I get many questions about the top one percent in net worth and income. And, as you might expect, net worth and income blend quite a bit... so I also get questions about the correlation of net worth and income in the United States. Usually, people wonder how well income predicts net worth.

Income does not predict wealth all that well. There certainly is a relationship, though it's relatively weak. In 2022-23 in America, the correlation between income and net worth was .5593, an R^2 of .3128.

Read on for the correlation of income and net worth by age – and arguments for why this isn't a great measure.

The Correlation of Income and Net Worth is Weak in America

An R^2 of .3128 is a weak coefficient of determination, though it is stronger than we saw in past editions of this post. That number means nearly 69% of the variability between income and net worth comes from somewhere else.

There is more at play in net worth than a household's income at the point they take a survey. However, as you can see below in the income and net worth correlation visualization, income definitely matters.

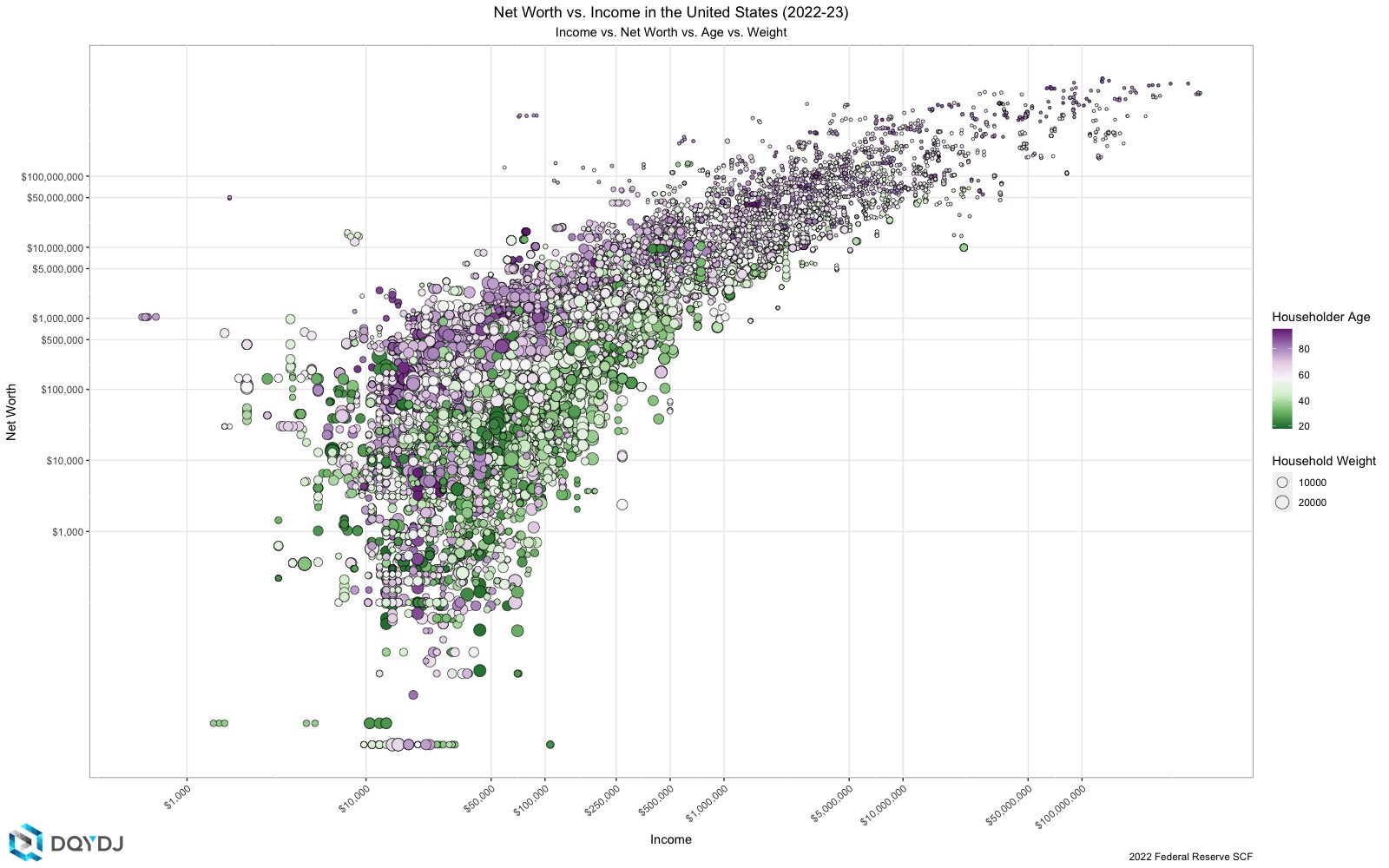

Visualizing the Relationship Between Net Worth and Income

Above, we've graphed individual responses in the 2022 Federal Reserve SCF with income on the X-axis and net worth on the Y-axis with a logarithmic scale. The color varies between green and purple, and represents the age of the reference householder. The size of the circle represents the weight of the response in the correlation calculation – NORC and the Federal Reserve weight the responses to better represent American demographics.

