If there's one thing to be said about Finance sites (especially the blogs), it's that there is no shortage of voyeuristic information posted for the view of anyone who happens to wander by. Think about it - straight Personal Finance blogs sometimes detail every transaction the author makes, Investment sites demand disclosure about what stocks a person owns, Advisor sites come complete with a detailed biography, and debt blogs? Well, those blogs take disclosure to a new level...

DQYDJ on the other hand, metes out the personal details slowly - because, well, you are not Cameron, Bryan or me. Decisions we make are generally good for our situations, and we do our best to explain how you should approach similar decisions. However, this is a site built on trust. So, once again, we open our books to our faithful readers so you can see if we're (well, at least if PK is...) trustworthy enough to deserve your subscription.

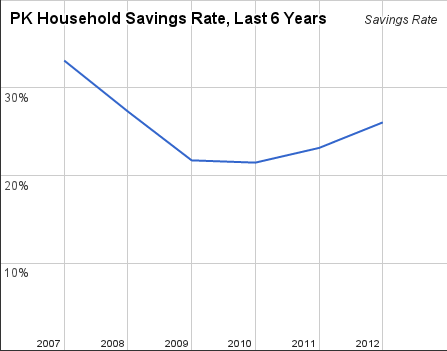

Your Favorite Author's Savings Rate

I use a very strict definition of savings for my calculations, spelled out back when Cameron and I did a point-counterpoint series last year. In essence, I only count liquid savings vehicles - savings accounts, retirement accounts, and the like versus net income. If I counted principal pay-down it would obviously be quite a bit higher. And, of course, if I also counted home improvement spending (I'm sure you could make the case), it would be much higher (heh, especially this year). But we'll run with what we've got - here's the PK household's (strict) savings rate since 2007:

So that's 26.07% net in 2012, using my definition of savings.

How did you do in 2012?