On this page is a Restricted Stock Unit Projection calculator or RSU calculator. Enter details of your most recent RSU grant, your company's vesting schedule, and some assumptions about your tax rate and your employer's future returns. From there, the RSU projection tool will model the total economic value of your grant over the years.

Restricted Stock Unit Modeling Calculator

Using the RSU Projection Calculator

To use the RSU projection calculator, walk through the following steps.

- Enter the amount of your new grant - whether an offer grant or an annual refresh.

- Estimate how much your RSU value will increase per year.

- Input your current marginal tax rate on vesting RSUs.

- Decide on your strategy. "Sell Vests" assumes you sell immediately upon vesting shares, while "Hold All" assumes you keep your granted shares.

- Let us know your company's RSU calculation. "Share Conversion" is for companies that convert to a share amount upfront and expose unvested shares to market pricing, while "Fixed Dollars" converts to a share amount only at vest.

By default, the calculator assumes your grant vests equally over four years, with a one-year "cliff" and quarterly vests. The cliff is the first date you receive any share of the new grant. Cliffs are typical for a new hire grant, although ongoing grants (also known as top-ups or refreshers) sometimes vest immediately.

Advanced: Set a Vesting Schedule

If your company has a different restricted share vesting schedule or your shares don't have a 12-month cliff:

- Hit the "Show" button for the Vesting Schedule.

- Enter the percentage of your grant that vests in each year (up to year 6).

- Choose the vesting schedule your company follows – Annually, Quarterly, or Monthly.

- Set the length of the RSU cliff or the month where you first receive any percentage of the new vest.

RSU Projection Outputs

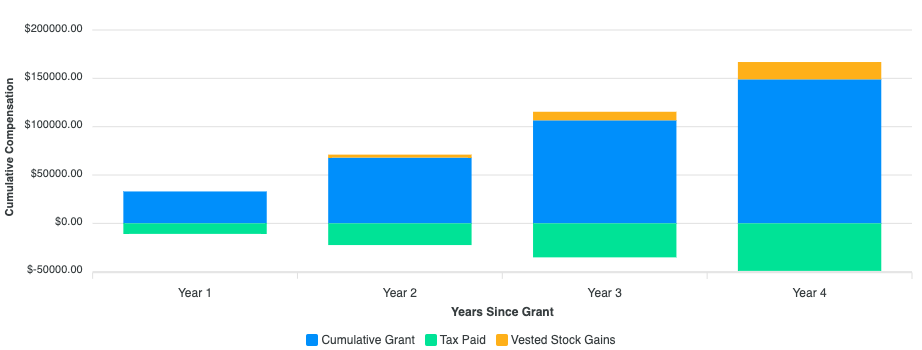

There are two output options – if you choose "Calculate," you'll receive a numerical projection of your strategy. "Draw Graph" will compute a numerical projection and also show you the cumulative breakdown in compensation from your new grant over the vesting period.

- End of Year: in the table header, you can see which year the tool is projecting.

- Total Amount Granted: If your company exposes unvested shares to market pricing, this field projects the actual dollar value of your grant by totaling over vesting periods. If it converts to shares at a fixed value at vest, it will equal your initial grant.

- Total Tax Paid: This field shows how much you paid in taxes based on what you owe at vest time.

- Ending Cash Balance: If you choose to sell your shares immediately, this field shows the balance at the end of the last projected year (at 0% interest).

- Ending Stock Balance: If you choose to keep your shares, this field shows the estimated value of your stock at the end of the projection.

If you choose to graph your scenario, you can see how the new grant evolves. The graph will estimate your cash at the end of each year, or your stock's fair value (including and market gain or loss if you hold your shares).

RSU Questions

I've been working at companies that issue RSUs for... well, my entire career (yes, at my day jobs). Here are some of the questions about RSUs that come up.

What are RSUs?

RSUs or Restricted Stock Units are a form of equity compensation where companies promise to grant you future employer stock based on various criteria. For some industries, they are a large part of overall compensation – in some senior roles, they are the largest component.

Most commonly, RSUs are promised upfront and rewarded on a schedule. For example, one common schedule for a new hire is RSUs awarded over four years with a one-year "cliff" (or first vest hurdle), and the remaining shares vesting equally over four years, every quarter. Most companies also refresh or "top up" your grants annually or in conjunction with high-performance or a promotion. Sometimes these refreshers vest immediately, while other companies also add a new cliff.

RSUs nearly always have a value. RSUs convert to shares and a claim on the future performance of a business, so except in the case a company goes bankrupt and equity is wiped out, there's a future market for that equity. Generally in the United States, you owe tax at the time your RSUs vest – that is, when they turn into common stock.

Generally, publicly listed companies grant RSUs – although private companies have started to grant RSUs (liquidity is more complicated pre-IPO, although some companies enable a secondary market).

Should I always sell my RSUs?

Canonically: it's best to sell your vested shares and diversify your savings to something unrelated to your employer (and even your industry). Additionally, your employer might levy additional restrictions on your trading, which makes employer stock less advantageous to hold:

- You probably have a limited trading window or could be restricted at points due to holding insider information.

- You may not be able to buy or write options on your shares (or use them as collateral for things like loans).

- You may be restricted from taking positions in other companies in your industry.

Especially with trading windows, it can be complicated to sell shares at a loss without hitting wash sale rules [PDF] from new RSU grants or ESPP shares.

However, there are strong counterarguments in favor of keeping at least some shares:

- You are probably well versed in your competitive position and potential – if there is any company you are qualified to trade, it's your employer.

- Sometimes illiquidity works in your favor; if you are blocked from trading mid-quarter, you are less prone to make rash investment decisions because of a fall in the broader market.

- In some cases, you have to hold some shares as a condition of your employment or to qualify for a board seat.

It's not as simple as a binary "never hold" or "always hold". Take the diversification argument seriously, for sure – Enron, Arthur Andersen, and other companies show it's possible your equity goes to zero. But you can also sometimes find success through a concentration in one company's shares – and you do likely have a knowledge edge with your employer.

All I can say is: it's up to you. Make sure you are at least well-diversified before you take any big swings. Personally, I've sold a reasonable amount of past RSUs, but also hold a respectable amount of vested shares (and none of my employers' stock has gone to zero – knock on wood!).

Should I pay taxes I owe on grants in cash?

In most countries (including the US), you are required to pay tax on your RSUs as soon as they vest. However, many companies let you choose to pay your taxes using cash instead of selling a portion of newly vested shares to raise cash.

In theory, paying your taxes in cash is no different from buying your company's shares in the open market. In practice? It's complicated.

For some companies, stock-based compensation is quite significant – and the total company-wide shares sold for taxes are a substantial percentage of the stock's daily average trading volume.

It's sometimes worth it to pay the tax in cash even if you plan to sell within the next few days, to avoid distortions caused by all of the forced selling by your co-workers. Your mileage may vary. (And if you plan to keep your shares, it's something you should model as well.)

Projecting an RSU Grant's Effects

Especially at many technology and biotechnology companies, stock-based compensation can be a large component of your total compensation. And through some market cycles, people who sit on their hands and keep shares have performed extremely well – but beware of concentrating too much risk in a single company. Your employment and benefits already depend on your employer – do you want to add a significant amount of savings risk, too... especially if you don't have a substantial mass of other assets?

However, except in the most extreme cases, RSUs are real money – this isn't phantom equity you should write off. If you work at a publicly traded company, or a private company with a secondary market, IPO on the horizon, or potential for M&A, take your equity compensation very seriously.

RSUs are some of the best benefits an employer can offer and they have the potential to appreciate wildly based on your company's performance... and the market's overall levels, of course. Keep an eye out for companies with generous grants – and hopefully, this tool helps you better value your restricted stock!

Other Resources: