Every year, "conveniently" timed with tax season, we remember that DQYDJ is ostensibly a personal finance site. Let's turn tax-frowns upside down with a post on asset allocation here in in April, 2019.

Why bother? It comes back to skin in the game – a phrase recently repopularized by Nassim Taleb. In his book with the too-convenient title Skin in the Game, he lays out the reasoning perfectly:

“Don’t tell me what you think, tell me what you have in your portfolio.”

- Nassim Taleb, Skin in the Game

Positioning Our Portfolio for Safety in April 2019

Asset allocation is an interesting topic. We like to approach it with a view of all of our liquid – read: non-real-estate – assets.

In our recent post on the yield curve we mentioned our target for a 60/40 risky/safe ratio. We talked about it again in our 2018 savings rate post. We*'re anticipating choppier investment waters than the last few years.

How did we do after the self-audit? Pretty close!

| Safe Assets | 34.72% |

| Risky Assets | 65.28% |

*"we" here equals mid 30s, married, with two kids.

To be honest, it's not all that far off from our allocation last April: 62/38. However, investment gains and savings over the year threw it off – this allocation wasn't a given.

A few months ago risky assets were upwards of 80% of our liquid portfolio.

Domestic and International Split in April 2019

Last year, we mentioned that our allocation to international - at 29.5% - felt low. Here's this year:

| Cash & Bonds (Domestic) | 34.72% |

| International Stock | 12.73% |

| Domestic Stock | 52.55% |

So - 87/13 if you care about the safe stuff, 80/20 if you don't.

We're a bit uncomfortable here. There are some excellent arguments for overweighting the United States, of course:

- We plan to retire here (Forex risks are baked in)

- Large public companies already do business overseas (JL Collins has best led the charge on this argument)

- We know the US best

The third argument is, of course, the weakest. Knowing it well introduces bias. Additionally, in theory, buying a well constructed index means we don't need to know a country.

For the record, that 20% allocation is us over-weighting Pacific markets and Europe. We'll watch this, but I'm not as concerned about fixing this bucket as I was in the past.

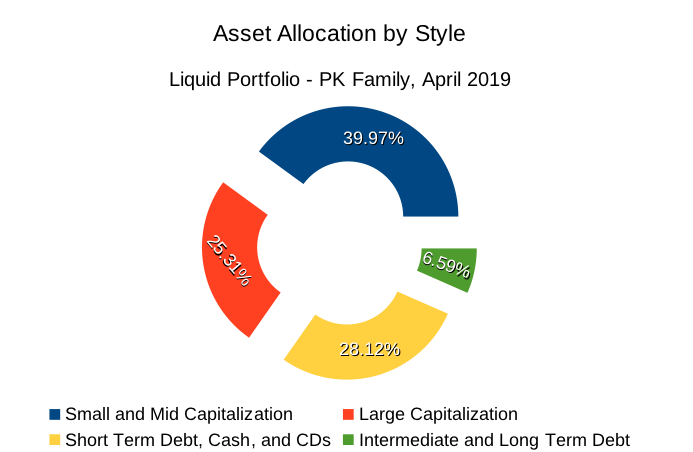

Style Allocation in April 2019

I broke down our allocation into four styles based on the types of investment:

- Large Cap Stocks (roughly the 5% largest public stocks)

- Medium/Small Cap Stocks (including vested equity in my employer)

- Short Term Debt, Cash, and CDs (<= 2 years duration)

- Intermediate and Long Term Debt

The takeaway here?

We should probably flip our small/mid cap exposure with large cap....

As for the Short vs. Long/Intermediate term disparity? It isn't really fixable with the yield curve in its current state.

Best case, perfectly timed 30 year Treasuries would have yielded 4.85% in April 2010 – buying today gets you under 3% for 30 years. With short term cash yielding over 2% in all our (non-checking) accounts there's really no need to fix this.

Why Bother Messing with Asset Allocations?

Setting aside the fact we had roughly the same percentage of safe & risky assets last year, why bother changing it around? Isn't it market timing to move to only 60% risky assets at our age?

Maybe, but how you define this allocation doesn't phase us. Our goal is to set ourselves up for a minimum of stress in a choppy market.

Imagine: starting with a 60/40 breakdown, where safe assets appreciate by 5% in a fall while risky assets fall 50%. That leaves us around 42/58 risky/safe - and only 28% down!

50% isn't really a random number. That was what the last two bear markets temporarily destroyed in value.

(If stocks surge in 2019 accompanied by a mid 2% return on safe assets? Well, I'll have to fix my allocation for this post next year...)

I don't think working out of a 60/40 breakdown for a while is bad. The trick is, of course!, moving back to a riskier allocation when and if we see a real fall.

How is your asset allocation post-tax season?