One question we get quite a bit is related to the fundamentals of saving: is there a magic savings rate?

In the past we’ve looked at the ideal savings rate. There we suggested 20% as a minimum savings rate, with the caveat you should save more if you can.

Interestingly, there are also some magical savings rates. These rates are mathematically elegant: without even worrying about returns, they help you reason about savings and amounts. Let’s discuss those magical mathematical breakpoints and savings rates today.

The Most Magical Savings Rate

The most magical of all the savings rates is 50%.

When you save 50%, for every year you work you’re saving one year’s worth of spending. In essence, you’re paying for the entire next year by working during this one.

Importantly, this property doesn’t require any investment gains whatsoever.

Presumably, you’re earning some interest on your savings. Even if you’re only being paid a small return, everything on top of 50% is gravy.

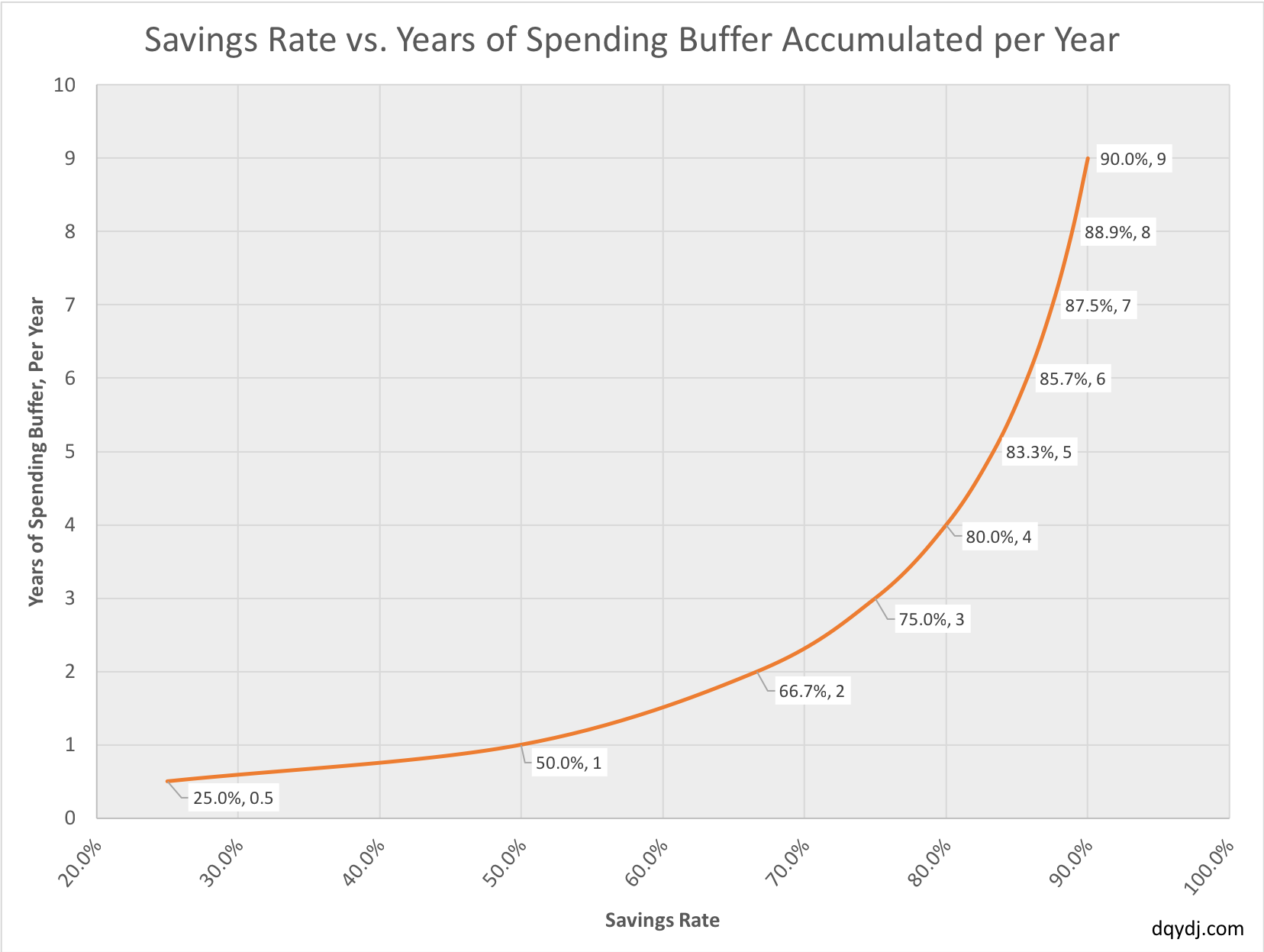

Savings Rates vs. Whole Years of Spending

20%, 25%, and 33% are also magical savings rates. Although they don’t provide a spending buffer for an entire year, they also make the math easy on income replacement:

- 20% savings rate: for every 4 years of work, you save 1 year of spending.

- 25% savings rate: for every 3 years of work, you save 1 year of spending.

- 33% savings rate: for every 2 years of work, you save 1 year of spending.

How does it work so cleanly?

It boils down to a simple fact: money you save is money you aren’t spending. Without knowing any more about your situation, I know if you save money you didn’t pay it in tax or spend it.

Extremely High Rates and Spending Breakpoints

Because of the above property that saving is non-spending, extremely high savings rates make the financial picture even better. For this article, we’re calling a savings rate over 50% extremely high savings rates.

That makes the inversion of the above magical rates interesting. Flip the above rates for spending and here’s what you get:

- 80% savings rate: every year, you save 4 year of spending.

- 75% savings rate: every year, you save 3 year of spending.

- 66% savings rate: every year, you save 2 year of spending.

Sometimes it helps to look at savings really as spending buffer building.

The Deceiving Top End

Now, undoubtedly, extremely high rates are... extremely hard to sustain. However, they cover up an interesting mathematical property: savings rates aren't linear, they're closer to exponential.

Take 50% savings, for example, which saves one year worth of spending. It takes an additional 16.7% savings to turn 1 year of savings in a single year to 2 years of savings.

Now you can see the curve...

Respectively, it takes 8.3%, 5%, then 3.33% to add another year of spending buffer in a single year. These high rates are deceiving – by the time you get to 90% savings, that's 9 years of savings buffer for a single year of spending.

Capturing the Magic of High Savings Rates

A 90% savings rate is more than twice as effective as an 80% rate.

-DQYDJ

The best part about reasoning about savings rates in this way? It doesn't require coming up with investment gains or interest returns. All of these numbers are achievable with money under your mattress.

(Don't store money there...)

The key takeaway: people tend to group these rates together, especially at the top end. However, because savings is "not spending", extremely high savings rates are volatile.

The difference between 80% savings and 90% savings is a whole 5 years of spending buffer at 90%. Stated differently: a 90% savings rate is more than twice as effective as an 80% rate.

Now, the magic makes more sense. If you're targeting financial independence, your goal should be as high a rate as possible. The more you save, the more years of buffer you build at once... and the less you need to worry about investment returns.