One good habit to get yourself into is an, at a minimum, annual financial health check. For me, I often do a deep dive into our finances during tax season. "Thanks" to this annual tax ritual, it's easy to evaluate our financial situation at the same time as I've got all of my documentation in order (read: in chaos) around me. That labor also produced this 2016 savings rate article.

For this article, I've rolled up my investment allocation. In this post I'll share some broad strokes on my positioning coming out of tax season. Maybe that helps you, or maybe it doesn't - but perhaps this template will help you take stock of your own portfolio. (Pun always intended)

This includes only the liquid portion of our portfolio, broadly defined as the parts that can be moved without too much hassle.

Investment Categories and Classes

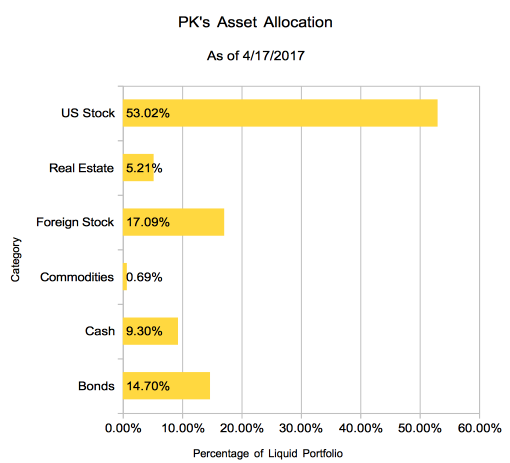

PK's Portfolio Allocation

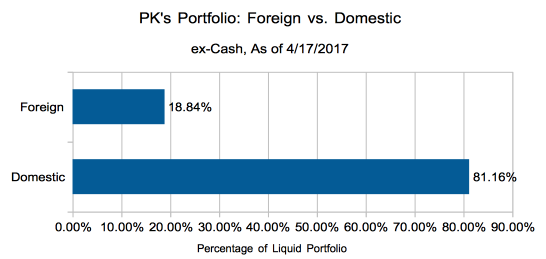

At a category level, it looks like I've got some knobs to turn. New contributions combined with some big successes (and a general rising tide for domestic equities) have left my portfolio with a majority of domestic stock. I expect to shift that allocation more towards overseas stocks this year.

Foreign vs. Domestic Breakdown

Broad Asset Classes

Zooming out ever further, here's what the portfolio looks like:

| Class | Percentage |

| Equities | 70.10% |

| Bonds & Cash | 24.00% |

| Real Estate | 5.21% |

| Commodities | 0.69% |

For the under-35 crowd, our 24% cash and bonds might be on the high side of desired. However, I think we're most comfortable with somewhere between an 80/20 split and a 60/40 split. Call it a wash.

Commodities at this point are just a rounding error in our portfolio. I'm not particularly keen on commodities as investments, but I might bump that a couple percentage points. I suppose it's possible we are caught short by massive commodity price run-ups or something, but I don't think it's too likely a scenario. If you do feel particularly strong one way or the other I'd love to hear your thoughts.

As for real estate, we have no interest in becoming commercial or industrial landlords, so that's why this shows up here. Outside of the obvious decline of retail, its not doing too terribly as a class - I feel comfortable with the current allocation.

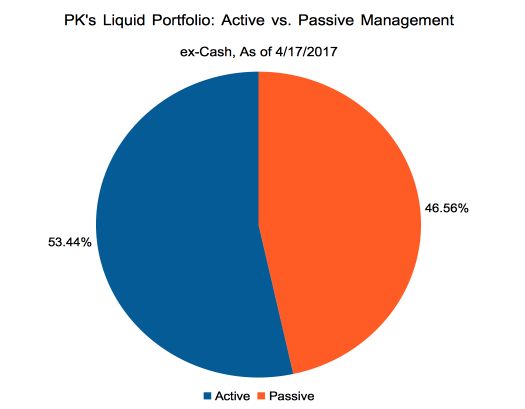

Management Style

As for the active vs. passive breakdown, active is now slightly dominant. I've backed cash out of the portfolio for this graph (I suppose that's technically passive-ish?), but here's an ugly pie chart showing the breakdown:

PK: Active vs. Passive Breakdown (Get that Pie Chart Out of Here!)

As you longer term readers know, we recommend that a generic person's portfolio is mostly - if not wholly - passive. (See our personal finance basics article).

We don't entirely follow our own advice. I do manage some individual stocks, and some funds we hold are actively managed. If you've been through a few business cycles (and have studied the field) judge for yourself, but I agree: this is too much active management. I will move the needle back into passive management.

Investment Allocations for 2017

When I did the math on my current allocation some things stuck out:

- Our domestic - foreign balance is too far towards domestic

- Our active - passive balance is too far (way too far) towards active

That's the sort of thing I'd only learn if I made the effort to roll up the metadata. That's why we suggest doing the same sort of exercise on your own situation - you might find that your exposure to various things is too high or too low.

Have you done a financial checkup recently? Find anything interesting? Do you disagree with any of my moves (or curious non-moves)?