If you've read Don't Quit Your Day Job... for a while, you've likely noticed the tension between us three writers over whether or not markets are rational and whether or not market irrationality is worth attempting to exploit due to transaction costs and risks.

See The Finale - What Does it Mean?

On Nobel Prizes...

Recently, our hilariously pointless sparring (pointless in the sense Bryan and I still continue to purchase individual securities) stepped up a notch due to the Sveriges Riksbank Prize in Economic Sciences in Memory of Alfred Nobel (commonly shortened to the Nobel Prize in Economics) being awarded to Eugene Fama, Robert Shiller and Lars Peter Hansen.

Fama is, famously, a militant believer in the efficiency of public markets, and the popularizer (if not the first) of applying the concept of random walks to stock market prices. Robert Shiller (a name that often crops up on our site) covers the other side of the field - his seminal work is on security pricing, bringing the concept of smoothed 10 year earnings (I believe first appearing under Benjamin Graham and David Dodd) to the stock market as a means to predict returns. Hansen's work is of a far more technical slant - but suffice to say, his work is invaluable in evaluating the theorems posited by Fama and Shiller - read his 1980 paper with Robert Hodrick. (His work is also beyond the scope of this article!).

Is the Stock Market Overvalued?

Which brings us to the point of this piece - adapting Shiller's methods to look at the current stock market (our proxy today is the S&P 500).

But why care?

A few reasons, really.

Sure, lots of mainstream investment advice nowadays warns you off trying to time the market. That's fine - but wouldn't you want to know when a historically predictive indicator was flashing red?

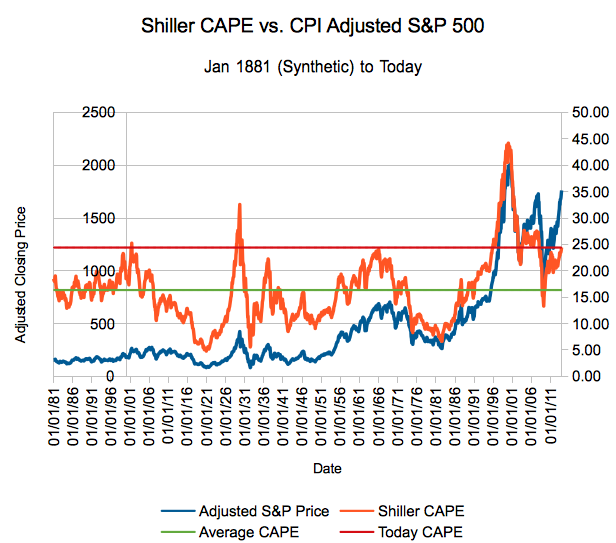

What's going on in this chart?

I've taken Shiller's historical stock market data on the S&P 500 (including the reconstruction before the S&P 500 existed) and scaled the S&P 500 closing price using CPI. The orange line is Shiller's "CAPE" - the cyclically adjusted PE ratio, which is a smoothed and inflation adjusted number representing the previous 10 years of earnings.

CAPE's historical average (as of my retrieval of the data on 11/3/13)? 16.36. Today's CAPE? Around 24.42. (Green and red lines, respectively.)

So It's Overpriced?

Remember, we recently came off a pretty historic drop in earnings - spiking the S&P 500's price to earnings ratio temporarily in the 2008-2009 time-frame (that's just the law of small numbers - we never went negative). Also, as Professor Jeremy Siegel has argued, changes in accounting rules have negatively biased CAPE due to massive write-offs in the last 10-15 years.

Okay, sure, but we've also had two periods of quickly increasing earnings in that time - and cash flow isn't an easy entry to come by for the market as a whole (at least with publicly available data - I'll see if I can derive it for you eventually). Additionally, many folks suggest using the regular Price to Earnings ratio of the market - either the trailing 12 months or analysts expectations - in place of CAPE while the ratio normalizes. To them we must ask: when you encounter volatility in a model, do you contend it's better to average less samples? Hah! (RIP Marcia Wallace)

Truth is, CAPE is taking the bad with the good. Even if earnings were misstated for a few years, CAPE would average the 'bad earnings' in with the good and give you a smoother result with the changing tides. My contention is that it's still useful to look to CAPE and say, "hey, we're not getting as much for our money as we once did".

If you don't like that answer? You can use TTM or forward looking P/E on the S&P 500. According to the Shiller numbers (S&P earnings are only available through June) you're looking at around an 18 P/E for the trailing 12 months, and a 15.5 P/E average all time. Using Yahoo! and the ETF SPX, the 2014 P/E is expected to be around a 17.62.

The Final Word?

There won't be one, unless we look back in the future. That's why we'll be taking look at a few more measures of market valuation over the next few pieces - so you can develop your own models by taking hints from the best. It's important to note that Shiller himself interprets his model as saying that prices are high - but not bubbly (at least not yet).

In the tradition of The Daily Show, here's your moment of Zen: Shiller talking about the Nobel Prize in the New York Times. Enjoy.