Way back in 1968 (before many of you readers were born) when Robert Shiller was still getting his Master's at MIT, a man named James Tobin published a rationalization for market valuation with his partner William Brainard.

Tobin was an Economist of the Keynesian variety, and a supporter of Government intervention to spur economic growth. His fame came from the so-called "Tobit Model", a model he published in 1958 which could be used to calculate a relationship between two variables. He also was known for suggesting the "Tobin Tax" on foreign exchange transactions. He won the Nobel Prize in 1981.

Today, however, we toss him into focus because like our friends Shiller and Buffet, he and Brainard had a useful model for market valuation - known today as Tobin's Q.

See The Finale - What Does it Mean?

Back in the Ivory Tower

In this series we've whip-lashed between the Ivory Tower and Wall Street - or at least Yale and Omaha. Tobin's method brings us back to Academia, but thankfully to a ratio with an impressive history. While it's important to note that the q can be applied to individual firms, as a valuation metric it is (obviously) best applied to the stock market as a whole.

Have you ever had a home appraised?

One of the valuation metrics used to value homes is the so-called cost of replacement. Tobin's q is a rough approximation of whether a company (or, for our purposes, companies) is being priced at more or less than it would cost to replace. For the purposes of market valuation, the Federal Reserve Board of Governors publishes everything we need, as represented by this fraction:

Nonfarm Nonfinancial Corporate Business Equities and Liabilities

________________________________

Tobin's q

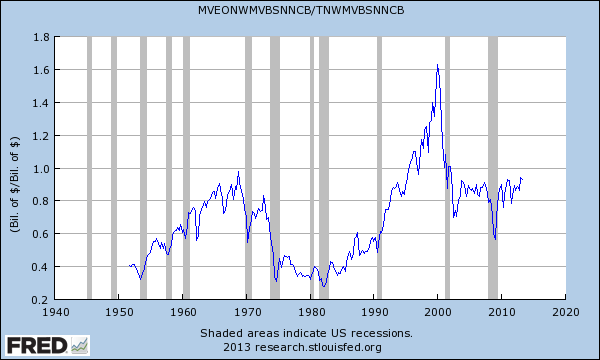

Here's how the q looks going back to the 40s:

(Links to the 2 series are in the quote box above).

All time, the average Tobin q is ~ .693 and the median is ~.714.

The most recent q? .92

So It's Overpriced?

Of the three ratios we've looked at so far, the stock market is most obviously 'overvalued' by Tobin's q. Remember, what we're trying to do here is basically figure out what people are paying for a company (based on liability and equity prices) versus the net worth of the company. You'll note that since the early 90s, the q has become elevated - only once flashing a buy signal (between 3Q 2008 and 2Q 2009 q never went above .716).

That could mean a few things, but one theory is the most interesting - perhaps net worth is understated?

Goodwill is a measure that companies hold on their books which attempts to balance the intangibles of a company often due to mergers and acquisitions in the market. However, there are a few other things which might be considered assets, without GAAP agreeing: 'brain trust' or amazing talent at the firms, or perhaps assets held at purchase price instead of fair value. Or (and here is an interesting one): political effects or barriers to entry which make it so companies already in the market can keep out new competition.

Let's hope it's not the last one, eh?

The Final Word

Sadly, we can't ask Professor Tobin - he passed away back in 2002. However, I did find an interesting piece in the New York Times from 1996 estimating Q for the S&P 500 at around 1.4 to 1.5. If you had sold then? Well, you would have missed the Tech Bubble.

However, q is still historically high, and an interesting ratio for your toolbox. Use it in good health.