On this page is a bond yield to call calculator. It automatically calculates the internal rate of return (IRR) earned on a callable bond assuming it's called at the first possible time. Importantly, it assumes all payments and coupons are on time (no defaults).

Also, find the approximate yield to call formula below. Like with Yield to Maturity (YTM), Yield to Call is an iterative calculation. There is a shortcut equation to guess a yield to call which we cover below.

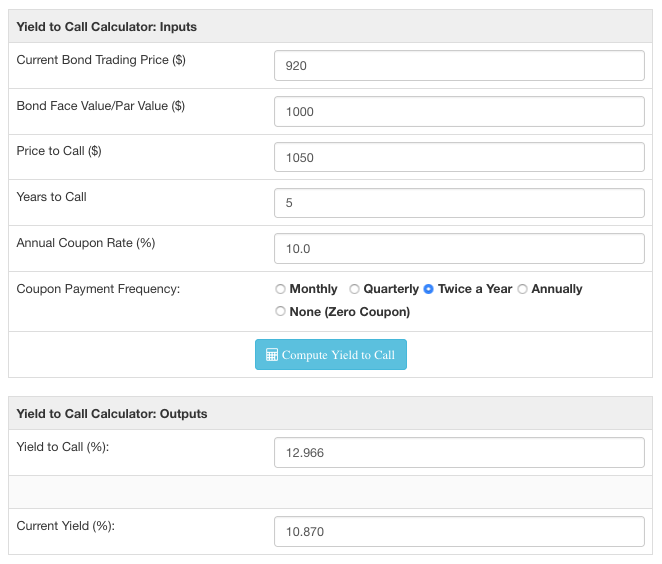

Bond Yield to Call Calculator

Yield to Call Calculator Inputs

- Current Bond Trading Price ($) - The trading price of the bond today.

- Bond Face Value/Par Value ($) - The face value of the bond, also known as par value.

- Price to Call ($) - Generally, callable bonds can only be called at some premium to par value. If there is a premium, enter the price to call the bond in this field.

- Years to Call - The numbers of years until the bond can be called.

- Annual Coupon Rate (%) - The annual percentage paid on the bond based on the par value (read: do not recompute it for the current trading price, the tool will handle it.)

- Coupon Payment Frequency - How often the bond makes coupon payments.

Bond YTC Calculator Outputs

- Yield to Call (%): The converged upon solution for the yield to call of the current bond (the internal rate of return assuming the bond is called).

- Current Yield (%): The simple calculated yield which uses the current trading price and face value of the bond. See the bond yield calculator for explanation.

Bond Yield to Call Formula

The calculation for Yield to Call is very similar to Yield to Maturity.

When making this calculation, we assume the bond will be called away at the first opportunity. Additionally, the price to call bond is usually a bit more than the face value of the bond – we use the price to call for this formula instead of the par value in YTM.

Estimated Yield to Call Formula

However, that doesn't mean we can't estimate and come close. The formula for the approximate yield to call on a bond is:

\frac{(Annual\ Interest)+((Price\ to\ Call-Current\ Price)/(Years\ to\ Call))}{(Price\ to\ Call+Current\ Price ) / 2}Estimating Yield to Call for the Calculator Scenario

Let's solve the default entry of the calculator:

- Current Price: $920

- Par Value: $1000

- Price to Call: $1050

- Years to Call: 5

- Annual Coupon Rate: 10%

- Coupon Frequency: 2x a Year

\frac{(100)+((1050-920)/5)}{(1050+920 ) / 2}=\\~\\\frac{100+26}{985}=12.792\%Exact Yield to Call Formula

Of course, if you hit the 'Calculate' button you get a different answer – namely, you'll get 12.966%. Why the disparity?

Internal to the tool, we calculate the return an investor would see then look at the present value of those cash flows. The summation looks like this:

Price = Coupon\ Payment/(1+rate)^{-1} + Coupon\ Payment/(1+rate)^{-2} +\\ ... + Coupon\ Payment/(1+rate)^{-n}+Cost\ to\ Call/(1+rate)^{-n}The calculator internally uses the secant method to converge upon a solution, and uses an adaptation of a method from Github user ndongo. The discussion of the formula itself is a bit heavy, but start with our references in the Yield to Maturity Calculator to read more.

(Yes, you'll want to do the math with a computer. Which... is what this site is, I suppose.)

Why Does Yield to Call Matter?

When you start investing in bonds, you'll soon recognize that bonds can either be callable ("redeemable") or un-callable. Callable bonds usually offer some sort of perk – like a higher interest rate – with the risk that the issuer might call it before its full maturity. If you don't care about the duration, it can be a win-win – a slight edge in yield, while the issuer can hedge a bit against falling interest rates.

In a sense, callable bonds are very similar to some forms of consumer debt.

Take mortgages, for example. When mortgage rates fall, people rush to refinance their current mortgages. In a refinance, people prepay – "call" – their current mortgage, paying it off in full. They then effectively reissue a bond at the prevailing rate... only to restart the cycle if rates fall an acceptable amount in the future.

It's not a perfect comparison, sure. (There are usually no prepayment premiums, most cost is up-front on a mortgage, etc.) However, it's a useful model to keep in mind when investing in bonds.

Know this: callable bonds might not behave exactly as you planned (although we assume the calculator default bond wouldn't be called!). Computing YTC like we've done in the calculator shows you the yield on your bond if it doesn't make it to maturity. And it's not always against you – some bonds have a put option; see the yield to put calculator for the nearly-equivalent yield to put.

Conclusion and Other Financial Basics Calculators

Use the Yield to Call as you would use other measures of bond valuation: a factor in your decision whether to buy or avoid a bond.

Yield to Worst on a Bond

Combining Yield to Maturity with Yield to Call and taking the minimum is known as the Yield to Worst. While yield to worst doesn't show you duration, it does show you the worst (from your perspective) possible annual yield you'd make when considering a bond.

If your bond is called, presumably you'll have to find another investment to substitute for it.

Yield to worst on a non-callable bond is exactly equal to the yield to maturity. On a callable bond, it is the lower of the yield to maturity and yield to call.

For other calculators in our financial basics series, please see: