One series we've been tracking for quite some time now (but not since June) is the market's implied inflation expectations in the United States. Essentially, when you subtract the yield on inflation adjusted instruments from the Treasury (which will track the CPI) from the yields on non protected securities, you're polling the market on what it expects inflation to be, annualized, over the term of the securities.

These numbers, so-called "inflation breakevens", are a great gauge of the market's inflation expectations which you can take on any day you've got Treasury data.

(Of course, its not always that simple - there are some factors which introduce noise into the math such as tax treatments, so there are superior models as well).

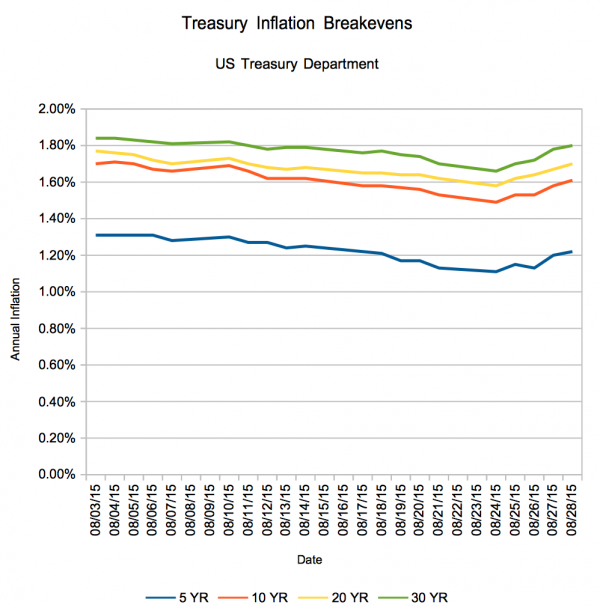

Inflation Expectations in August

Anyway, you're probably interested in seeing how expectations have changed in August due to the increases in volatility in the market. Here you go!

Quite interesting to see breakeven volatility with your own eyes, isn't it? Last week was volatile for more than just stocks.

Anyway, odds are good that a lot of the noise is also shifting expectations of the outcome of the Federal Reserve's September meeting - which, if you haven't been watching closely, might include a rate hike for the first time in the careers of many Millennials now working on Wall Street. (Interesting piece, there, if you haven't seen it.)

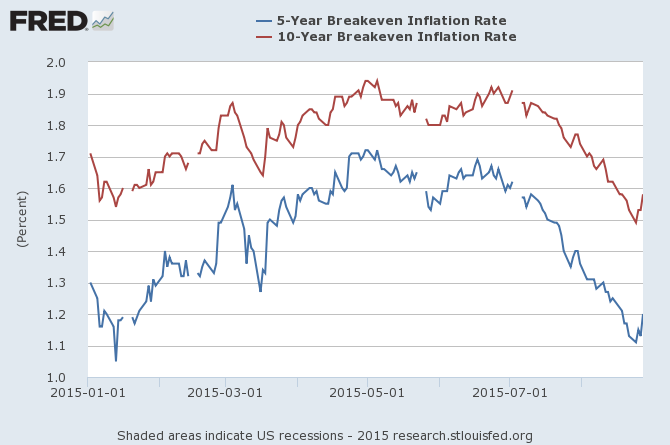

Longer Term Expectations?

But breakevens have moved quite a bit this year, even outside of the volatility which has recently gripped the market. Here's what the five and ten year look like in 2015:

Yes, you're looking at almost a complete retracement from lows in January - buying treasuries just a few months apart made a tangible difference.

As for what happens next? Your guess is as good as mine, so leave your guess in the comments!