Back in June 2019 we last checked on inflation expectations. Well, at least the kind measured by Treasury Breakevens.

In the ensuing months we watched the yield curve un-invert. We witnessed the President's impeachment, an initial trade deal with China, and all manner of international events.

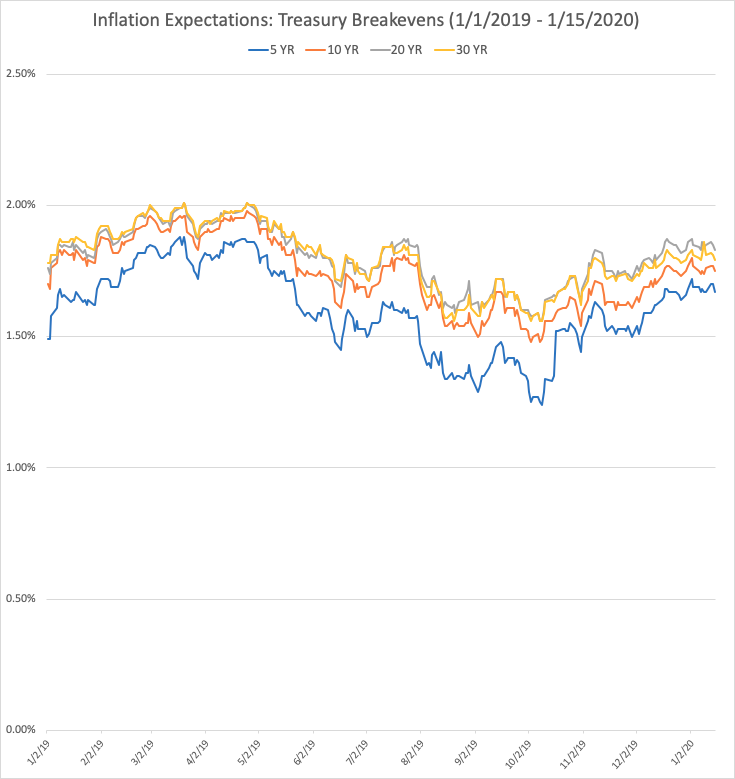

And inflation expectations have risen – back up to roughly where they were in May of 2019.

One Third of an Eye on Inflation Expectations

The yield curve and the other issues took all the air out of the room. But – yes, I've still been watching inflation expectations, kinda.

For some context, the Federal Reserve targets around 2% inflation annually (measured by PCE) as policy. It's a good middle ground inflation number which the Fed believes – with fair justification – helps maximize employment without the prices of goods getting too out of hand.

Since July 2018, inflation expectations have – for 5 year timeframes – been south of 2%. Here's how 5 year break-evens have tracked since 2010:

We don't know where we're headed, and it's important to remember that these numbers imply X% inflation over the next Y years. But – something flipped back in October, 2019 causing the current conditions and direction. Perhaps the anticipation of the third (and so far final) Federal Reserve rate cut in the current cycle?

Here's how expectations have looked this month (based on closing prices from the Treasury).

| Date* | 5 Year | 10 Year | 20 Year | 30 Year |

| 1/2/20 | 1.72% | 1.80% | 1.87% | 1.83% |

| 1/3/20 | 1.69% | 1.77% | 1.85% | 1.81% |

| 1/6/20 | 1.69% | 1.75% | 1.84% | 1.80% |

| 1/7/20 | 1.67% | 1.74% | 1.83% | 1.79% |

| 1/8/20 | 1.68% | 1.75% | 1.86% | 1.81% |

| 1/9/20 | 1.67% | 1.74% | 1.84% | 1.86% |

| 1/10/20 | 1.67% | 1.76% | 1.85% | 1.81% |

| 1/13/20 | 1.70% | 1.77% | 1.86% | 1.82% |

| 1/14/20 | 1.70% | 1.77% | 1.85% | 1.81% |

| 1/15/20 | 1.67% | 1.75% | 1.83% | 1.79% |

*Read the chart as "X% inflation each year over the next Y years".

Rising Inflation Expectations

Are there issues with using Treasury Breakevens as a proxy for inflation expectations? Yes of course – the Cleveland Fed has you covered.

It's also important to note that TIPS – the inflation adjusted securities used to construct this series – pay out on CPI not PCE. That, of course, makes my Fed talk a bit problematic.

In the immortal words of Carveth Read, "It's better to be approximately right than exactly wrong." Indeed – even if the numbers are slightly off, expectations have certainly shifted again. Investors expect more inflation moving forward than they did a few months ago.

What does it mean? Let me know your theories.