Here's a funky question for you: "is Social Security a good investment?". I know it's not possible to opt out (short of leaving the United States), and there still isn't a private option for your funds, but it's still interesting to ponder.

It may be hard to recall now, but in 2004 a President won his election while promising to reform Social Security to allow private accounts. George Bush ultimately failed at that goal, but with Social Security again in the limelight during the whole "Fiscal Cliff" overreaction, we wanted to toss some facts out there to see if the universe is still listening.

Social Security Was Never Meant to Replace Your Entire Income...

Now, we at DQYDJ may swim against the tide quite a bit. Still, we recognize that the odds that one piece of the fiscal cliff bargain is some sort of private Social Security account option are approximating 0%. We also recognize that the low-ish payouts on Social Security are somewhat by design - they were always meant to be supplemental to savings in some other form. Regardless, increasing OASDI levies have squeezed out other forms of defined benefit retirement plans, and moved many companies to defined contribution plans. These facts alone have contributed to a growing wealth gap versus people making more than the Social Security limit. Additionally, there is an undeniable push by some parties to have Social Security pay out even more benefits.

Let's pretend private accounts are actually on the table. I wanted to go back and do the math for some typical workers - would they have been better off under the current system of Social Security, or better off if they had invested their FICA taxes directly in the S&P 500. And how do you perform that wizardry? Simple - I created that tool myself, and you can locate my S&P Dividend Reinvestment Calculator here on DQYDJ. Open it in a new tab and go play with it later.

Okay, you know how to reproduce my data (if you don't I provide a worksheet later in ods format). Let's dig in!

An 'Average' Worker.

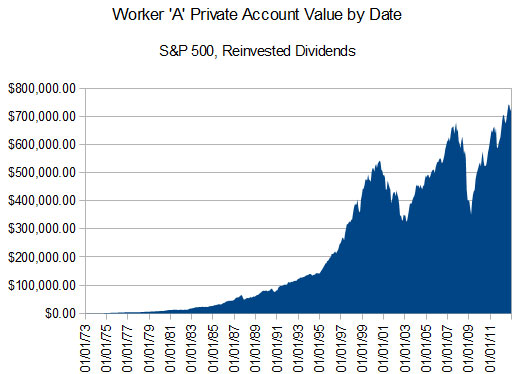

How do you define an average worker? Seems like a tricky question to answer - so I didn't even attempt it. All of the math on this page is based on two 'typical' workers who have earnings histories laid out on a page on the ssa.gov site. On top of that, I retrieved the history of OASDI tax rates from the Tax Policy Center.

Worker 'A' made roughly $40,000 - $45,000 in 2012 dollars annually, while worker B was really unlucky and earned exactly the Social Security taxation limit for every year he was in the workforce (from $10,800 in 1973 to $110,100 in 2012). Worker A accepts benefits at age 62, and worker B at age 65 (see the site for details). Monthly, A will receive $1,605.98. B will receive $2,404.73. And workers A and B in our Bizarro-World of private accounts, invested in the S&P 500 over their careers? Worker A finishes with $730,710.02, while worker B finishes with $1,589,151.22.

Is Social Security a Good Investment? Well, are Equities?

Converting a Lump Sum to a Cash Flow

A oft-quoted rule of thumb of a 'safe withdrawal rate' is 4% - a number which likely isn't completely safe. So, let's try a few methods to figure out what sort of cash flow you could attain:

Worker A - $730,710.02 / 25 / 12 = $2,435.70 (Worker A is 51.7% better off with the Private Account)

Worker B - $1,589,151.22 / 25 / 12 = $5,297.17 (Worker B is 120.28% better off with the Private Account)

But wait, I'm cheating - and it's in favor of Social Security. You see, when a beneficiary and spouse die, that money is no more. Depending on account setup, a private account may have money remaining to pass down between generations. However, let's try to compare apples to apples here, and assume that money is invested directly into an annuity which is inflation adjusted (sort of like the COLA from Social Security) and will continue to be paid at 50% if the main beneficiary dies if his or her spouse is still living.

I'm going to use the annuity calculator on the Thrift Savings Plan website to do this instead of a private sector calculator (with spouse set to the same age as A or B).

Worker A - $730,710.02 = $2,102.00 (Worker A is 30.9% better off with the Private Account)

Worker B - $1,589,151.22 = $5,407.00 (Worker B is 124.85% better off with the Private Account)

Is Social Security a Good Investment? No Contest - It Can't Compare.

Note that the annuity interest rates quoted are incredibly low - 1.75% versus highs of near 5% in 2008... so you're looking at the bottom of the barrel in annuity quotes. Read that again - the worst annuity rates we've ever seen are still better than the return you get from Social Security if you are retiring this year. If you are retiring in 10, 20 years? Odds are you won't even come close. The only time Social Security will beat the private sector (maybe...) is with an early career disability or death of a breadwinner without disability insurance. Outside of that? Not going to happen. In effect, Social Security is squeezing the investment opportunities of people with less income - regressivity in disguise.

The truth is, a private account invested in the S&P 500 would have destroyed anything the Government has to offer - and this is for workers who started working in 1973 during some of the worst economic conditions in history, and are finishing in some similar situations. You truly are comparing the worst of the private world versus the highest benefits Social Security will have (and probably the lowest OASDI tax rates we'll see). Also, I'm not estimating second order effects, but odds are a massive influx of money into the stock market would have some effect on the price of the S&P 500 Index (I'm being facetious, but I didn't want to add any assumptions).

So, if you're against private accounts, please explain your reasoning. From here on my spreadsheet (download it below), they look like a no-brainer. Perhaps a psychology argument might be convincing?

But until then, if you ask "Is Social Security a good investment?" and I'll answer... nope.