The Individual Retirement Account or IRA is an excellent tax free account available to most American workers. Unlike 401(k)s, IRAs are completely portable and usually have fewer restrictions on the number of investments they allow. They unfortunately come with smaller contribution limits than 401(k)s. Still, most people don't take full advantage of the accounts... so we have to ask: what if you always maxed out your IRA?

What if you always maxed out your IRA?

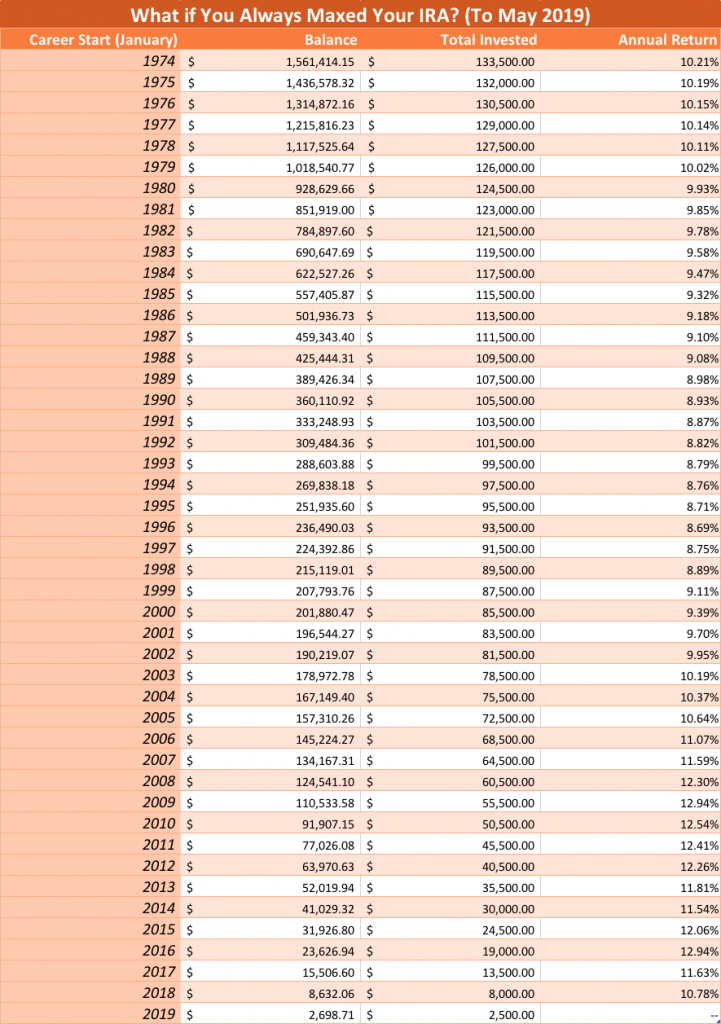

If you started an IRA in 1989 and always contributed up to the limit while investing in the S&P 500, you'd have around $390,000 today. All that's on a total of around $110,000 invested.

You can find the number for other account start dates in the chart below.

Maximizing a IRA in every year since 1974

If you had started maxing out your IRA in 1979 or earlier, we estimate you're currently an IRA millionaire!

A roughly 60 year old who started maxing out an IRA in an S&P 500 Index Fund in 1982 had around $785,000 in their account. A roughly 35 year old who started in 2007 now claims around $135,000.

For every account start year going back to 1974, we ran the numbers. This chart shows the value of an account started in January of the listed year:

Note that some of these years span longer than a 'typical' career. 1974-2019 is 45 years, so presumably a person is either retired or started the IRA pre-career.

You can find the complete history of IRA contribution limits on our site.

What did you find out about maxing your IRA?

We found that for starting every period in the last 45 years, you've never seen average annual growth under 8.69%.

For accounts open longest, you're probably also seeing a million or more dollars in account balance! And that includes a wild amount of leverage - accounts started in 1974 sit around $1.56 million on only $133,500 in contributions.

It was good news all down the chart, too. If you always maxed out your IRA, invested in the S&P 500, and have had the account since 2009, we estimate your account is at least 6 figures.

Since IRAs aren't bound to a formal job, that means folks who are maybe 28-34 (and always maxed their IRAs) could have over $100,000 based on IRA contributions alone!

Whether you chose a Roth-style IRA or a Traditional IRA, you are getting a great deal. Along with that tax benefit, your account itself also grows without the drag of taxes.

What other IRA assumptions did you make?

- We used the S&P 500 Reinvestment and Periodic Investment Calculator for computations and estimates

- We assumed you only invested in a S&P 500 index fund with a typical low fee

- Numbers track IRA balances based on starting in January of each year since 1974

- The simulation assumes equal contributions each month

- Our data ends on 05/03/2019

What else did you learn from the maxed out IRA study?

Just like our 401(k) maxing out study, we learned a lot of interesting things in this study.

- The (simple) average annual return if you always maxed out your IRA starting in Januaries between 1974 and 2018 was 10.21%

- The median annual return while maxing out your IRA between 1974 and 2018 was 9.95%

- Investors starting in 1996 so far have fared the worst, returning "only" 8.69% a year

- IRAs started in January 2009 and always maxed out returned an estimated 12.94% annually so far!

In every time period, starting an IRA and always maxing it out was an excellent financial move!

Always Maxing Out Your IRA is the Best Option

On this site, we've argued forcefully to always maximize your retirement funds. This study only furthers the case for cranking your savings up to the max.

Even in the worst case, an always maxed out IRA still would have returned over 8.5% a year... a very good result. Also, a very good result which you could have attained by merely buying and holding an index fund.

(And that strategy is often best for the common investor.)

While we wouldn't suggest staying 100% in stocks (especially a mere 500 stocks from a single country), passive portfolios work best for the vast majority of people. With that in mind, you shouldn't try to beat the above numbers... consider them an investing ideal and a theoretical (and just a guess).

Have you always maxed out your IRA? Even if you haven't, how does your balance compare to the above chart?