Sometimes we feel that DQYDJ gets an unfair reputation as a solely-individual investing "beat the market" type blog. While our most prolific writer (...me), does maintain an actively traded portfolio, we just did the math - it's only 37.4% of our equity investments.

Oh, and that counts employer equity awards and holdings - needless to say, we're actually mostly in the passive camp.

Cyclically Adjusted PE Ratios

That doesn't mean that we don't use valuation statistics to inform our portfolios.

One of those statistics is the CAPE - the cyclically adjusted PE ratio - of a country's stock market. The CAPE, for the uninitiated, comes from Professor Robert Shiller and uses the last ten years of earnings (inflation adjusted) to produce a normalized price to earnings ratio, instead of using earnings which may, for all we know, be occurring at an unseen peak in the markets. If you're interested, we wrote a little bit more about the CAPE here and here.

Now, the interesting thing about the CAPE is that, more than a number, it's a methodology - if you can find reasonable earnings for a company, sector, index, or even country - you can make an estimate of past and current CAPEs for the investment in question.

That's where today's piece enters: our friend forwarded us Joachim Klement and Oliver Dettmann of Wellershoff & Partners Ltd's research on the current CAPE in 38 different countries around the world. You can find it here, on SSRN (full paper linked from there).

The US, and the Rest

We don't need to rehash the arguments about the United States - yes, the CAPE is high for the US, and it would take very strong earnings... or, alternatively, a price drop... to bring it into line with historical valuations. Even if you find CAPE a crude measure prone to error and vulnerable to changes in accounting practices (as the current argument goes), it's still interesting to view it across various world economies. Here is the money shot... the US versus a number of established economies:

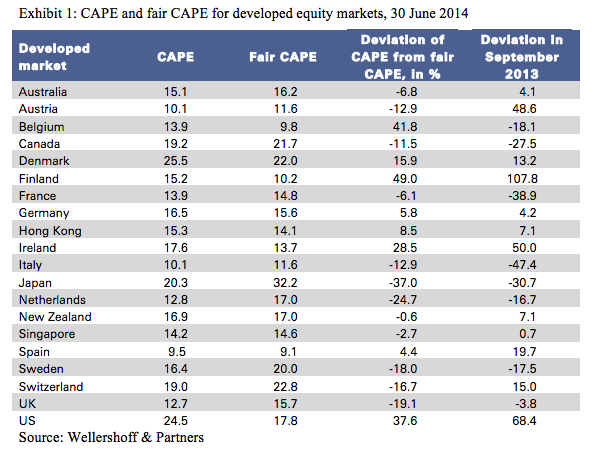

CAPE in Selected Core Countries (Wellershoff & Partners Ltd)

And, another great shot from a macro perspective:

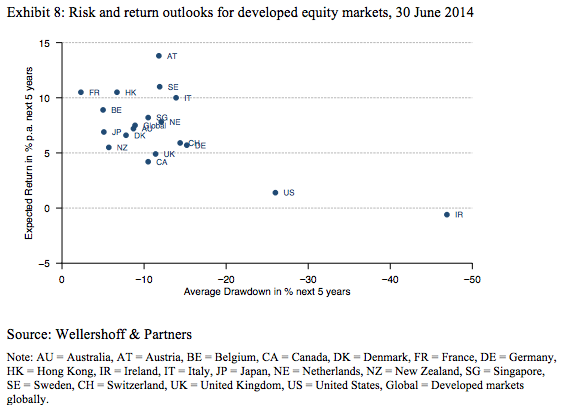

CAPE-Predicted Returns and Drawdowns, Selected Countries (Wellershoff & Partners Ltd)

Your Takeaway

Now, adherents to the CAPE in the United States were taking a bit of heat in the press - at least until the market strung together a couple down days in a row. An honest CAPE observer, however, would note that future returns at current levels aren't negative - they imply low single digit returns over the next decade or so. Of course, the market tends not to move in a straight, well behaved, line - which is why the risk of a dip followed by above average returns shouldn't be discounted.

So, if you are a CAPE adherent, you should give the paper a read through - it looks like you've got a number of other reasonable countries to investigate while making your investments!