Inflation expectations through Treasury breakevens – a concept we just visited – are a decent take on the market's opinion on the 'cost of holding money'. Mortgages are, of course, the standard means by which people acquire houses - usually borrowing money for 30 years to pay off the cost of a home (see some mortgage history here). One interesting perspective is to compare what a mortgage 'costs' in rate versus inflation to see how much of a deal a mortgage is compared to cash.

Comparing Mortgages vs. Breakeven CPIs

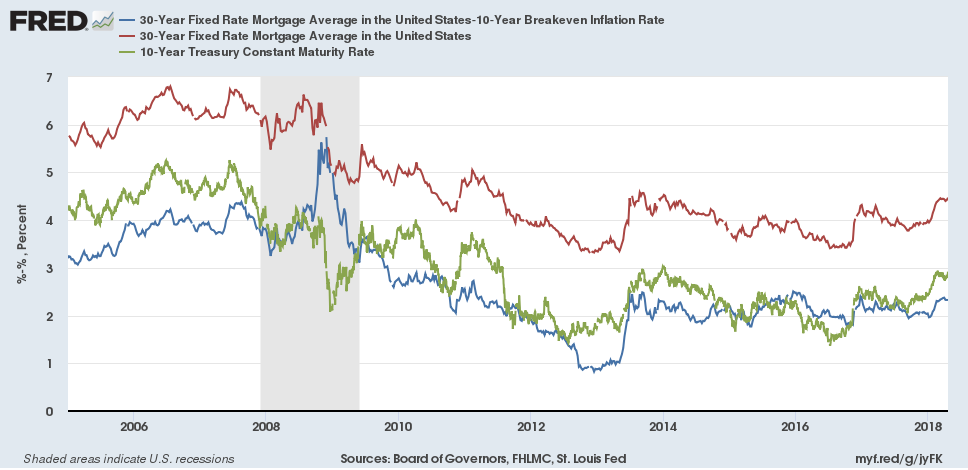

Nominally, the 30-year breakeven would be the comparable rate to a 30-year mortgage - but reality intervenes!

One apocryphal stat that used to make the rounds was the average 30-year mortgage lasts around 7 years. Dubious veracity, sure - but buying a new home or refinancing does turn mortgages over. Let's build on the urban myth (if you have a source, we're all ears) and call it 10 years.

Here are 10 year Treasury breakevens and 10-year constant Treasury maturity rates mashed up with the venerable 30-year mortgage rate:

And, the punchline: compared to a baseline of 10 year Treasury breakevens... mortgages are a slightly worse deal to where they were starting in 2013. You're paying about a 2.36% premium over 'expected' CPI to hold a 30-year mortgage for 10 years.

| Mortgage Premium over 10Y-B | 30 Year Mortgage | 10 Year Constant Maturity Rate | |

| Last Reading | 2.33% | 4.47% | 2.92% |

Increasing Mortgage Rate – and Inflation Expectations

It's a common theme in many cities - homes are quite expensive to purchase. For most purchasers, the 'cost' of a home is the product of the house purchase price and the affordability of a mortgage. The 30-year mortgage rate is now sitting a full percentage point above the lows it touched in 2013 - it was around 3 and a half percent for a 30-year.

We may never see those rates again... coming as they did during a period of low (or negative!) inflation expectations and a low spread. Still, mortgages are a decent deal – one thing considered – by this quick cut.

Is this the be all and end all of mortgage affordability measures? Certainly not - and this cut doesn't tell you anything about purchase price (we'll fix that soon). However, we like this framing - "what does the market demand on top of a safe inflation-adjusted investment"?

What measures do you use to look at mortgage and housing cost? Anything interesting you see in the data? Have a lead on 'average mortgage length' for us?