In our last post on the yield curve inverting we discussed differences between a few terms. Specifically, the 5 Year Treasury and the 3 Year and 2 Year Treasury have inverted in recent days.

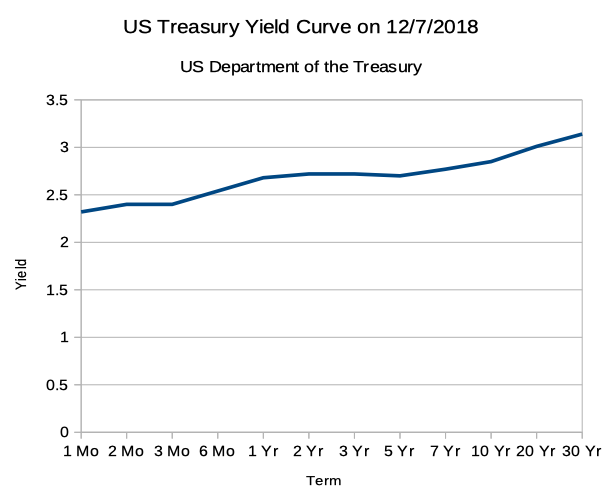

As of 12/07, the 1 year threatens to join the inversion party; 5s1s now sit at a mere .02% difference:

5s3s, 5s2s, 5s1s - these are all interesting measures of the curve. However – for better or worse – the financial press tends to concentrate on the 10 year Treasury and the 2 year Treasury Difference. That's now at .13% – so no red flags (yet?) if you're waiting.

So... which yield curve sample is best?

Yield Curve Inversions and Academic Literature

The financial press's concentration on the – not yet inverted(?) – 10s2s is a notable phenomenon. Back in August, the Federal Reserve Bank of San Francisco addressed the issue.

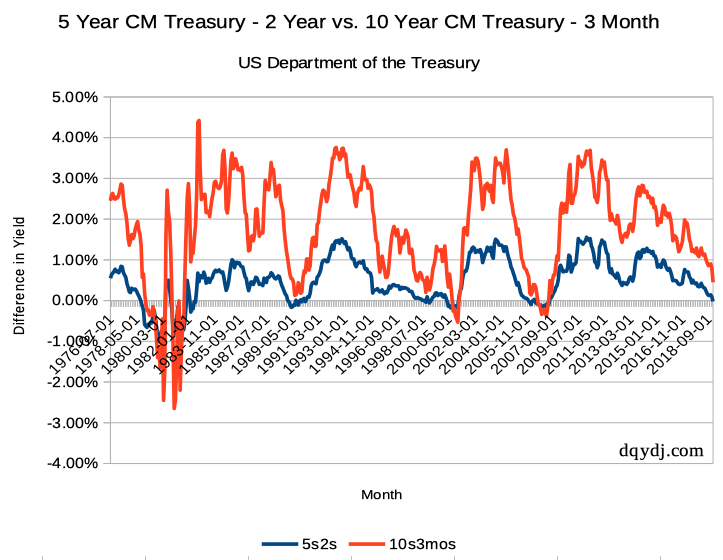

One takeaway - academic and economic research actually tends to concentrate on the 10 year - 3 month spread. It happens to be the term spread with the highest predictive power (but not necessarily through inversions).

It makes sense when you think it through - it's comparing the almost immediate term to an intermediate to long term view of the next decade. Even if you don't perfectly know the future (who does?) you can, finger in the air, say the near-present is probably tougher than the long run view.

Should We Ignore Intermediate Term Inversions?

In the inversion post we said there are three ways to approach the 5s3s and 5s2s inversions:

- It's a real indication of trouble – beware.

- It's a fluke – there is some technical or temporary explanation for the inversion.

- "This time is different" (as the yarn goes - the four most expensive words in investing).

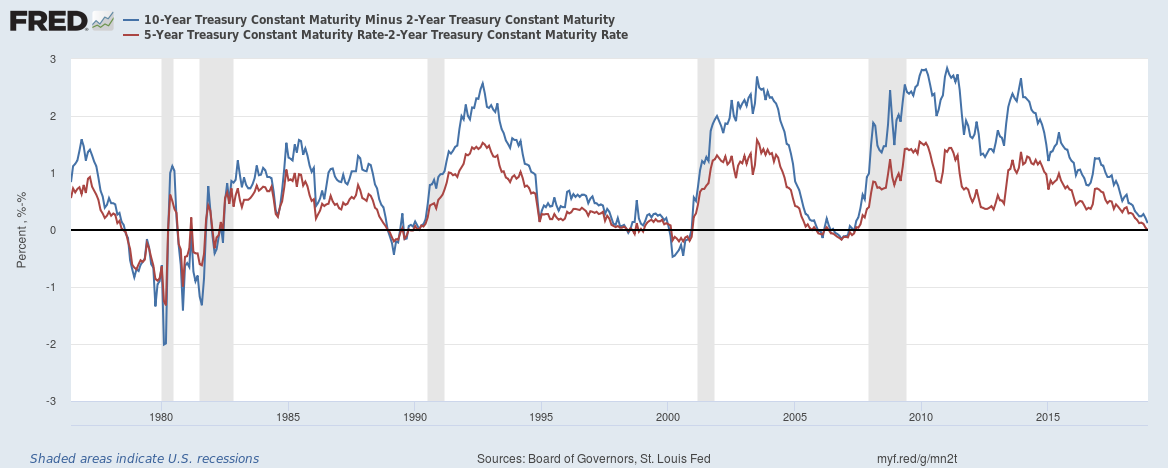

There's not a ton of historical data on the 2 year constant maturity treasury. Still, let's look at 5s2s compares to 10s2s back to '76:

... Not much hope in the last 42 years. Every time (save 1) the 5 year minus 2 year inverted the 10 year 2 year soon followed. (The weird exception: February 1, 2000 where the 10s2s beat the 5s2s by a day).

The takeaway: at least for 5s2s vs 10s2s it's been a distinction without difference.

How About the Short Term?

The researchers out there will appreciate if we do the same for (proxies of) the 3 month.

In our post visualizing yield curve inversions we took the 10s3mos back to the 1800s... kind of. Let's lazily only go to 1976 today:

Useful? Well - maybe.

You'd see flattening early, but there's no flashing red light like an inversion you'd get with the 10s2s or 5s2s. Using only inversions on the 10s3mos you would have missed the early 90s recession completely(!).

Maybe when the slope on 10s3mos went negative you could have reacted better with your investments. Not sure - if you can formulate a theoretical there let me know, I'm happy to look into that one further.

Handling Intermediate Term Inversions

Yogi Berra once said, “It's tough to make predictions, especially about the future.” Indeed - and it stands to reason that if predictions are hard, they're even harder the longer the timeframe.

However! – waiting for a 10s3mos inversion isn't the best plan... just see the early 90s. Further, holding out for the 10s2s is a... notable strategy... but it's a distinction without difference in the limited data. It seems that even if the exact timeframe is fuzzy, we do need to pay attention to the intermediate term spreads.

I do have skin in the game here. As discussed previously, I'm moving towards 60:40 risky:safe from my previous upper 70s risky. For our age and situation that's a conservative allocation, but hey... how do you value sleep? (ha)

(Also, hilariously, it's already paid off some - that's obviously too short for significance though).

How are you approaching the intermediate term inversions? Do you care about the 5s1s weakness or are you holding out for a 10s3mos or 10s2s inversion? How much do you concentrate on hitting exact dates, especially in the future? Love to hear your thoughts.