When it comes to setting your Retirement or Financial Independence date, the most important variable in your control is your savings rate. Which is fitting, because people often land here after asking "what is the best savings rate?". Let's work through the variables and try to come to an understanding of the ideal savings rate.

When it comes to setting your Retirement or Financial Independence date, the most important variable in your control is your savings rate. Which is fitting, because people often land here after asking "what is the best savings rate?". Let's work through the variables and try to come to an understanding of the ideal savings rate.

And if you don't want to read too much, we've got you covered with more than a "save all you can". As a savings rule of thumb, save a minimum of 20-25% of your post-tax income in lieu of other goals. To give yourself the most possible options in your career and life, save 50% or more (read about magic savings rate breakpoints).

We'll show you why further down the page. Onward!

Savings Rate vs. Rate of Return vs. Others

It's true, savings rate is an important factor but other things do matter. Rate of return, tax efficiency, changes in entitlement programs, continuing education, health, living situation, and others – these things will affect your goals. However, the most important thing you can do today is try to hit your ideal savings rate.

Should you spend less or earn more?

Here's the thing: if you can register a high savings rate it doesn't matter.

You can get a rough idea for how quickly someone can retire solely from their reported savings rate.

If you're saving 50%, you're closer to your "breakeven" date (the date when your savings can support your lifestyle on their own) than if you are saving 5%. Very often, the easiest way to do this is to increase your income - it's much easier to reach 50%+ savings rates with more income.

However, if you're new to personal finance you probably have un-examined expenses as well. If you can reduce these costs it's just as effective as earning the proper proportion after tax. As a bonus, savings are usually immediate.

Especially in the beginning of your savings journey, you should look at both sides of the equation. Earn more and spend less and you are guaranteed to have a higher savings rate.

The Ideal Savings Rate vs. Goal Amounts

There is an elegant truth behind savings rates:

If you are saving a certain amount, you are not spending that amount.

Say you make $50,000 after taxes a year. If you save 0% of that money that means you are spending $50,000. If you, however, are saving 50% of your salary? I don't even have to look, that must mean you are spending $25,000 of it.

That relationship also helps us determine how much you should have saved before you retire.

There are some caveats

- We'll ignore the effects of taxes, pensions, annuities, and entitlement programs. (See the tax equivalent yield calculator for a deeper examination.)

- Returns run at 10% a year, inflation it 2%, and 4% is a safe withdrawal rate. When this article is over, you can change the assumptions in our ideal savings rate calculator.

- Starting with $0 in savings.

- You don't touch the principal.

- You invest at the beginning of every month.

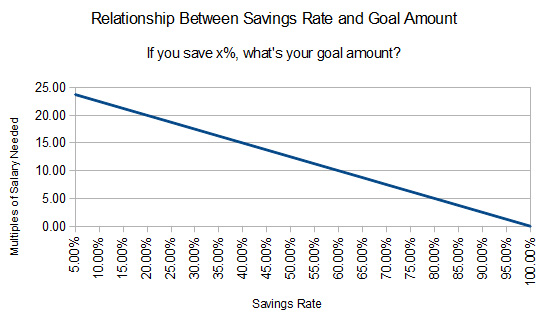

The Ideal Savings Rate Chart

- If you save 5% a year, you need to save 23.75x your current salary to retire using our assumptions.

- If you save 50%? 12.50x.

- 70%? 7.50x.

If you make $1,000,000 and you save 50%, you'll need $12,500,000 (in today's dollars) to maintain your exact lifestyle.

The math is exactly the same if you make $31,000 and save 50%- you'll need $387,500 to keep up your standard of living!

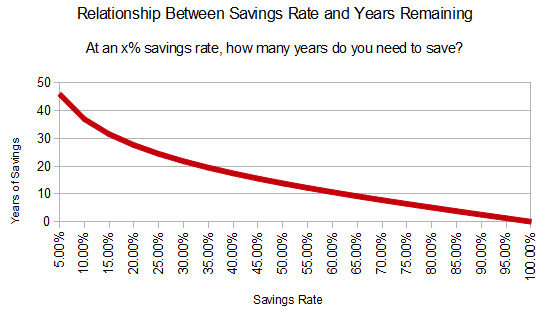

The Ideal Income Savings Rate vs. Years Until Retirement

The above section proves an important point: figuring out your ideal savings rate is multifaceted.

- A higher savings rate means your target is lower.

- A higher savings rate means you're putting more cash towards the goal every month.

Assuming a $50,000 income, if you're saving 5% that means you're aiming for $1,187,500 in savings. You're currently investing $208.33 a month.

How about 50% savings? For the same income, $625,000 and $2083.33, respectively.

As you'd expect, we're no longer talking about a linear relationship. Here's what happens when you apply saving rate and calculate years until retirement or financial independence:

Your best savings rate shows where you fall upon this curve

The Diminishing Effect of Investment Returns on High Savings Rates

You'll also notice diminishing effects of higher savings returns. Here's why:

- For lower savings rates, your cash is dependent upon market return.

If we were assuming higher or lower returns, you'd be changing the slope of the line at any point (the derivative, for those of you that care). Higher returns mean quicker goal achievement for low savings rates, while lower returns mean it'll take much longer. (Or it'll never happen...)

- For higher savings rates, you reduce the effect of market fluctuations:

The difference between 2% and 20% real investment returns for a 90% savings rate? Retirement in 2.20 vs. 2.70 years; respectively.

The higher your savings rate, the more you are insulated from the volatility of the market.

You'd only need 4.02 years to retire at a 90% savings rate with -20% returns. (Well, you would hope to get better returns after you retire though).

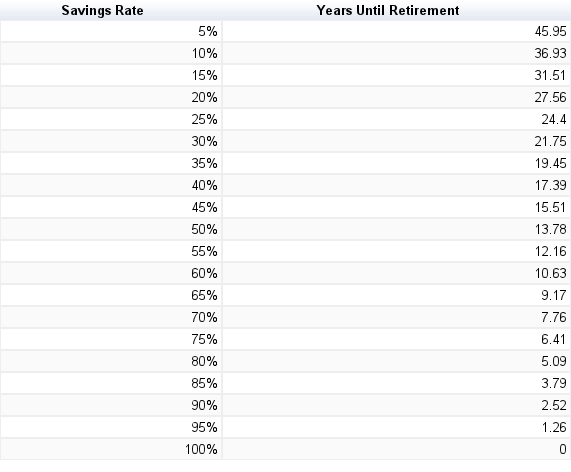

Graphing Savings Rates vs. Years to FIRE

FIRE, or "financial independence, retire early", is the minimum point where you no longer 'need' to work. With the math above we finally have enough theoretical underpinnings to show you ideal savings rates until FIRE.

Using this post's assumptions, here are our calculations for your current year savings rate versus the number of years minimum you need to FIRE.

Targeting Years Until Retirement is One Way to Find Your Best Savings Rate

Of course, if you save 100% of your income you "can" retire already. Often though, it's psychologically useful to save more to buffer yourself from very bad scenarios. This might mean something like a chronic illness or other expensive incident or ongoing expense.

What's The Best Savings Rate?

At a minimum, you should save 20-25% of your income. If you have other goals, I'll walk you through how to calculate the number below.

The interesting way to answer this question is to target independence by a certain year.

If you are a 22 year old new college graduate and would love to be independent by 40 (whether you choose to retire or not), these assumptions suggest you should save around 40% of your income.

Even if the market only gives you a 5% real return, you'd only have to delay independence until 43 or so. And if you want to, say, retire by 30? We're thinking right around 68-72% is the best savings rate for you.

Of course, not everyone is young with the ability to set their savings rate in such a matter...

For the rest of us, the best thing to do is to look at your current spending, and do what you can to decrease it. At the same time, try to earn more income.

The largest gains, of course (using our assumptions), will come onincreasing low savings rates. You gain more (24.2 years until FIRE) from the jump from 5% to 30% savings than from the jump from 30% to 75% (15.34 years until FIRE).

Savings Rate Rule of Thumb: 20-25% Minimum

In essence, I can't exactly tell you the best savings rate for your situation – but I can toss out some reasonable targets.

Minimum Ideal Savings Rate Target

Save at least 20-25%. This will cut your independence date roughly in half from a 5% savings rate.

Since the average professional career is roughly 40-45 years (assuming you can avoid injuries, chronic illness and later-in-life layoffs), 20-25% should leave you with enough cushion to deal with issues that crop up.

Better Savings Rate Target

If you can, save 50% or more. 50% is magic; for every year of saving you're adding a year's buffer in savings even if the market returns 0%.

Finding the Right Savings Rate for You

The takeaway: a minimum of 20-25% savings rate, plus benefits and pensions will put you in a decent spot, mathematically.

And always, aim to increase your income. Naturally, older workers tend to make more than new graduates up until around 35-45 years old. If you can solidify your savings rates early, you'll have a much easier time when you have more responsibilities outside of work mid-career.

Much better is saving 50% – or more – of your take home income. We discuss the compelling math behind extremely high savings rates in our magical savings rate article.

If you don't like our assumptions? Don't worry. Our ideal savings rate calculator can do this exact math to help you come up with your own goal.

Good luck!