage becomes massive after enough time. Accounts started in 1982 have $3.2 million balances on only $500,000 in personal contributions!

One of the features you can see in our chart is that we estimated annual return percentages (sort of like weighted compound annual growth rates) if you always maxed out your 401(k).

This used a function called 'XIRR', which we built into our S&P 500 Periodic Investment tool. XIRR allows you to find out the actual return on money based on periodic investments, as opposed to 'simple' returns based on a lump sum up front. XIRR is a weighted average, so each month's contributions matter in the final result.

401(k) Maximum Contribution Methodology

- The math is for a maxed out 401(k) contribution divided evenly for 12 months

- We used our S&P 500 Periodic Investment Calculator to do the math

- The fee estimates are inside the calculator; feel free to redo the math for your own assumptions!

- The current chart ends in May of 2017

- We started in 1982 because that's when the 401(k) became popular (technically, it began 4 years earlier)

- 1982-1986 technically had a $30,000 employee contribution limit - but we used a $7,000 limit for fairness.

How did you compute employer 401(k) matches?

- We based all of the numbers on a 3% employer match (It's estimated around 2.7%)

- We estimated you earned 2 times the personal median income

- See all income percentiles by age on our calculator

Always max out your 401(k)!

Some time back, we made a strong argument to always max out your 401(k). This study should solidify it: if you always maxed out your 401(k) you'd have a very healthy account balance. That's even if you always just stayed in stocks. Additionally, we showed you a 401(k) calculator to project your growth over time.

That includes all of the ups and downs - and sideways - moves inherent to investing in stocks. They've handsomely paid off for you if you're maxing out annually. (You can see what sort of historical returns the S&P 500 has with our convenient calculator, and historical returns in this other tool.)

Nothing speaks louder than results. If you always maxed out your 401(k) you're doing very well!

I hope this was enlightening and useful - we'll consider it a success if you move your 401(k) contributions just a little bit closer to 'max' after you read this. Let us know what you decide!

Have you always maxed out your 401(k)? Even if you didn't, how does your balance compare to the chart? Is maxing out your 401(k) a good strategy?