Note that our choice of the log scale means we are tossing out households with a net worth (or income) less than or equal to $0. Also, read our net worth research for full methodology details.

Logarithmic Income and Net Worth

I'll continue to play ball with the correlation question. As you see from our axes in the bubble plot, if we took the Pearson correlation coefficient of the log10 income and log10 net worth, it will likely be better than the naive linear correlation.

Now, there's a significant issue here – you lose data since income or net worth of $0 (or negative) needs to be discarded. Let's accept that's okay, and push onward.

Using positive numbers and log base 10 numbers:

- Correlation: 0.6347

- R^2: 0.4028

Better – but still, that's not a very strong relationship.

What Variables Matter for Net Worth?

I don't believe correlations – adjusted for log base 10 or not – make much sense for this data, as we'd ideally like an input like income history.

(Also, I don't want to be the target of this joke:)

Performing this exercise every few years is useful to show that a single year snapshot of income isn't enough to explain net worth. That's despite how the media conflates income and net worth.

Here are other things that matter:

- Age – More time in the market almost always beats timing the market

- Consistency – Earn a large income over time

- Frugality – Save a high percentage of your income, annually

- Luck – Sometimes it's better to be lucky than good*

* Yes, luck is controversial. But especially for high variance situation – think a startup seeking funds or similar – luck matters. Luck's definition may be the combination of preparation and opportunity, but you can't discount the effect of the coin flip or the dice roll completely.

Additionally, and a new one to note this year (remember, the last survey was in 2020, so this survey period covers many cryptocurrency and meme stock gains), the types of income matter. Capital gains income is tracked by the survey, so selling would show up. However, untaxed capital gains would not show up.

Age and Income vs. Net Worth Correlation

You can see in the above visualization that age has a pretty significant effect on the survey results. Even without a full income history variable, it's evident that older folks at the same rough current income level tend to have more net worth.

Although 'events' such as home sales, stock sales, business windfalls, and the like can cause huge year-to-year swings, earned – or wage – wage income is relatively inelastic. Despite my note above, we'll push forward here and try to split this up by age. What should we expect to see?

A lovely story might be:

- lower correlation for the youngest groups; high net worth here is probably windfall related (e.g., an inheritance or other inter-generational transfer)

- higher correlation in middle age

- falling correlation in older groups as consistency and propensity to save start to dominate income (also: retirees have less income)

but we don't see that.

| Age | Correlation | R^2 |

| 18-24 | .7792 | .6072 |

| 25-29 | .6281 | .3945 |

| 30-34 | .5999 | .3599 |

| 35-39 | .2118 | .0449 |

| 40-44 | .8519 | .7258 |

| 45-49 | .6821 | .4653 |

| 50-54 | .7429 | .5519 |

| 55-59 | .6629 | .4394 |

| 60-64 | .6234 | .3887 |

| 65+ | .5989 | .3587 |

Just like last time – yes, I can't quite invent a narrative here. Things completely break down for 35-39 year old householders, yet you see some significant R^2s elsewhere.

Maybe you've got something?

Net Worth vs. Income: How do they differ?

We've done this analysis in the past on 2019, 2016, and 2013 data, and the correlation is there – it but remains weak. This year is the strongest correlation we've seen in the SCF, but it isn't easy to make up a narrative for it.

I'll now mention an excellent way to look at income and net worth that I've discussed in the past:

- Look at income as acceleration - how quickly a household adds to its total wealth... assuming the household can save and invest.

- Net worth, on the other hand, is speed or how fast the car is currently moving. Net worth has inertia.

It's not perfect. It is, however, a decent way to frame this issue. Acceleration matters in gaining speed, but it doesn't necessarily mean you'll reach a high speed (You could crash! You could slow down! You might accelerate again!).

Lump Sums and Income Streams

Another way to look at income vs. net worth?

It's relatively easy to convert net worth to a stream of income. However, converting an income stream to net worth is not so straightforward. (More discussion in the average net worth post).

Instead of just one year's income, variables like age matter a lot – play with the net worth by age calculator to get a feel.

You should expect a 25-year-old and a 65-year-old, both making $100,000 a year, to have wildly different household wealth. And – although we don't know the future – the 25-year-old can have a substantial net worth at age 65 if they sustain those earnings and are good at saving.

Furthermore, there is a large group of people with little to no income and substantial wealth: retirees.

(No, not "personal finance bloggers"!)

Methodology and Source on the Correlation Of Income and Net Worth

We start with the 2022 SCF Data from the Federal Reserve.